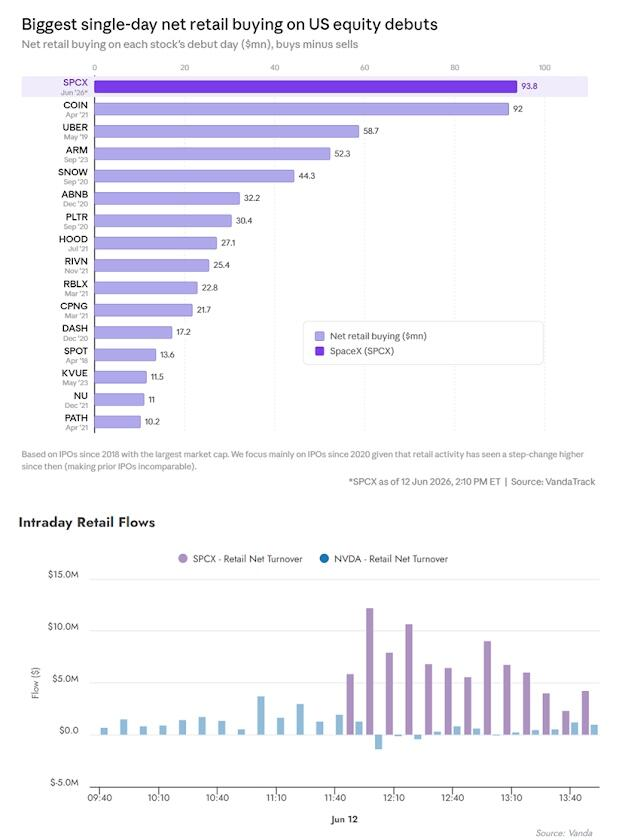

On Friday, the S&P 500 rose 0.5%, the Nasdaq Composite gained 0.31%, and the Dow Jones Industrial Average climbed 0.7%. SpaceX completed its Nasdaq listing on the same day, with its shares surging approximately 19%, making it the market's focal point. The Mag 7 underperformed the broader market, while memory chip stocks were mixed. Oil prices pared losses to close down 2.3%, and spot gold traded sideways.

Expectations for a U.S.-Iran peace agreement continued to intensify, pressuring oil prices lower. Cooling inflation expectations lifted U.S. equity indices, marking their tenth consecutive weekly gain, while Treasury yields declined and the dollar weakened.

On Friday, news of U.S.-Iran negotiations dominated market sentiment:

Ahead of the U.S. market open, rumors that a U.S.-Iran “peace agreement” could be signed as early as Sunday triggered a sharp drop in oil prices during Asian trading hours. However, after some Iranian officials denied plans to relinquish control over the Strait of Hormuz, oil prices rebounded from their intraday lows.

On Friday, Trump posted on social media that the draft agreement published by Iranian media had “nothing to do” with any written understanding reached between the U.S. and Iran and was factually incorrect, causing market sentiment to swing once again.

During early U.S. trading hours, according to China Central Television (CCTV), Iranian Foreign Minister Abbas Araghchi stated that the Islamabad Memorandum of Understanding was "closer than ever" to being finalized, prompting a sharp decline in oil prices and extending the gains in U.S. equity indices.

Iranian Foreign Ministry spokesperson Baghaei indicated that Tehran and Washington have already reached understandings on most issues, and Iran is currently finalizing the consolidated text of the memorandum of understanding.

During midday U.S. trading, CCTV reported that Pakistani Prime Minister Shehbaz Sharif stated that "the final agreed-upon text of the peace agreement has been completed," and both countries are advancing toward implementation. Oil prices extended their losses.

During U.S. trading hours, equities briefly dipped following Trump’s criticism of Iran for leaking details of the agreement. However, reports emerged that the UAE had agreed to unfreeze substantial funds for Iran, with an initial tranche of approximately USD 3 billion already transferred, further bolstering optimism about a deal.

Bloomberg strategist Kristine Aquino noted that the equity rally sparked by the latest comments from Iran’s foreign minister suggests markets still have room to price in a concrete agreement, though the magnitude of such reactions may be limited.

Chevron CEO Mike Wirth warned that despite rising volumes of Persian Gulf oil shipments passing through the Strait of Hormuz, global oil inventories are declining to “alarming” levels.

