Source: DeepTide TechFlow

While global investors are fixated on$NVIDIA(NVDA.US)$financial reports,Taiwan Semiconductor (TSM.US)capacity expansions, and Samsung's HBM yield rates, a quiet surge is unfolding on the Tokyo Stock Exchange.

On June 3, 2026, the Nikkei 225 index surpassed the 68,000 mark for the first time, posting a year-to-date gain of nearly 31%—triple that of the S&P 500 and more than double that of the Nasdaq over the same period.

This rally is far from a balanced, steady bull market; capital inflows are highly concentrated in one sector: the AI semiconductor supply chain. Just $Tokyo Electron Devices (2760.JP)$ and$Advantest(6857.JP)$two stocks together lifted the Nikkei index by approximately 840 points on that day.

This rally is far from a balanced, steady bull market; capital inflows are highly concentrated in one sector: the AI semiconductor supply chain. Just $Tokyo Electron Devices (2760.JP)$ and$Advantest(6857.JP)$two stocks together lifted the Nikkei index by approximately 840 points on that day.

Even more astonishing figures belong to$Kioxia (285A.JP)$a NAND flash memory manufacturer that listed on the Tokyo exchange only in December 2024. Its share price soared from an IPO price of ¥1,455 to above ¥78,000 in less than 18 months—an increase of over 3,500%—briefly surpassing$Toyota Motor (TM.US)$to become Japan’s second-most valuable company.

Behind these numbers lies an often-overlooked industrial reality: on the world’s most crowded AI race track, Japan neither designs nor manufactures chips—but it controls nearly everything required to make them.

From equipment, materials, wafers, passive components, power systems, and cooling solutions to fiber-optic cables—from the first cut of silicon to the final fiber connection in a data center—Japanese companies occupy the most upstream positions in the AI supply chain. To use a clichéd but apt analogy: in the AI gold rush, Japan is selling shovels, dynamite, and miner’s lamps.

We break down this supply chain into six tiers and examine, tier by tier, the strategic positioning, financial performance, and investment logic of Japanese companies.

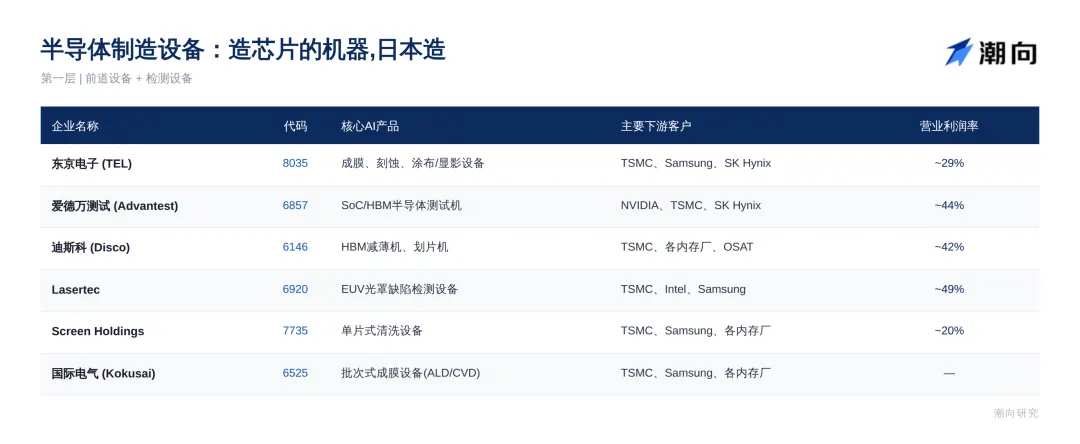

Tier 1: Semiconductor Manufacturing Equipment

At its core, chip manufacturing involves using extremely precise equipment to etch circuits layer by layer onto silicon wafers. The more advanced the process node of AI chips (GPUs, ASICs, HBM), the greater the number of fabrication steps—and each step demands ever-higher precision from the equipment. This makes semiconductor manufacturing equipment the segment with the highest technical barriers, the fattest profit margins, and the strongest certainty across the entire AI supply chain.

