The U.S. National Oceanic and Atmospheric Administration (NOAA) has officially declared the onset of an El Niño event, with models indicating a 63% probability that it will develop into an "extremely strong" episode. This phenomenon has cascading effects on agriculture, food inflation, coal demand, hydropower supply, and the insurance sector, exerting upward pressure on prices of corn, rice, wheat, and sugar. India’s sugar output could decline by approximately 3 to 8 million metric tons year-over-year, triggering significant price volatility.

What could be the strongest El Niño event in decades is taking shape, and its potential impacts on global agriculture, inflation, and commodity markets are already coming into investors’ focus.

According to Chasing Storms Trading Desk, on June 12, UBS Group’s Global Sustainable Development Research team hosted an expert conference call featuring Dr. Tim Stockdale, Chief Scientist at the European Centre for Medium-Range Weather Forecasts (ECMWF), who provided an in-depth analysis of the latest developments in the El Niño phenomenon and its market implications.

Just one day before the call, on June 11, the U.S. National Oceanic and Atmospheric Administration (NOAA) officially declared the onset of El Niño and forecast that it would strengthen further to a moderate or strong intensity by this autumn. This formal classification marks the transition of market concerns from anticipation to reality.

Just one day before the call, on June 11, the U.S. National Oceanic and Atmospheric Administration (NOAA) officially declared the onset of El Niño and forecast that it would strengthen further to a moderate or strong intensity by this autumn. This formal classification marks the transition of market concerns from anticipation to reality.

How strong will this El Niño be?

The formation mechanism of El Niño is relatively straightforward: when a large mass of unusually warm water in the western Pacific shifts eastward toward the central and eastern Pacific, the normal trade winds weaken, upwelling of cold water diminishes, and sea surface temperatures rise further—creating a self-reinforcing cycle. Once a strong event forms, substantial heat is released into the atmosphere and distributed globally.

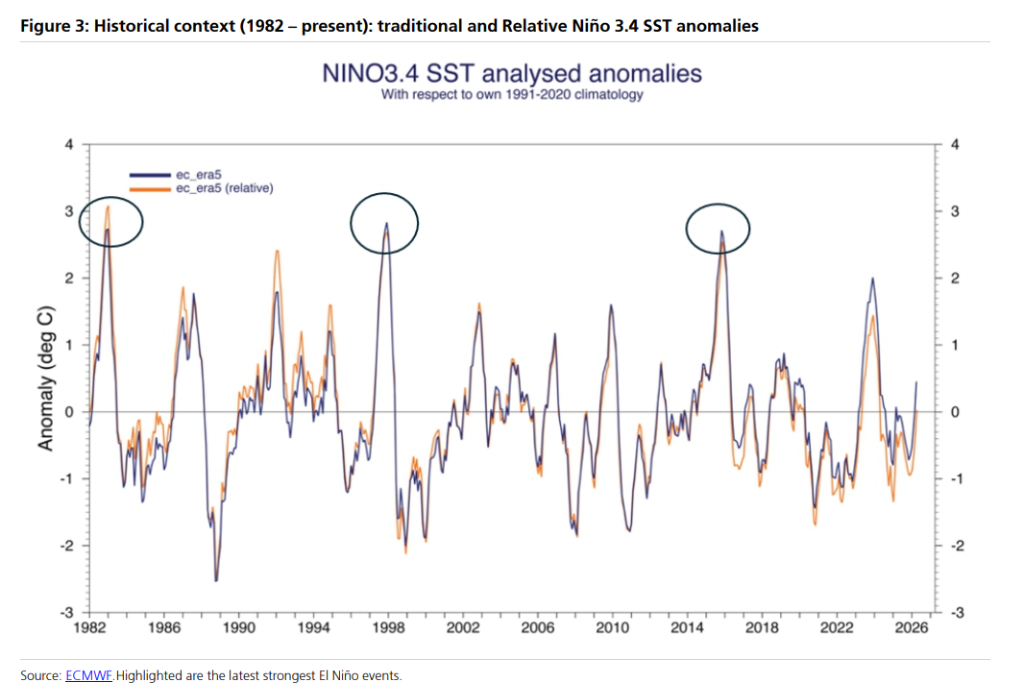

What makes this event exceptional is its scale. During the call, Dr. Stockdale noted that an anomalous warm water mass with temperatures of 30°C or higher has already accumulated in the central tropical Pacific—an area roughly equivalent to the size of the contiguous United States—which he described as “highly unusual.”