Mike Wirth said:

If you look at either products or crude oil, we’ve moved from comfortable inventory levels typical of normal times to inventory levels that will soon become uncomfortable.

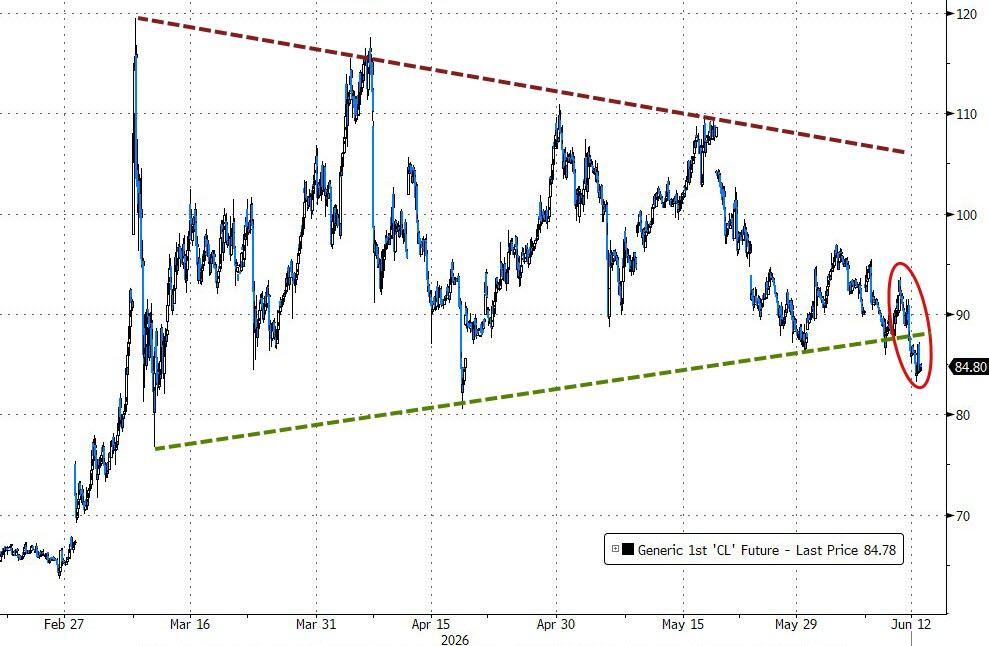

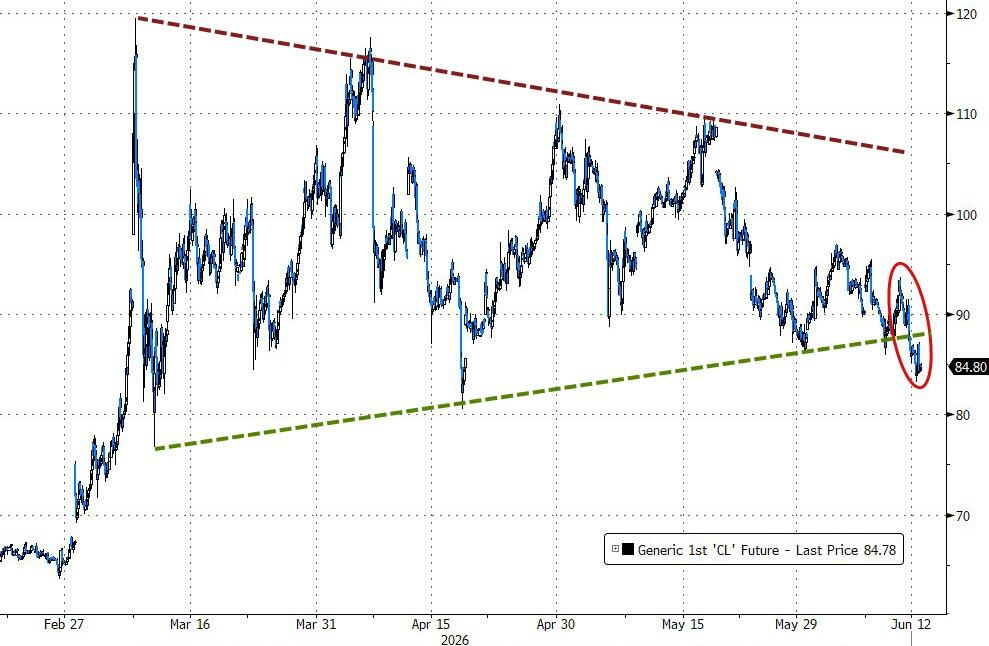

Crude oil prices declined on the day, marking the third weekly drop in the past four weeks, though they remain above pre-war levels.

