Goldman Sachs believes market expectations for next year's capital expenditures by hyperscale cloud computing companies are overly conservative. The consensus forecast stands at $920 billion, while the firm’s base-case scenario is $1.1 trillion, with an upside scenario as high as $1.4 trillion.

Meanwhile, valuations of AI infrastructure stocks have risen to their highest level since the launch of ChatGPT, yet actual enterprise adoption of AI remains weak, and a token price war is intensifying industry uncertainty.

“Market expectations for hyperscalers’ capital expenditures in 2027 are overly conservative.”

On June 12, Goldman Sachs economist Ryan Hammond significantly raised his forecast for next year’s hyperscaler capital expenditures in a research report titled “More AI Capex, More Volatility”: $1.1 trillion under the base case scenario and as high as $1.4 trillion under an extremely optimistic scenario.

On June 12, Goldman Sachs economist Ryan Hammond significantly raised his forecast for next year’s hyperscaler capital expenditures in a research report titled “More AI Capex, More Volatility”: $1.1 trillion under the base case scenario and as high as $1.4 trillion under an extremely optimistic scenario.

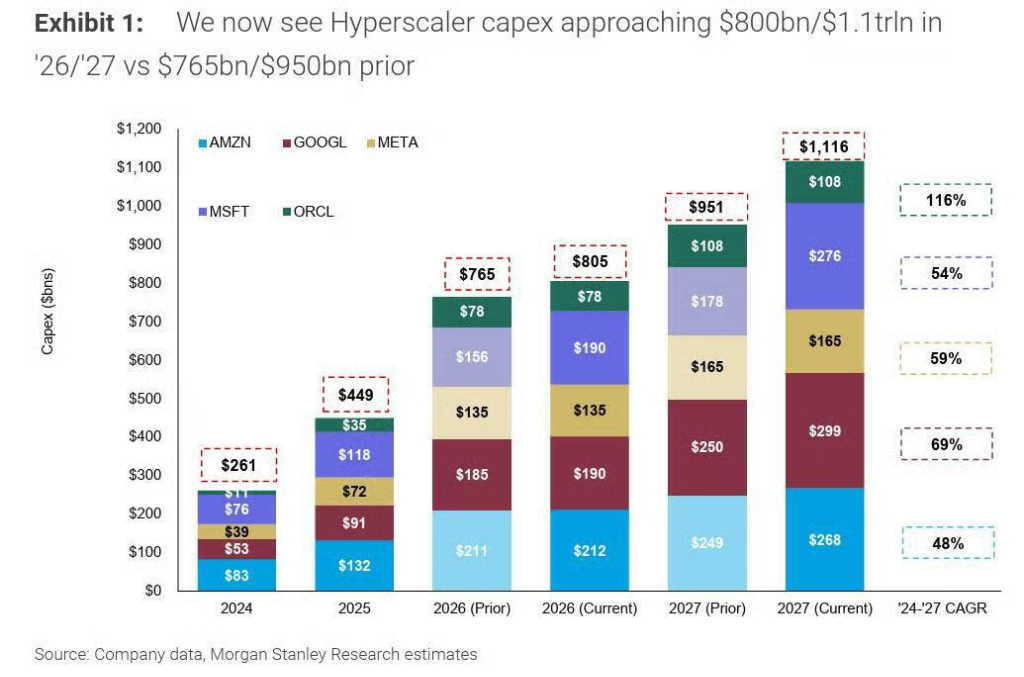

This report comes against the backdrop that just a few weeks earlier, major hyperscalers—namely tech giants Microsoft, Google, Amazon, and Meta—had successively released their Q1 earnings and capital expenditure guidance. According to Morgan Stanley, the combined 2027 capital expenditure outlook for these companies has surged from $950 billion as of Q4 2025 to over $1.1 trillion, marking a single-quarter upward revision of more than 30%.