ECMWF models send a clear signal: this El Niño event “has virtually no chance of staying below 2°C,” and the median forecast across multiple models projects a peak of 3°C by November. Under standard classifications, a sea surface temperature anomaly of 2°C constitutes an “extremely strong” El Niño event (which typically peaks around December). According to NOAA’s latest data, there is a 63% probability that the event will evolve into an extremely strong one.

It is worth noting that the term “super El Niño,” commonly used in media reports, is not an official designation. Dr. Stockdale specifically clarified this point.

A new indicator: the Relative Niño Index

In addition to traditional sea surface temperature anomaly metrics, ECMWF has introduced an updated “Relative Niño Index,” which measures the temperature difference between the Niño region and the broader tropical region, rather than relying solely on absolute temperatures.

Currently, the relative index is approximately half a degree lower than traditional indicators. There is an important underlying rationale: the atmosphere is more sensitive to temperature gradients than to absolute temperatures. As global warming elevates background temperatures across the entire tropics, traditional indicators may overstate El Niño’s actual atmospheric impact.

However, climate change also introduces an amplifying effect on the opposite side: in a warmer environment, soil dries out more quickly during dry spells, and when it rains, the atmosphere holds more moisture, leading to more intense rainfall. This adds complexity to forecasting.

Agriculture: Overall negative impact, but unevenly distributed

The impact on agriculture is one of the core concerns for markets.

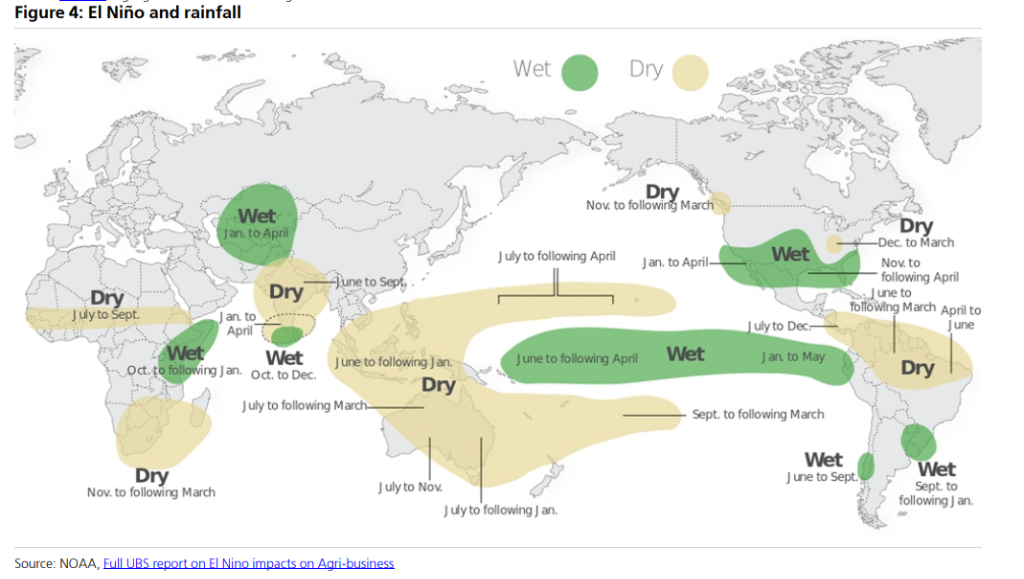

The overall assessment is that El Niño exerts a generally negative effect on global agricultural output, though impacts are uneven—some regions (e.g., those experiencing improved rainfall conditions) may even benefit.

Specifically for major crops: yields of corn, rice, and wheat are typically below normal levels during El Niño years, driving up prices; soybeans are an exception, showing a positive response on a global average basis.