According to Polymarket, the probability of a U.S.-Iran deal being reached by the end of June has surged to 43%, up from previously less than 30%.

On Friday, the S&P 500 rose 0.5%, the Nasdaq gained 0.31%, and the Dow Jones Industrial Average increased by 0.7%. $SpaceX (SPCX.US)$ It completed its Nasdaq listing on the same day, with its share price surging approximately 19%, making it the market’s focal point.

Amid the 'siphoning effect,' shares of other space-related companies faced a wave of selling, such as $Rocket Lab (RKLB.US)$Down more than 10%,$Redwire (RDW.US)$ dropping more than 11%, $AST SpaceMobile (ASTS.US)$ and falling over 15%.

According to Vanda Research, SpaceX became the most purchased stock by retail investors on the day, with net retail buying exceeding 3.5 times that of NVIDIA—the second most bought stock. Retail trading volume reached $453 million, accounting for approximately 4% of total single-stock retail trading volume that day.

SpaceX is thus poised to become the IPO with the highest level of retail investor participation in recent years, far surpassing the record $92 million in net retail buying during Coinbase's April 2021 listing and exceeding the first-day retail participation of all major IPOs over the past six years.

Although U.S. equities closed higher, performance diverged significantly within the week. The S&P 500 and Dow Jones Industrial Average posted slight weekly gains, the Nasdaq rose by approximately 2%, and small-cap stocks led the rally, with the Russell 2000 Index gaining more than 4% for the week.

The S&P 500 has closed higher in ten out of the past eleven weeks, partly driven by substantial short-covering activity on Thursday and Friday.

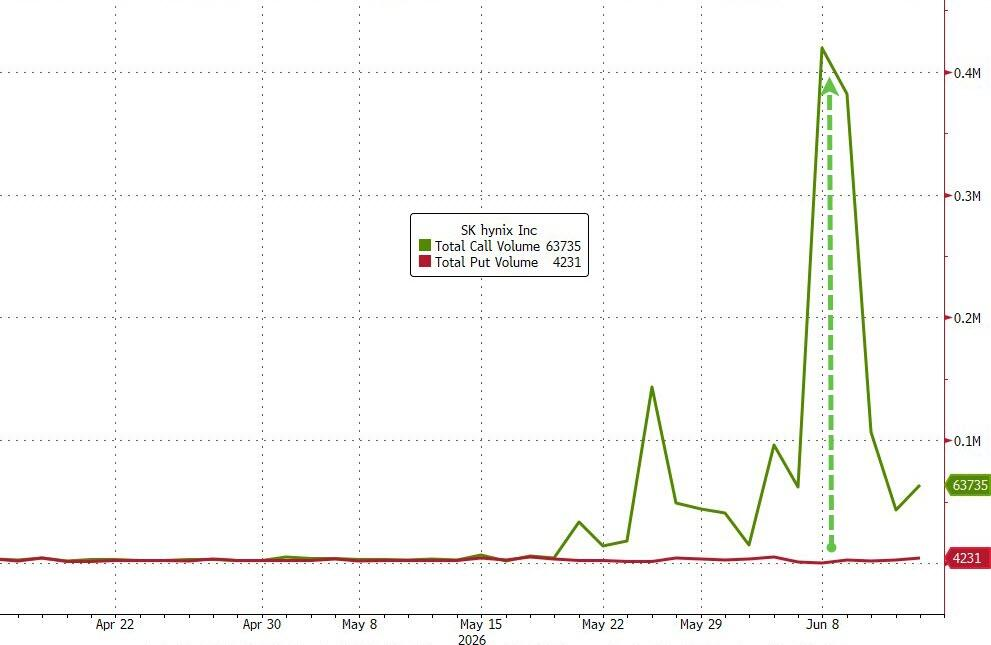

There was notable divergence within the technology sector. Semiconductor stocks staged a strong rebound this week, erasing last week’s losses, and SK Hynix saw a call-to-put options volume ratio as high as 100-to-1, reflecting extremely bullish market sentiment.