Goldman Sachs’ three-tier forecast: from $920 billion to $1.4 trillion

The consensus among mainstream analysts currently stands at approximately $920 billion for hyperscalers’ 2027 capital expenditures, implying a sharp deceleration in growth from 84% in 2026 to 22%.

Goldman Sachs disagrees with this figure.

Hammond’s analytical framework posits that if incremental investment in AI infrastructure reaches 2% to 3% of GDP—comparable to historical build-out cycles in the railroad and automotive industries—capital expenditures in 2027 would amount to approximately $1.1 trillion, implying 45% growth.

Under a more extreme optimistic scenario, factoring in both hyperscalers’ own cash flow generation capacity and the financing capacity of the investment-grade corporate bond market, capital expenditures could reach as high as $1.4 trillion, corresponding to 89% growth.

Valuations have reached their highest level since the launch of ChatGPT.

The upward revision in capital expenditure expectations has directly driven valuation expansion in the AI infrastructure sector.

Its data show that the median price-to-earnings (P/E) ratio of AI infrastructure stocks has risen to 26x, the highest level since the launch of ChatGPT. Among these, the median P/E ratios for the semiconductor and power (non-utility) sectors have continued to rise year-to-date, while valuation expansion for hyperscale cloud computing companies themselves and storage chip stocks has been relatively limited.

Hammond’s assessment is: "Higher-than-expected capital expenditures imply upside potential in both earnings and share prices of beneficiaries of AI infrastructure in the near term."

However, Hammond also issued a cautionary note: recent valuation expansion and shifts in portfolio positioning suggest heightened volatility ahead. Investors need to strike a balance between 'higher-than-expected capital expenditures,' the possibility of 'slowing capital expenditure growth,' and 'uncertainty around earnings sustainability.'

AI Adoption Data: Strong Hype, Weak Traction

During the Q1 earnings season, approximately 54% of companies mentioned AI and productivity on their earnings calls. However, only 11% quantified productivity gains in specific use cases, and just 2% linked AI-driven productivity improvements directly to earnings—a marginal improvement from last quarter’s figures of 10% and 1%, respectively, indicating little substantive progress.

More direct evidence comes from user surveys: currently, only 12.6% of respondents use AI daily, an increase of just 2 percentage points compared to a year ago. Self-reported cumulative productivity gains among all workers stood at 1.6% a year ago and have now reached 2.2%, reflecting an increase of only about 0.5 to 0.6 percentage points over the past year.

In other words, trillions of dollars in capital expenditures are pouring in, yet actual user adoption depth and productivity returns at the end-user level remain quite limited for now.

The Debate Over Software Stocks’ 'Endgame Valuation'

Hammond also specifically addressed the valuation rationale for the software sector.

The P/E ratio for software stocks peaked at 39x last year, fell to 21x in March this year, and has since rebounded to 25x, though significant divergence persists across sub-sectors.

Using a discounted cash flow model, Hammond estimated that at the beginning of the year, approximately 85% of the software sector’s present value stemmed from 'terminal value'—the discounted expectation of profits far into the future. This implies that even a 'modest' shift in market assumptions regarding long-term growth rates and profit margins for software companies could lead to significant valuation volatility—an explanation for the pronounced swings in software stock valuations seen this year.

The core debate centers on whether AI serves as an enabler or a disruptor for software companies. Will the emergence of low-cost competitors continue to suppress revenue growth and profit margins for incumbent software firms? This ongoing debate will continue to drive performance divergence within the sector.

Token price war: Another variable that cannot be ignored

Concurrent with the release of this report, another development has been unfolding in the market: a 'race to the bottom' in token pricing between OpenAI and Anthropic.

This price war occurs against a backdrop where some enterprises are already exhibiting 'tokenmaxxing'—excessive token consumption. For instance, Uber exhausted its entire annual AI budget within a single quarter. As token prices continue to decline, large language model providers will face mounting revenue pressure, putting their ability to sustain commitments to massive capital expenditures to the test.

This suggests that there could be a substantial gap between projected capital expenditure figures and actual implementation.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/melody