Japan holds the third position in this field, trailing only the Netherlands $ASML Holding(ASML.US)$ and the United States.Applied Materials (AMAT.US)Six core companies each control critical entry points across different process nodes.

Tokyo Electron (8035): A full-line front-end equipment powerhouse

Tokyo Electron is the world’s third-largest semiconductor equipment manufacturer and ranks among the top two globally in four key segments: coating/developing (with a near-90% global market share), etching, cleaning, and film deposition. No leading foundry—including Taiwan Semiconductor, Samsung, or Intel—can build advanced-node production lines without it.

For fiscal year 2026 (ending March 2026), revenue reached JPY 2.44 trillion and net profit hit JPY 574.45 billion—both all-time highs—with an operating margin of approximately 29%. Its 52-week share price ranged from JPY 19,870 to JPY 61,420, reflecting a gain of about 76% over the past year.

The migration of AI chips to the 2nm node and below entails more manufacturing steps per wafer and greater equipment consumption. This reflects an incremental logic where 'the more advanced the node, the higher the equipment value.' Of the 22 analysts surveyed, 17 issued buy ratings, with none recommending a sell.

Advantest (6857): The final checkpoint before every AI chip leaves the factory

The more complex the AI chip, the more critical testing becomes. Advantest holds approximately 50% global market share in SoC testers and maintains a similarly dominant position in memory testers. Every NVIDIA GPU and every HBM chip undergoes testing on its equipment before shipment.

For FY2025 (ending March 2026), revenue reached JPY 1,128.6 billion, surging 44.7% year-over-year, with operating profit at JPY 499.1 billion and an operating margin as high as 44%. Gross margin has remained consistently elevated at 55%–58%. Over the past year, its market capitalization grew by more than 309%, and its share price has risen approximately 145% year-to-date.

Each AI tester unit sells for several hundred million yen, requires lengthy test cycles, and exhibits extremely strong leverage effects when scaling production capacity. The company has further raised its FY2026 guidance to JPY 1,420 billion in revenue and JPY 627.5 billion in operating profit.

Disco (6146): Sole monopolist in HBM ultra-thin grinding equipment

Manufacturing HBM (High Bandwidth Memory) requires stacking multiple layers of DRAM chips, each of which must be ground to an ultra-thin thickness. Disco holds near-total dominance in the ultra-thin grinding equipment market, with a global share of 70%–80%.

For the fiscal year ending March 2025, revenue stood at approximately JPY 385 billion, up about 25% year-over-year, with operating margin exceeding 40% and gross margin estimated at around 60%. Its business model features a key nuance: 'equipment sales + high-consumption consumables (dicing blades and grinding wheels).' Each machine sold generates a continuous stream of cash flow from recurring blade and wheel replacements.

Lasertec: 100% global monopoly in EUV photomask inspection

Manufacturing the most advanced AI chips requires EUV (Extreme Ultraviolet) lithography. For inspecting defects on EUV photomasks, there is only one company in the world capable of performing this task— $Lasertec (6920.JP)$ , with a 100% market share—no other competitor comes close.

For FY2025 (ending June 2025), it reported revenue of JPY 251.4 billion and operating profit of JPY 122.8 billion, yielding an operating margin of 48.8%—the highest in the global semiconductor equipment industry. Its latest-generation product, the ACTIS A300, supports High-NA EUV processes and is equipped with its proprietary EUV light source, URASHIMA.

This is a business model based purely on a monopoly derived from disruptive technology, with extremely high barriers to entry.

Screen Holdings and Kokusai Electric (6525)

$Screen Holdings (7735.JP)$ is a global leader in single-wafer cleaning equipment. As chip manufacturing processes grow more complex, the number of cleaning steps increases geometrically, yet its operating profit margin remains above 20%. Kokusai Electric ($Kokusai Electric (6525.JP)$) is highly competitive in batch deposition equipment (ALD/CVD), with strong demand for advanced thin-film processes required for 3D stacking and HBM.