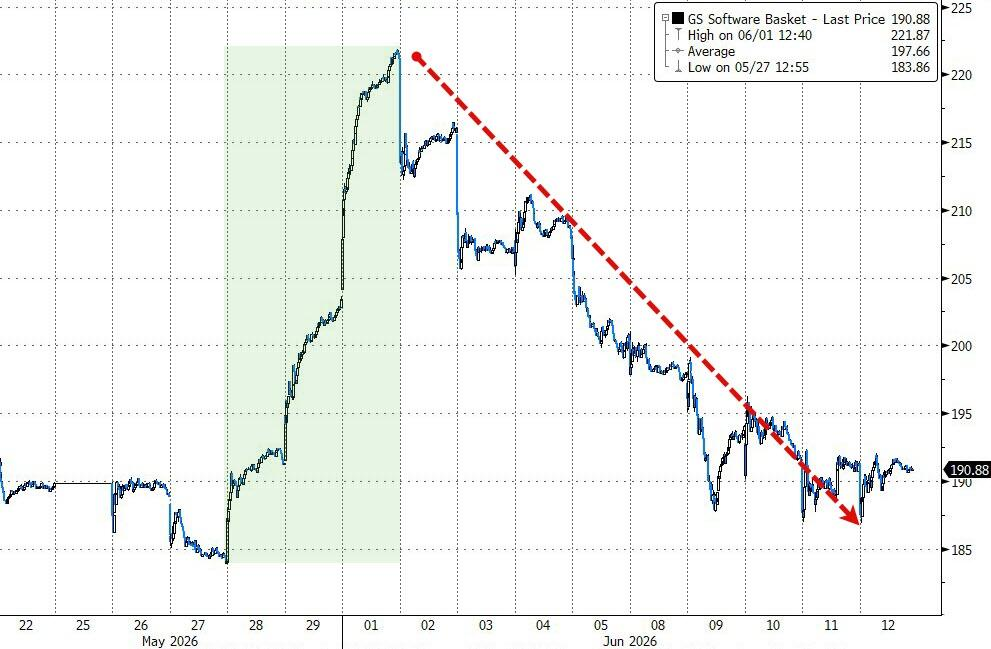

In contrast, software stocks suffered sharp declines, $Adobe (ADBE.US)$ 、 $ServiceNow (NOW.US)$ with multiple individual stocks falling more than 10% during the week; Adobe faced additional pressure due to news of its CFO’s departure.