Sugar deserves particular attention. The global sugar market is already tight on supply and demand, with substantial speculative short positions. Should El Niño weaken the Indian monsoon—as currently forecasted at about 92% of normal rainfall—India’s sugar output could decline by 3 to 8 million metric tons year-over-year, triggering significant price volatility.

Inflation transmission: Food prices are the key variable

The transmission channel from El Niño to inflation is clear: weather shocks → reduced agricultural output → higher food prices → broader inflationary pressures.

Empirical analysis shows that the year-over-year change in the IMF’s Global Food Price Index (with a four-month lag) explains approximately 94% of food inflation volatility in emerging markets and about 83% in advanced economies. This implies that once global food prices rise due to El Niño, the resulting inflationary pressure is almost certain to transmit through the system.

Taking India as an example, the risk of weaker monsoons triggered by El Niño could push up food inflation. However, given that food carries a direct weight of approximately 21% in the CPI, the immediate impact of a one-off shock would be relatively limited. The real risk lies in the fact that if the shock persists, second-round effects—namely, the broadening of inflation expectations—would become harder to contain.

Energy and Insurance: Rising coal demand; hurricane season likely to be quieter than usual

El Niño affects energy markets primarily through two opposing channels that nevertheless lead to the same outcome—an increase in thermal coal demand.

On one hand, extreme heatwaves could sweep across Asia, boosting electricity demand—particularly for cooling—and thereby increasing coal consumption and imports, tightening the seaborne market.

On the other hand, El Niño typically reduces rainfall in Latin America and Africa, lowering hydropower generation and creating a supply gap that must similarly be filled by thermal power generation.

The insurance sector faces a relatively favorable short-term window: hurricane activity in the Gulf of Mexico is typically below average during El Niño years, which helps improve insurers’ book values. However, it should be noted that fewer hurricanes do not necessarily imply lower intensity. Additionally, catastrophe losses in Australia are generally lower during El Niño years, but risks from droughts and wildfires rise; parts of South America may experience increased flooding.

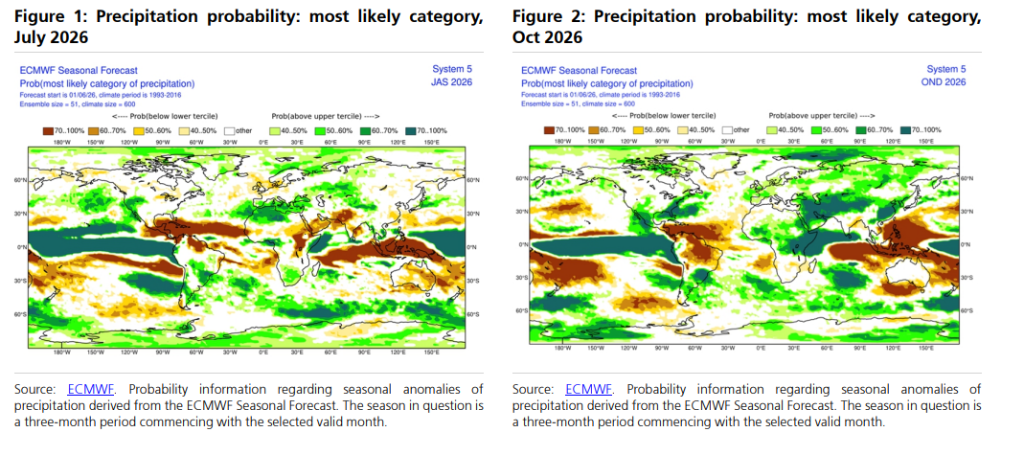

Regional Impacts: Clear signals in the tropics; uncertainty persists in mid-latitudes

Dr. Stockdale emphasized that while each El Niño event is unique, certain consistent patterns tend to emerge. Signals in tropical regions are relatively clear and stable, whereas impacts in mid-latitude regions—such as Europe—are weaker and more difficult to predict.

This implies that for investors in tropical and subtropical regions—including Asia, South America, and Australia—the transmission channels of El Niño impacts can be reasonably assessed based on historical patterns. In contrast, European markets face greater uncertainty, warranting more cautious interpretation of model forecasts.

Editor/Jayden