Tier Two: Semiconductor Materials and Silicon Wafers

Every chip begins with an ultra-high-purity single-crystal silicon wafer. AI chips demand far stricter requirements for wafer flatness and defect density than consumer-grade chips. Moreover, key materials such as photoresists, polishing slurries, and packaging compounds used in wafer production are almost entirely controlled by Japanese companies.

Shin-Etsu Chemical (4063) and SUMCO (3436): The silicon wafer duopoly

$Shin-Etsu Chemical (4063.JP)$and$Sumco (3436.JP)$ Together, they control more than 50% of global 300mm silicon wafer capacity. Including Taiwan-based GlobalWafers, Germany’s Siltronic, and South Korea’s SK Siltron, the top five players account for approximately 80% of the market—a concentration that is even higher in the advanced wafers required for cutting-edge semiconductor processes.

Shin-Etsu Chemical’s semiconductor silicon wafer business has consistently maintained an operating profit margin above 30%, aligning with the company’s overall consolidated profit margin of around 30%. Beyond wafers, it is also one of the world’s largest suppliers of photoresist raw materials, and produces epoxy resins for chip packaging and rare-earth magnets. This diversification across multiple critical nodes in the semiconductor materials supply chain helps mitigate risks tied to any single market cycle.

As a pure-play silicon wafer manufacturer, Sumco is more sensitive to supply-demand fluctuations in the memory market, with its current operating profit margin fluctuating between single digits and around 10%. However, the premium pricing for advanced wafers driven by AI demand will serve as the key engine for its profit recovery.

Both companies share a common strategy of 'restrained capacity expansion.' Having experienced the consequences of overcapacity in recent years, the industry shows little appetite for aggressive investment. Shin-Etsu Chemical is currently advancing new factory construction both in Japan and overseas, with plans to add more than 20% in new capacity by the end of 2026.

Tokyo Ohka Kogyo (4186) and Resonac Holdings (4004): The Invisible Army of Chemical Materials

Beyond silicon wafers, AI chip manufacturing consumes vast quantities of chemical materials: photoresists (which determine chip linewidth precision), CMP slurries (for wafer surface polishing), advanced packaging materials, and thermal interface materials.

$Tokyo Ohka Kogyo (4186.JP)$and $Resonac Holdings (4004.JP)$ (formerly Showa Denko) are global leaders in these fields. While their products may not attract as much attention as equipment, they are equally irreplaceable. The increasing number of process steps in AI chip fabrication directly drives up chemical material consumption per wafer.

Layer Three: Storage Chips

Both AI training and inference are tasks with extremely high data throughput. The loading of large language model weights and the read/write operations for KV Cache have driven exponential growth in demand for high-speed storage. NAND flash memory, as the core medium of data center SSDs, is currently undergoing an AI-driven supercycle.

Kioxia Holdings (285A): King of the NAND Cycle

Kioxia is the single most explosive investment opportunity in Japan’s current AI-driven equity rally—without exception.

Since its IPO in December 2024, its share price has surged by over 3,500%. Its 52-week price range spans from JPY 1,950 to JPY 83,140—an extraordinary level of volatility rarely seen among large-cap stocks in developed markets. For fiscal year 2026 (ending March 2026), revenue reached JPY 2.34 trillion, up 37% year-over-year, and net profit totaled JPY 554.49 billion, doubling from the prior year. The first quarter of fiscal 2026 was even more dramatic: quarterly revenue hit JPY 1,002.9 billion, soaring 189% year-over-year, while operating profit surged fifteenfold to JPY 59.68 billion, setting a new quarterly record. NAND average selling prices in U.S. dollar terms doubled during this quarter.