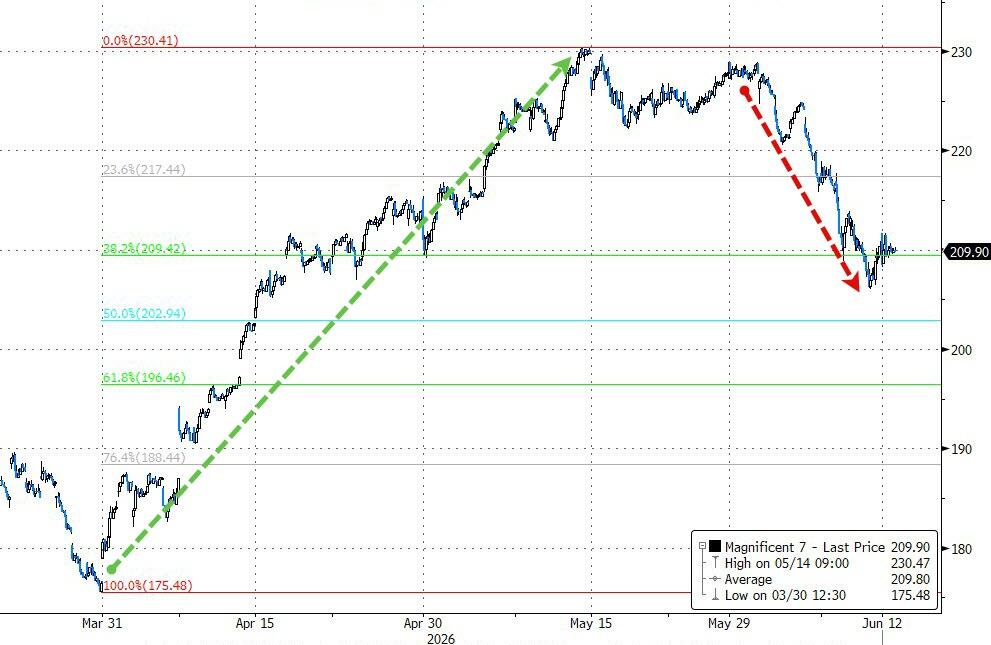

AI-related mega-cap tech stocks also underperformed, $Amazon (AMZN.US)$ with Alphabet (Google’s parent company), $Microsoft (MSFT.US)$ and others each declining between 2% and 7% for the week, causing the Mag 7 to lag behind the broader S&P 493 constituents.

The Mag 7 have now retraced more than the 38.2% Fibonacci level from their post-ceasefire rally highs.

Goldman Sachs strategist Chris Hussey likened the current market to a cha-cha—tensions between growth and interest rates have not been resolved but are merely shuffling back and forth without making significant progress. He advised investors to focus on three areas:

First, individual stocks with strong earnings;

Second, using AI infrastructure companies as a hedge against volatility;

Third, portfolios of stocks benefiting from earnings tailwinds but exhibiting low correlation with AI-related trades.

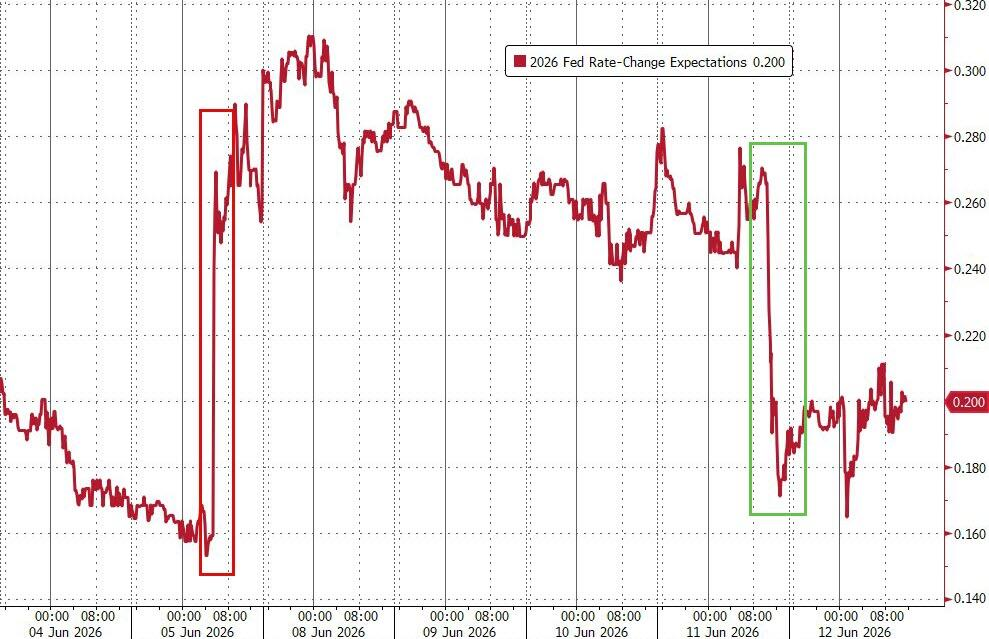

With oil prices declining, market concerns over inflationary pressures have eased somewhat, leading to a sharp retreat in Federal Reserve rate-hike expectations, effectively unwinding most of the hawkish repricing triggered last week by strong nonfarm payroll data.

The yield on the 10-year U.S. Treasury note declined by approximately 10 basis points over the week, closing Friday at 4.48%; the 30-year yield fell back below the 5.00% mark.

The U.S. Dollar Index posted its largest weekly decline since early May, erasing about half of last week’s gains following the nonfarm payrolls report, and ended Friday essentially flat at 99.75. The dollar-yen exchange rate remained near 160.20, close to the intervention warning level closely watched by markets.