The driving force behind this surge is a historic supply-demand imbalance: explosive demand for NAND from AI data centers has collided with a supply side that will not see new capacity come online until the end of 2027. In June 2026, Goldman Sachs upgraded Kioxia from Neutral to Buy and raised its price target from JPY 48,000 to JPY 93,000. Kioxia has announced it will initiate dividend payments starting in fiscal year 2027 and plans to issue American Depositary Receipts (ADRs) in the United States.

The risks are very clear—the inherent strong cyclicality of the NAND industry. Currently,forward P/E ratiothe trailing P/E ratio stands at nearly 77x, while the forward P/E is approximately 8.8x. This stark discrepancy itself indicates that the market is betting on sustained explosive profit growth; should AI-related capital expenditures slow or new capacity come online en masse, prices could fall sharply.

Layer Four: Passive Components and Packaging Substrates

The hardware architecture of an AI server differs fundamentally from that of a traditional server. GPU motherboards require massive quantities of passive components—particularly multilayer ceramic capacitors (MLCCs)—to stabilize current, along with ultra-high-specification multilayer packaging substrates to support GPU chips. A single AI GPU accelerator card often incorporates several thousand to as many as 20,000 MLCCs—a quantum leap in component count compared to smartphones or PCs.

Murata Manufacturing: The Undisputed Global Leader in MLCCs

$Murata Manufacturing (6981.JP)$ It holds approximately 40% of the global MLCC market share, making it the dominant player. AI servers impose extremely stringent requirements on high-voltage, high-capacitance, and ultra-high-reliability MLCCs, and Murata possesses the deepest technological moat in this premium segment.

For fiscal year 2025 (ending March 2026), revenue reached a record-high JPY 1,830.9 billion, with operating profit at JPY 281.8 billion, yielding an operating margin of 15.4%. Sales to data centers surged by approximately 70% year-over-year. Murata explicitly stated that current orders for high-end capacitors from data centers have reached twice its existing production capacity, and this severe supply-demand imbalance is expected to persist for one to two years.

On May 29, 2026, Murata’s stock price rose more than 96% over the past month.

Taiyo Yuden (6976): The MLCC Stock with Highest AI-Driven Upside

$Taiyo Yuden(6976.JP)$ Ranked third globally in the MLCC market, MLCCs account for 64% of its revenue, giving it significantly higher exposure—and thus greater elasticity—to AI server demand compared to Murata.

Net profit for FY2025 skyrocketed 5.4-fold year-over-year to JPY 14.8 billion. Orders from January to March exceeded JPY 100 billion for the first time, with a book-to-bill (BB) ratio consistently above 1.25. Taiyo Yuden has already implemented price increases of 6%–13% on medium- and low-capacitance MLCCs. CEO Katsuya Sase described current demand levels in an interview with Bloomberg using one word: “scary.”

Goldman Sachs forecasts that demand for MLCCs from AI servers will increase at least fourfold by 2030, while industry-wide capacity expands by only about 10% annually. Taiyo Yuden’s stock has risen 163% over the past month, and internal projections for FY2027 anticipate a 50% surge in operating profit to JPY 30 billion.

TDK (6762): A Diversified Player Beyond MLCCs

$TDK Electronics (6762.JP)$ Products include aluminum electrolytic capacitors, film inductors, optical transceiver modules, HDD heads, and secondary batteries for AI data centers.

FY2026 projected revenue is JPY 2,504.8 billion, with operating profit of JPY 272.4 billion, yielding an operating margin of approximately 11%. The company plans to expand AI-related sales at a compound annual growth rate (CAGR) of 25%–30% through FY2031, targeting a tenfold increase in passive component sales for AI data centers. However, given that the core of overall revenue still stems from energy applications (lithium-ion battery business), the earnings elasticity driven by AI remains relatively moderate compared to the other two major electronic components manufacturers.

Ibiden (4062): Dominant Monopolist in GPU Packaging Substrates

$Ibiden Co., Ltd. (4062.JP)$ The company produces FC-BGA (Flip-Chip Ball Grid Array) packaging substrates, which serve as the critical carrier for NVIDIA GPUs and data center CPUs. Ibiden is estimated to hold a 70%–80% market share in high-end AI server packaging substrates. An industry adage states: “Without Ibiden and Shinko Electric, the world cannot produce high-performance server processors.”

FY2026 projected revenue is JPY 415.0 billion, with operating profit of JPY 61.0 billion, yielding an operating margin of approximately 13%. The company plans to execute an ultra-large-scale capital expenditure program of JPY 500.0 billion over the next three years, focusing on expanding its Ono and Kawanishi plants, with the goal of permanently securing its global leadership position in high-end AI packaging substrates.

In April 2026, it was the best-performing stock year-to-date among global foreign-owned IT equities. In February, the company completed a JPY 52.47 billion equity offering, with all proceeds allocated to capacity expansion.

Shinko Electric (6967): Japan’s Second Pillar in Packaging Substrates

Shinko Electric, alongside Ibiden, forms Japan’s ‘twin pillars’ in high-end packaging substrates, together dominating 70%–80% of the global high-end substrate market. Its key customers include Intel and AMD. The company maintains a stable operating profit margin above 10%. It should be noted that its parent company,$Fujitsu (6702.JP)$is currently advancing its privatization in coordination with consortia such as JICC (via a tender offer), and secondary market trading activities should closely monitor related announcements.

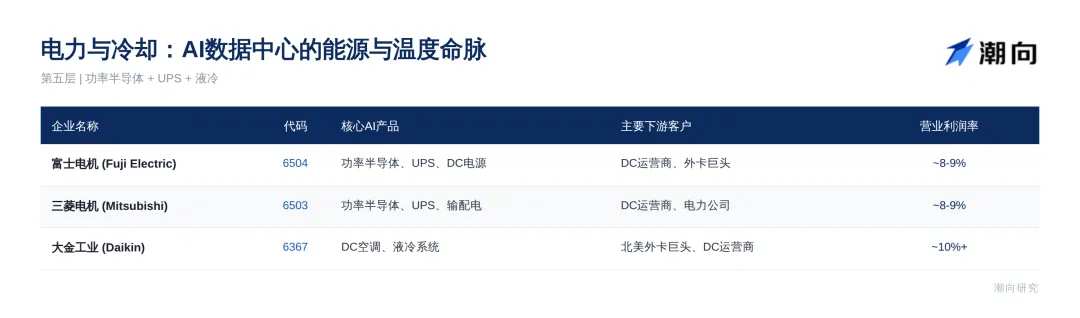

Layer 5: Power and Cooling

The power consumption per rack in AI data centers is several times higher than that in traditional data centers. This creates three new bottlenecks: ultra-high-capacity power distribution and uninterruptible power supply (UPS) systems, power semiconductors responsible for high-frequency power conversion, and liquid cooling systems and precision air conditioning units used to cool servers and chips. Approximately 30%–40% of a data center’s electricity is consumed by cooling systems, making power and cooling the ultimate constraints on scaling AI computing capacity.

This layer is often overlooked, yet it represents another area where Japanese companies stand to benefit significantly.

$Fuji Electric (6504.JP)$: A comprehensive provider of DC power supplies, UPS systems, and power semiconductors

Fuji Electric offers a full range of products, including high-power UPS systems, data-center-specific high- and low-voltage power distribution systems, and core power semiconductors for power conversion (IGBTs and SiC modules). According to its latest financial report, operating profit for April–December 2025 increased by 8% year-over-year, marking the fifth consecutive year of record highs. The Infrastructure and Power Systems segment saw double-digit growth in both revenue and profit, driven by surging data center orders. The company is expanding its data center power supply production capacity to 1.7 times its original level, maintaining an overall operating profit margin of 8%–9%.