All three major U.S. equity indices closed higher on Friday. Mega-cap AI-related tech stocks underperformed this week, with Amazon, Alphabet (Google’s parent company), and Microsoft all falling between 2% and 7%. The Mag 7 as a group underperformed the broader S&P 493 index.

U.S. benchmark indices:

The S&P 500 index rose 37.16 points, or 0.50%, closing at 7,431.46.

The Dow Jones Industrial Average gained 353.51 points, or 0.70%, closing at 51,202.26.

The Nasdaq Composite rose 79.184 points, or 0.31%, to close at 25,888.844. The Nasdaq 100 gained 189.772 points, or 0.64%, closing at 29,635.948.

The Russell 2000 Index rose 0.79% to close at 2,943.992.

The CBOE Volatility Index (VIX) declined 9% to close at 17.69.

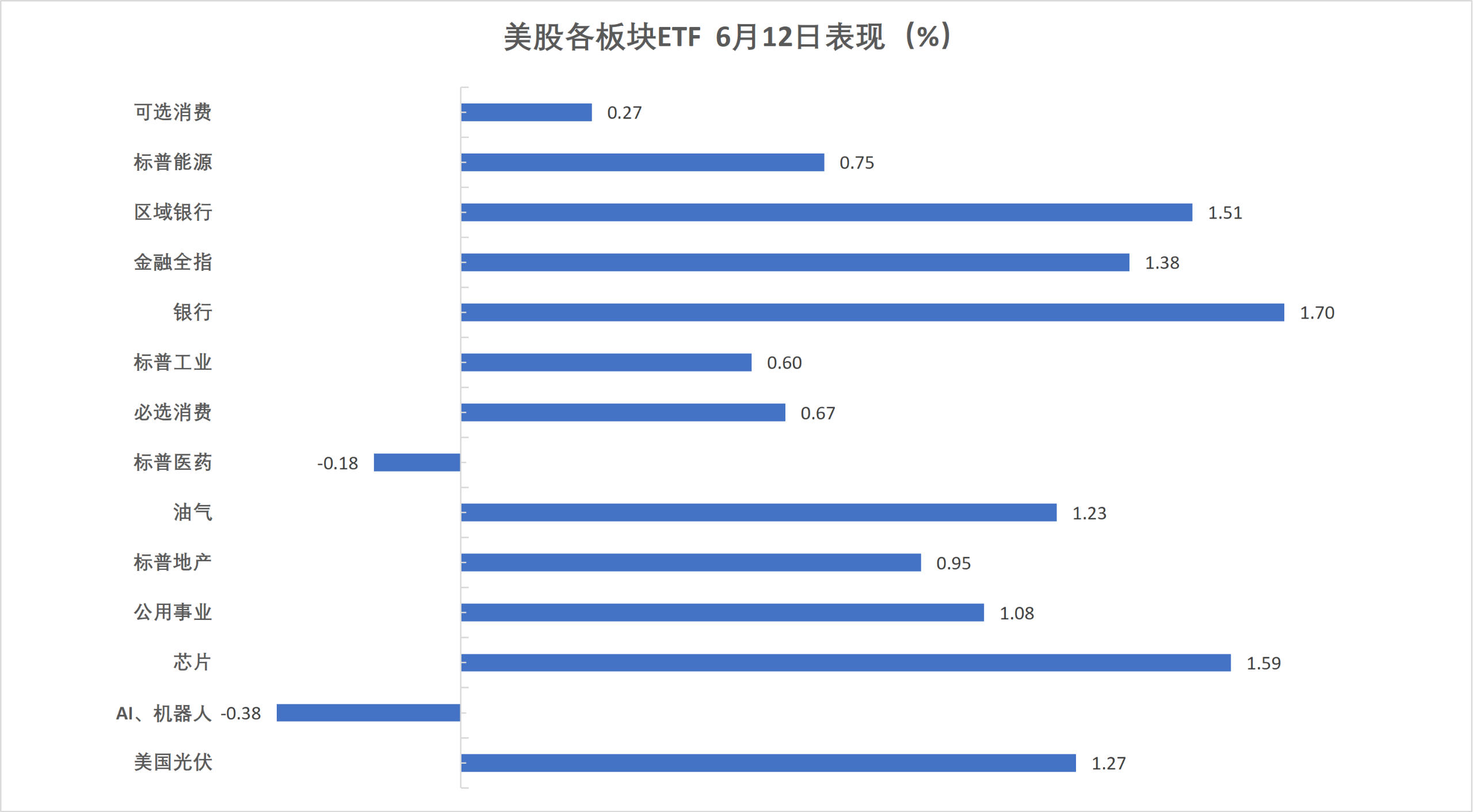

U.S. stock sector ETFs:

Most U.S. sector ETFs ended higher, with the Global Airlines ETF up 1.93%. Semiconductor, regional banking, banking, financials, and utilities ETFs rose by as much as 1.72%.

Mag 7:

The Mag 7 index fell 0.23% to close at 210.45, marking a weekly decline of 2.86%. It trended lower from June 8 to June 11, mostly holding steady around the 210 level during that period.

$Apple (AAPL.US)$ down 1.52%, Amazon down 1.23%, Meta down 0.26%, Microsoft up 0.10%, $NVIDIA (NVDA.US)$ up 0.16%, Google A up 0.53%, $Tesla (TSLA.US)$ up 1.82%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ rose 1.52% to close at 13,371.47 points.

$Taiwan Semiconductor (TSM.US)$ gained 0.65%, bringing its weekly gain to 2.32%. $Advanced Micro Devices (AMD.US)$ surged 4.73%, for a weekly gain of 9.69%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed up 0.48% at 6,326.73 points, down 0.56% for the week, showing an overall W-shaped pattern.

Among actively traded Chinese stocks, JinkoSolar closed up 6.5%, Canadian Solar rose 5.8%, and ASE Technology gained 4%, $Li Auto (LI.US)$ up 3.9%, New Oriental advanced 3.5%, while Meituan-W declined more than 1%.

Other individual stocks:

$Circle (CRCL.US)$ dropped 5.85%.