Mitsubishi Electric (6503.JP): A national leader in heavy electrical equipment

Mitsubishi Electric holds a dominant position in high-voltage power semiconductors (IGBTs/SiC) and large-scale industrial-grade UPS systems. Its UPS business serving overseas markets is enjoying a long-term upcycle, with products comprehensively integrated across the entire power chain of AI data centers. The company reports consolidated revenue of JPY 5.5 trillion and maintains an overall operating profit margin of 8%–9%.

$Daikin Industries (6367.JP)$: The world’s leading air conditioning manufacturer enters data center liquid cooling

Daikin Industries, the world’s largest air conditioning company, is now transferring its core technologies into data center cooling. Its chip-level direct liquid cooling system employs a proprietary negative-pressure circulation technology that makes fluid leakage extremely unlikely—even in the event of pipe damage—offering exceptional protection for server hardware. In 2025, it acquired U.S.-based DDC Solutions and Chil-Dyne in succession, fully integrating its AI data center cooling technology chain across North America.

Revenue from its dedicated data center cooling business surged from JPY 23 billion in 2023 to approximately JPY 100 billion in 2025, with a target to exceed JPY 300 billion by 2030. The North American data center cooling market is projected to expand from roughly JPY 1.1 trillion in 2025 to JPY 2.7 trillion by 2030. Daikin has already captured approximately 12% of this market, ranking third in the United States, with a consolidated operating profit margin exceeding 10%.

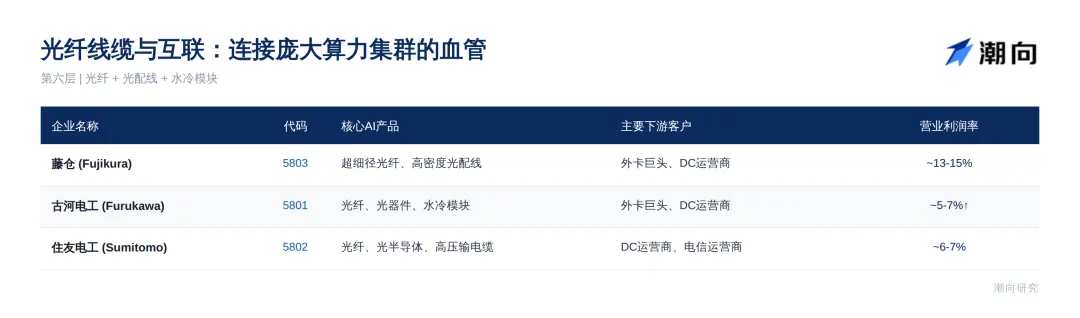

Layer Six: Fiber Optic Cables and Interconnects

AI data centers require ultra-high-speed, ultra-low-latency interconnectivity among tens of thousands of servers, driving explosive demand for high-specification fiber optics, high-density optical distribution systems, and photonic communication components. Japan’s 'Big Three' wire and cable manufacturers (Fujikura (5803.JP), Furukawa Electric, and Sumitomo Electric) have successfully shifted resources over the past few years from low-margin traditional wiring harnesses to high-value-added optical communications and data center businesses, becoming standout performers in both stock price and financial results during the current AI investment cycle.

Fujikura (5803): A Superstar in the Nikkei 225

With 139 years of history and a two-year stock price surge of 1,400%, Fujikura’s ultra-thin, high-density fiber optic cables—featuring Spider Web Ribbon technology—perfectly meet the extremely stringent space and routing requirements of AI data centers. Apple is one of its key customers.

For fiscal year 2026 (ending March 2026), it achieved record-breaking results, with data center-related sales reaching 2.3 times the prior year’s level. The company has repeatedly raised its earnings guidance. Its consolidated return on equity (ROE) stands at approximately 32.5%, and its consolidated operating profit margin has climbed to 13%–15%.

Demand is growing far faster than capacity, and CEO Naoki Okada has publicly acknowledged a state of 'supply shortage.' The company is investing JPY 40 billion to build a new production line at its Sakura plant and has established a wholly owned U.S. subsidiary, Fujikura Optical Cable Systems LLC. On May 12, 2026, its share price surged 11.6% to a record high of JPY 7,624.

Furukawa Electric (5801): An Integrated Player in Fiber Optics, Photonic Components, and Liquid Cooling Modules

Furukawa Electric’s distinct advantage lies in its simultaneous exposure to two cutting-edge segments: high-density cabling for optical communications and chip-level liquid cooling modules for data centers.

The company is experiencing explosive growth. Revenue for FY2025 reached JPY 1,145.9 billion, and the official forecast for FY2026 has been significantly revised upward to JPY 1,300 billion in revenue and JPY 65 billion in operating profit. The liquid cooling module business is projected to scale up from JPY 6 billion in FY2026 to JPY 25 billion in FY2027. The company aims to increase operating profit from its dedicated data center segment to JPY 200 billion by the fiscal year ending March 2031—8.5 times the prior period’s level. With a current operating margin of 5%–7%, the company is on a steep trajectory of margin expansion.

Sumitomo Electric Industries (5802): A comprehensive leader in optical fiber, optoelectronic semiconductors, and backbone power transmission cables

Sumitomo Electric’s product portfolio spans ultra-high-fiber-count optical cables, ultra-high-speed optoelectronic transceiver semiconductor devices, extra-high-voltage power transmission cables (used for cross-regional power delivery to data centers), and third-generation compound semiconductor substrates (GaN/InP).

The company-wide operating margin stands at 6%–7%. As Japan’s undisputed leader in wire and cable manufacturing, Sumitomo Electric has generated excess returns exceeding 90% amid strong dual demand from data centers and optical communications.

When Japanese equities surge

Japanese semiconductor firms did not become strong overnight. Names like Tokyo Electron, Shin-Etsu Chemical, and Murata Manufacturing have resonated in the industry for decades. Yet the Nikkei 225 remained trapped in the shadow of the post-bubble economy for over 30 years, only finally surpassing its 1989 historical peak in 2024. Why is capital now pouring into Japan with such ferocity?

A confluence of three forces.

First, the certainty of AI-related capital expenditures. In 2026, global tech giants are expected to invest approximately USD 800 billion in AI-related capex. On June 2, Alphabet announced plans to issue USD 80 billion in stock to finance its projected 2026 capital expenditures of USD 180–190 billion. This spending will ultimately translate into orders for semiconductor manufacturing equipment, purchases of silicon wafers, consumption of MLCCs, deployment of fiber optic cabling, and installation of UPS and cooling systems—a significant portion of which will flow to Japanese companies.

Second, the amplifying effect of yen depreciation. In June 2026, the USD/JPY exchange rate briefly breached 160. Given that Japanese semiconductor equipment and materials firms earn substantial revenues in U.S. dollars while incurring costs in yen, a weaker yen effectively functions as an implicit export subsidy.

Third, the realization of dividends from corporate governance reforms. One legacy of Abenomics is its push for Japanese companies to enhance shareholder returns. Kioxia has announced a dividend, and Fujikura has introduced restricted stock incentives—moves that would have been unthinkable for Japanese firms in the past. The Tokyo Stock Exchange continues to pressure listed companies to improve their ROE, and foreign investor interest in the Japanese market is structurally rebounding.

The Japanese government is also adding momentum. The semiconductor industry strategy released in March 2026 aims to increase domestic chip production value to JPY 40 trillion (approximately USD 250 billion) by 2040—eight times the JPY 5 trillion recorded in 2020. Rapidus is constructing a 2nm process fabrication plant, targeting mass production by 2027. Taiwan Semiconductor is also expanding its advanced production lines in Japan.

Risks That Cannot Be Ignored

The Nikkei Index has surged 33% year-to-date, far exceeding even the most optimistic forecasts at the beginning of the year. UBS’s year-end 2026 target, set at 54,000 points at the start of the year, has already been surpassed by more than 20%.

Concentration risk. On June 3, when the index hit a new high, just two stocks—Tokyo Electron and Advantest—accounted for approximately 1,100 points of the day’s gain, representing two-thirds of the total increase. Any crack in the AI narrative could trigger a pullback in these high-weight stocks, directly dragging down the index.

Valuation stretch. Tokyo Electron trades at a P/E ratio of approximately 48x, Advantest exceeds 60x, and Kioxia’s trailing P/E is nearing 77x. Fujikura and TAIYO YUDEN have seen their share prices surge well ahead of fundamentals due to extremely elevated near-term expectations. Any shortfall during the earnings delivery period could trigger sharp valuation corrections driven by expectation gaps.

Yen reversal. The Bank of Japan is expected to hike rates further in 2026, and real wages have posted positive growth for four consecutive months. A rapid appreciation of the yen would compress profit margins for export-oriented companies.

Cyclicality of AI capital expenditure. Once global payment giants enter a phase of capital spending adjustment, orders for highly cyclical semiconductor equipment and upstream components will face sharp periodic downturns. Historically, every major wave of IT infrastructure investment—from fiber optics during the dot-com bubble to servers in the early days of cloud computing—has gone through cycles of euphoria followed by digestion.

Interpretation

The essence of Japan’s AI semiconductor rally is a revaluation of 'deep infrastructure' assets.

Over the past two years, market valuations of AI have focused on the most visible segments: NVIDIA designing chips, Taiwan Semiconductor manufacturing them, and ASML Holding supplying the 'shovels.' Yet the AI supply chain is far longer and deeper. From silicon wafers to photoresists, from testing equipment to MLCCs, from UPS power systems to liquid cooling solutions, and from fiber optic cables to packaging substrates—every link faces bottlenecks, and each bottleneck represents pricing power. Japanese firms happen to sit at the very top of this chain, occupying positions that are exceptionally difficult to replace.

From an investment certainty perspective, the highest tier belongs to 'technology monopolies,' with representative companies including Lasertec (holding 100% market share in EUV inspection), Disco (near-monopoly in HBM thinning equipment), Advantest (dominant market share in AI testing equipment), and Ibiden/Newly Electronics (the leading duopoly in high-end packaging substrates). These firms are virtually irreplaceable in the value chain and possess genuine global pricing power. Demand for MLCCs, wire and cable, and precision air conditioning has also surged, but these sectors face some degree of competition and are more susceptible to supply-demand dynamics and production ramp-up cycles.

Kioxia’s 3,500% surge appears on the surface to reflect soaring NAND prices, but more fundamentally signals the market’s belated recognition that memory has become one of the key bottlenecks constraining AI computing capacity. The sharp rallies in Murata Manufacturing and Taiyo Yuden underscore a hard reality: an AI server requires several times more MLCCs than a conventional server, and global production capacity is expanding far too slowly to meet surging demand.

For investors, Japan’s AI semiconductor sector offers a fundamentally different way to gain exposure compared to U.S. tech stocks. Rather than betting on which AI company will emerge victorious, you only need to believe one thing: regardless of who wins the AI race, they will all need Japanese equipment, materials, and components to compete.

Annual gains of 33% won’t recur every year. However, viewed through the lens of the industrial cycle, the build-out of AI infrastructure is far from complete, and Japanese firms’ structural position in the global semiconductor supply chain is unlikely to be undermined in the near term.

Whoever controls the 'means of production' in the AI era—Japan remains at the table.

Disclaimer: This article is provided solely for informational purposes and investment research reference and does not constitute any investment advice. The stock market involves risks; please invest with caution. Specific stocks mentioned herein are included strictly for industry analysis and do not represent recommendations to buy or sell. Data sources include the latest corporate financial reports, Yahoo Finance, Investing.com, StockAnalysis, Bloomberg, and other publicly available information.

Editor /rice