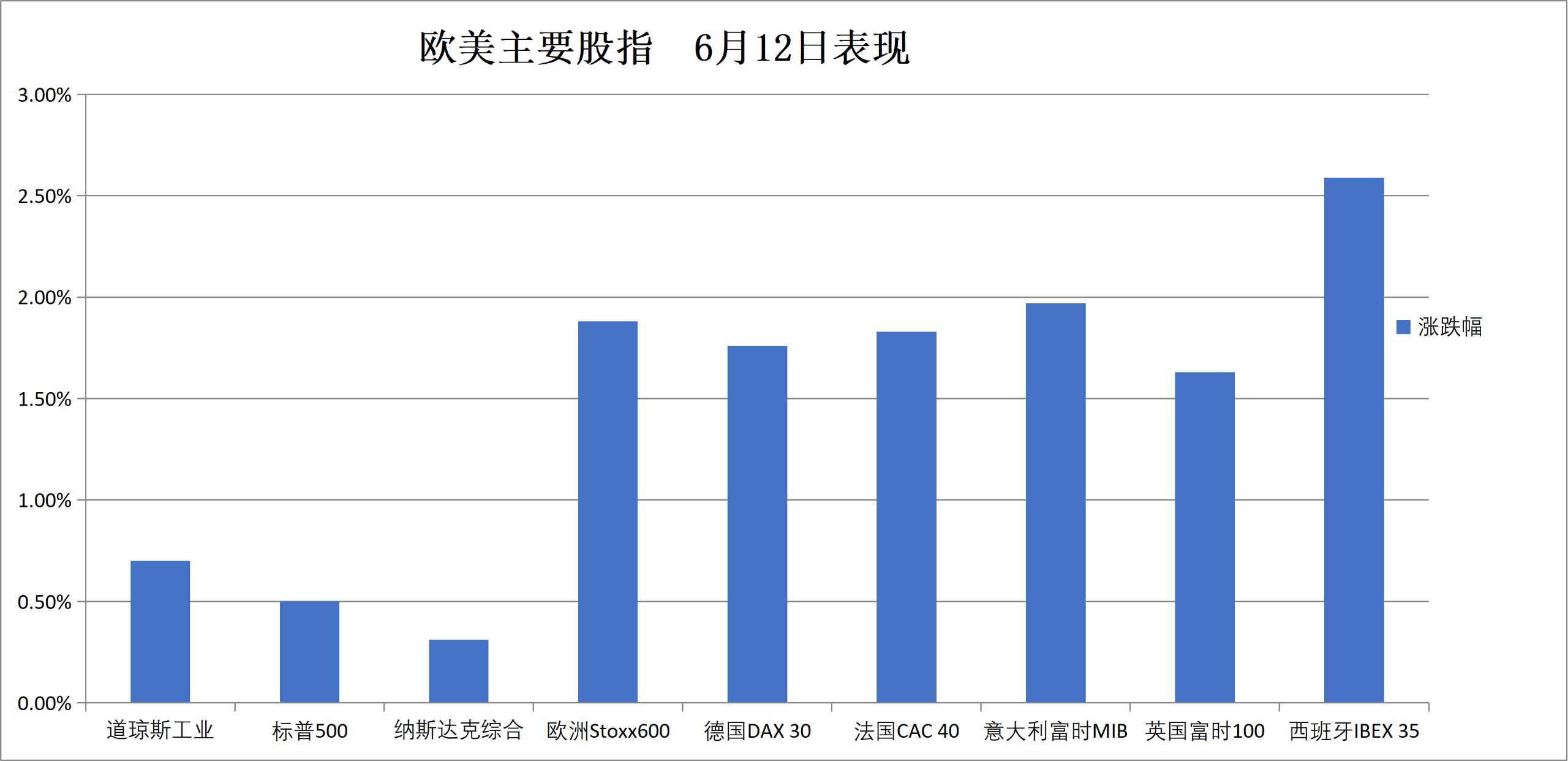

The Eurozone blue-chip index hit a record closing high, with the travel sector gaining over 3.8% this week and the oil & gas sector falling more than 1.2%. Italy’s stock market closed up nearly 2%, alongside the Netherlands and Spain, whose indices also reached record closing highs.

Pan-European Index:

The STOXX Europe 600 Index closed up 1.88% at 633.21 points, posting a weekly gain of 1.69%.

The EURO STOXX 50 Index closed up 2.16% at 6,187.63 points, for a weekly gain of 2.07%.

Major Stock Indexes Around the World:

Germany's DAX 30 Index closed up 1.76% at 24,635.30 points, down 0.50% for the week, forming an overall M-shaped pattern.

France's CAC 40 Index closed up 1.83% at 8,350.87 points, gaining 1.61% for the week.

The UK's FTSE 100 Index closed up 1.63% at 10,471.72 points, rising 1.00% for the week.

Sector and individual stock performance:

Among Eurozone blue-chip stocks, Deutsche Bank rose 6.60%, Adyen gained 5.50%, Spain’s Banco Santander climbed 5.29%, BNP Paribas advanced 5.17% (ranking fourth), and Italy’s Intesa Sanpaolo increased by 4.30%.

Among all constituents of the STOXX Europe 600 Index, Acciona surged 10.37%, Nokia rose 10.06%, TUI Group gained 8.69%, KGHM Polska Miedź increased by 8.10%, and ING Groep advanced 8.03%.

For the week, sector-wise, the STOXX 600 Personal & Household Goods Index rose 5.00% (continuing its upward trend), the Travel & Leisure Index gained 3.86% (breaking out of a prior sideways movement and moving higher on June 12), and the Food & Beverage Index increased by 3.64%.

According to the U.S. Commodity Futures Trading Commission (CFTC) commitment of traders report, in the week ending June 9, speculative net long positions in Brent and WTI crude oil declined by 43,742 contracts to 321,610 contracts, reaching a 19-week low.

Crude Oil:

WTI crude oil futures for July delivery fell $2.83, or more than 3.22%, closing at $84.88 per barrel, down 6.25% for the week.

Brent August crude futures settled down $3.05, or more than 3.37%, at $87.33 per barrel, posting a weekly decline of nearly 6.19%.

Abu Dhabi Murban crude futures fell 3.74% to $83.99 per barrel, marking a weekly loss of 7.38%.

Natural Gas:

NYMEX July natural gas futures settled at $3.12 per million British thermal units (MMBtu), recording a weekly decline of over 3.37%.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen