On Monday, the Nasdaq Composite surged 3%, while the Dow Jones Industrial Average closed at a record high. SPCX jumped 20% in a single day, extending its strong performance following its IPO on Friday. Oil prices declined immediately after news of the agreement emerged, with WTI crude futures plunging more than 4% to settle at $81.49 per barrel—the lowest level in three months.

The United States and Iran reached a framework agreement to reopen the Strait of Hormuz, prompting U.S. equities to rise, oil prices to fall, and both gold and Bitcoin to climb simultaneously.

According to Xinhua News Agency, U.S. President Trump stated on social media on the 14th that the Strait of Hormuz will be reopened for mine-clearance operations following the signing of the U.S.-Iran agreement on Friday, June 19. Iran’s Deputy Foreign Minister also indicated that Tehran would begin announcing immediate and permanent cessation of military operations across multiple fronts—including Lebanon—starting tonight.

The signing of the U.S.-Iran memorandum of understanding has provided a temporary relief signal for global crude oil supply chains, though significant distance remains before full normalization of the situation.

The signing of the U.S.-Iran memorandum of understanding has provided a temporary relief signal for global crude oil supply chains, though significant distance remains before full normalization of the situation.

U.S. officials confirmed that Iranian Parliament Speaker Ghalibaf, regarded as a hardliner within the Supreme Leader’s camp and whose endorsement carries considerable political weight, signed the agreement on behalf of Iran. Details of the memorandum are expected to be released within 24 to 48 hours.

The strait has been closed for over 100 days, and its reopening faces practical operational challenges.

Analysts noted that mine-clearance operations, restoration of shipping confidence, and recovery of production capacity will all take time. Shipowners in Asia and Europe stated they would not hastily resume transit until security assurances are confirmed, with regular shipping operations likely requiring several weeks to normalize.

Deutsche Bank strategist Reid wrote in a report:

“This agreement is very positive news for markets, but difficult negotiations remain over the next 60-day window to ensure the sustainability of peace.”

He also noted that the sanctions waiver provisions related to Iran still require approval from the U.S. Senate.

On Monday, oil prices fell immediately after the announcement of the agreement, with WTI crude futures plunging more than 4% to settle at $81.49 per barrel—the lowest level in three months—though losses were capped as WTI rebounded toward its session high by the close.

Brent crude futures (December 2026 contract) dipped below $80 but stabilized near the 100-day moving average.

Notably, current oil prices remain approximately 20% above pre-war levels.

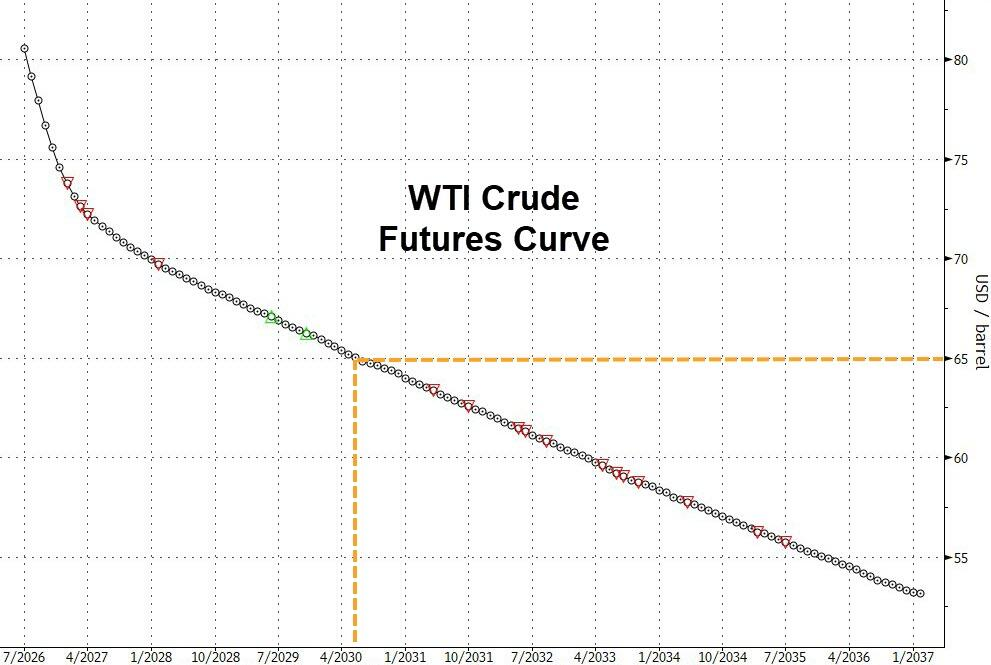

The futures curve suggests that WTI may not return to its pre-war level of $65 until after 2030. According to Jed Graham of Investors.com, a series of geopolitical risks and supply-side challenges could keep oil prices elevated over the long term.

On the inventory front, the restart of supply chains combined with prior drawdowns means that even as production gradually recovers, restocking demand will provide additional price support, limiting further downside for oil prices.

Andrew Ticehurst, strategist at Nomura in Sydney, stated:

The strait is expected to reopen on Friday, and markets may face a period of heightened tension before then. Israel’s actions will also be an unavoidable variable.

In the U.S., the pass-through effect of falling oil prices is already becoming evident. According to GasBuddy data, the national average retail gasoline price has fallen below $4 per gallon for the first time in three months. As lower crude prices transmit through to wholesale and retail levels, pump prices across the country are likely to decline further.

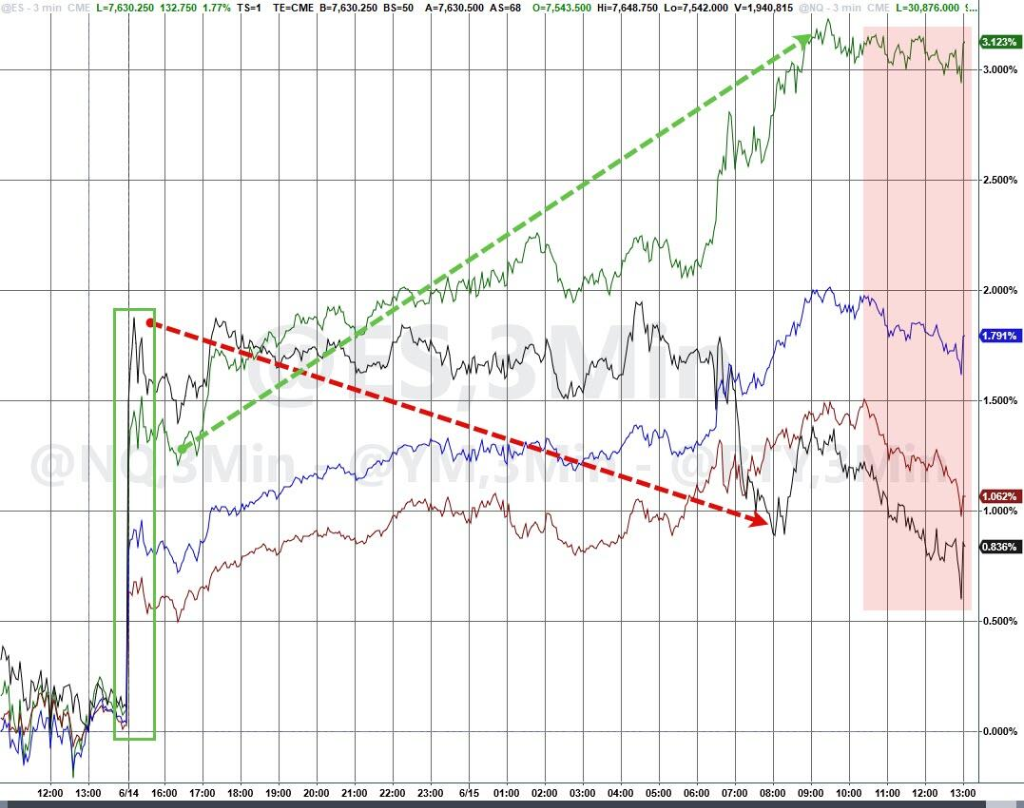

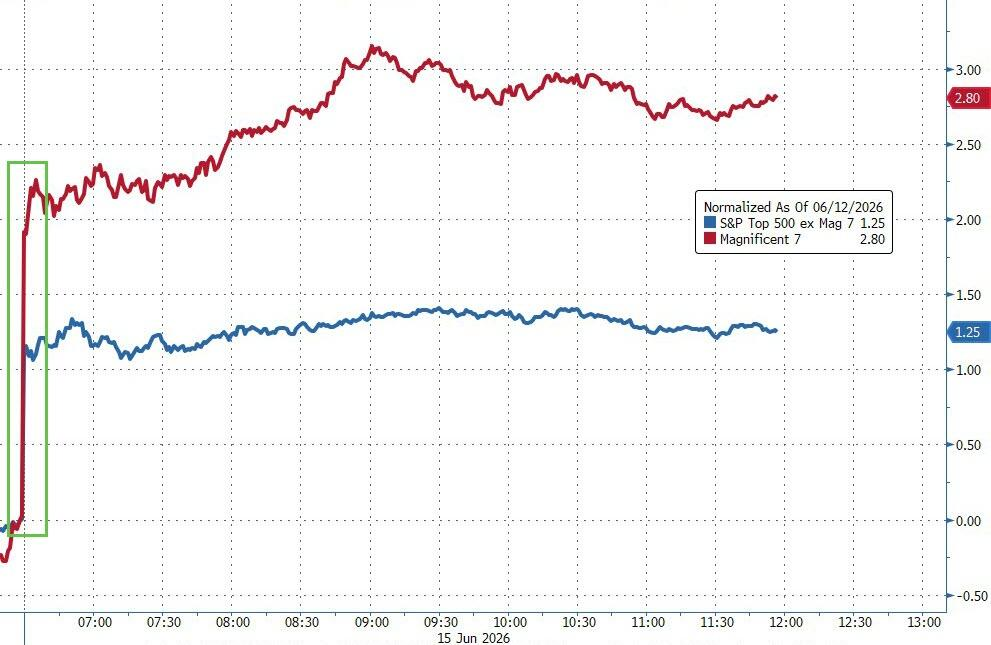

The Nasdaq surged 3% on Monday, while the Dow Jones Industrial Average closed at a record high. Against the backdrop of broad market strength, the technology sector stood out particularly.

The Mag 7 significantly outperformed the S&P 493 constituents during the session, after having been one of the primary sources of fund outflows the previous week.

Chip stocks surged significantly, with memory chip shares hitting record highs; semiconductor and semiconductor equipment segments tied to AI infrastructure also rose in tandem, emerging as one of the market’s most elastic sectors.

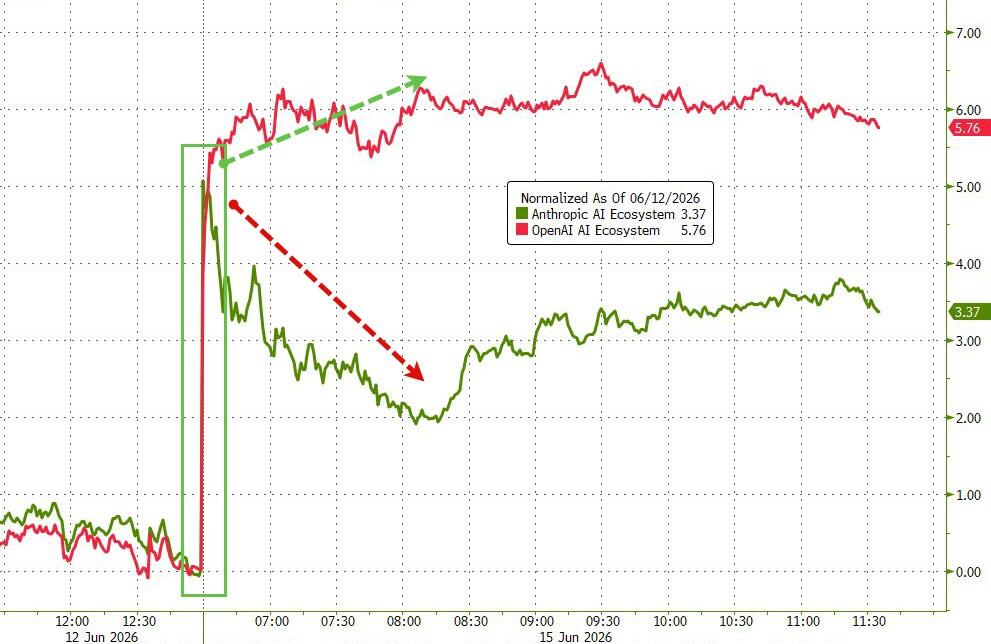

However, clear divergence has emerged within the AI ecosystem.

The U.S. Department of Commerce placed Anthropic’s two leading AI models, Fable 5 and Mythos 5, under export controls, restricting access by foreign nationals both overseas and within the U.S., citing jailbreaking security risks. Anthropic’s tokenized stock plunged sharply on Monday.

The broader Anthropic-related AI ecosystem also underperformed relative to the OpenAI-linked ecosystem, despite gains in both.

Meanwhile, $SpaceX (SPCX.US)$ The stock posted a single-day gain of 20%, extending its strong momentum following last Friday’s IPO.

In an intraday report, Rich Privorotsky, Goldman Sachs’ chief 1-Delta trader, noted that the focal point of competition in AI is shifting from a handful of leading labs toward model orchestration and open-source ecosystems.

This trend carries dual implications: lower costs and broader accessibility could boost demand for computing power and tokens, yet it also accelerates token price declines and raises questions about the sustainability of model monetization strategies.

In bond markets, U.S. Treasury yields diverged on the day, with the two-year yield edging down by 2 basis points and the ten-year yield holding steady at 4.47%. Investors awaited more significant signals later this week—the first monetary policy meeting chaired by new Federal Reserve Chair Warsh.

Economists expect the Federal Reserve to keep its benchmark interest rate unchanged in the 3.5%–3.75% range, adopting a wait-and-see stance on the economic impact of energy shocks emanating from the Middle East.

The central question for markets is how Chair Warsh will balance inflation control against economic growth and navigate the trade-off between institutional independence and policy flexibility. Tomo Kinoshita, global market strategist at Invesco Asset Management, stated:

Historical observations suggest that for every 10% decline in oil prices, the yield on the U.S. 10-year Treasury note falls by approximately 13 basis points.

If this relationship holds true currently, it implies potential downside room for long-duration bonds.

The U.S. Dollar Index fell to its lowest level since June 5, with dollar weakness mutually reinforcing a decline in market risk-off sentiment.

Notably, the Bloomberg Dollar Spot Index found support near its 200-day moving average and rebounded slightly, closing with limited net change, though it remains approximately 1.4% higher than levels seen since the U.S.-Israel strike on Iran.

Gold surged sharply over the past two trading sessions, rebounding strongly from a low near $4,000 to above $4,300, posting a daily gain of 2.4%, yet still remaining below its 200-day moving average of $4,450.

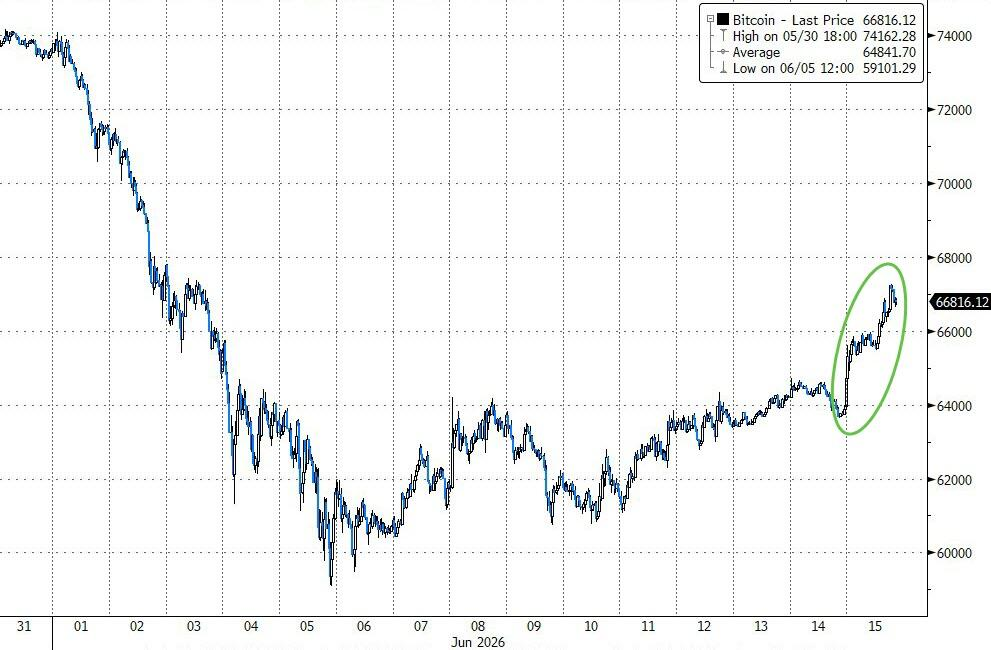

$Bitcoin (BTC.CC)$ The asset posted a daily gain of nearly 5%, marking its strongest single-day performance since early March, breaking above $66,000—the first time surpassing this level in two weeks.

On Monday, U.S. semiconductor and small-cap stocks closed at record highs. The SPCX index surged 20%, driven by substantial IPO fundraising. Energy and defensive sectors lagged, while small caps opened higher but closed lower.

U.S. benchmark indices:

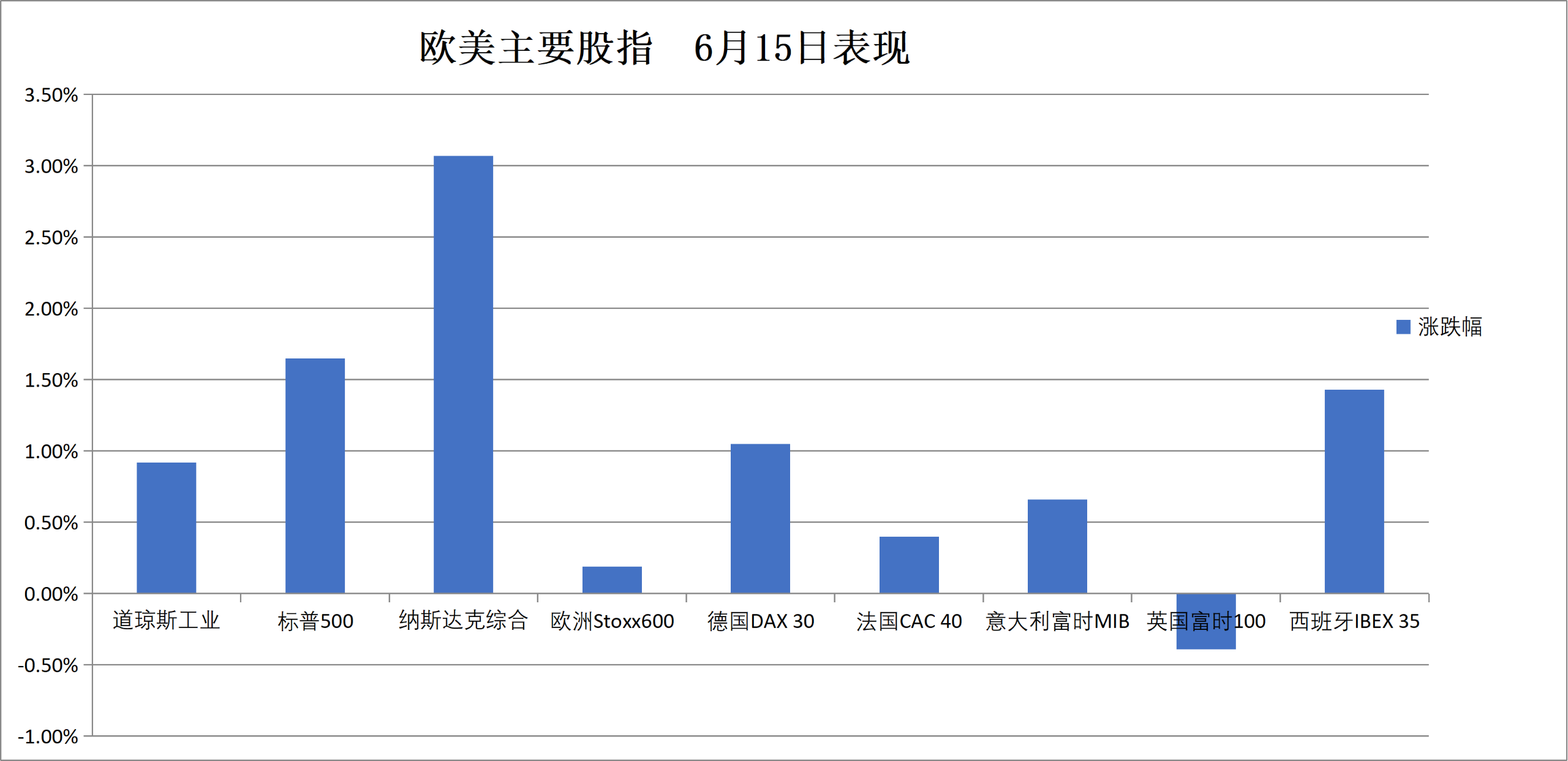

The S&P 500 Index rose 122.83 points, or 1.65%, closing at 5,167.10, marking a cumulative rebound of 3.95% over the last three trading days.

The Dow Jones Industrial Average gained 468.77 points, or 0.92%, closing at 51,671.03, surpassing its previous record high close of 51,561.93 set on June 4.

The Nasdaq Composite rose 795.097 points, or 3.07%, closing at 26,683.941. The Nasdaq 100 Index climbed 907.971 points, or 3.06%, ending at 30,543.918.

Russell 2000 IndexIt rose 0.72% to close at 2,965.087 points, setting another record high closing level.

The CBOE Volatility Index (VIX) declined 8.37% to close at 16.20.

U.S. stock sector ETFs:

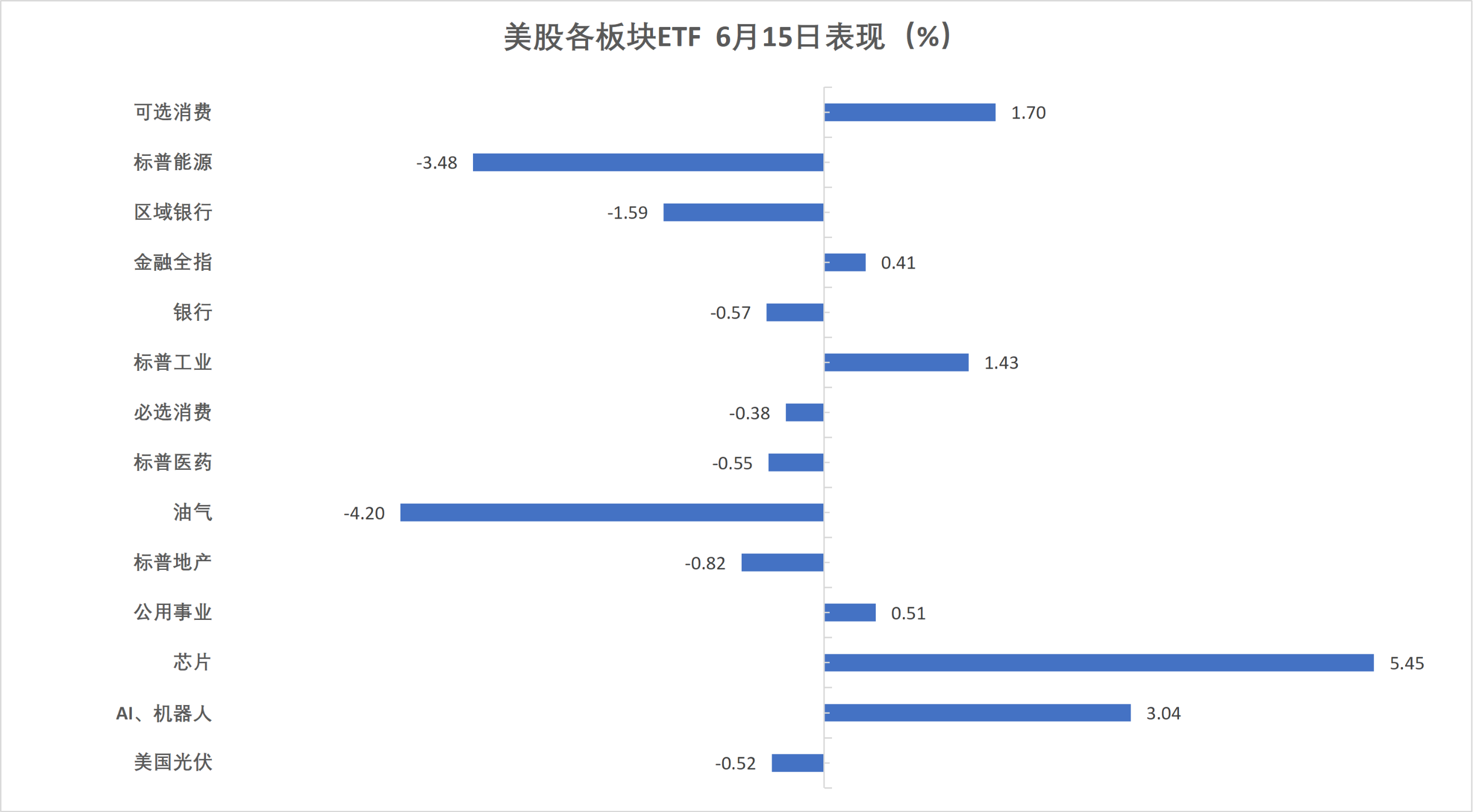

The semiconductor ETF gained 4.38%, while the global technology equity index ETF, technology sector ETF, and global airline industry ETF each rose at least 3.15%. In contrast, the banking sector ETF and regional banking ETF fell by up to 1.61%, and the energy sector ETF dropped 3.48%.

Mag 7:

The Mag 7 index rose 2.74% to close at 216.22 points.

$Tesla (TSLA.US)$ rose 1.16%, $Apple (AAPL.US)$ rose 1.82%, Microsoft gained 2.31%, Google A climbed 2.69%, Amazon advanced 3.16%, $NVIDIA (NVDA.US)$ rose 3.54%, and Meta surged 4.77%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ rose 5.45% to close at 14,099.623 points, surpassing its previous record high close of 13,916.960 points set on June 3.

Taiwan Semiconductor ADR rose 3.99%, $Advanced Micro Devices (AMD.US)$ up 6.98%.

The storage quartet hit new highs again, $Micron Technology (MU.US)$ surging more than 10%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed up 0.39% at 6,351.43 points.

Among actively traded Chinese stocks listed in the U.S., Kingsoft Cloud gained 5.8%, 21Vianet rose 5.1%, GDS Holdings advanced 2.6%, PDD Holdings increased by 2.4%, Ctrip climbed 1.9%, ASE Group rose 1.2%, New Oriental edged up 0.7%, Baidu gained 0.6%, and NetEase rose 0.1%.

Other individual stocks:

$Circle (CRCL.US)$ up 7.13%.

European equities hit a record closing high, with Deutsche Bank rising 4.3% and Ferrari leading gains among eurozone blue chips. Germany’s stock market closed up 1%, while Italian and Spanish indices continued to reach record closing highs.

Pan-European Index:

The STOXX Europe 600 Index closed up 0.19% at 634.44 points, surpassing its previous record closing high of 633.85 points set on February 27, and has risen 2.63% over the last three trading sessions.

The EURO STOXX 50 Index closed up 0.68% at 6,229.43 points, marking its second consecutive record closing high and gaining 3.65% over the past three days.

Major Stock Indexes Around the World:

Germany's DAX 30 Index closed up 1.05% at 24,894.01 points.

France's CAC 40 Index closed up 0.40% at 8,384.01 points.

The FTSE 100 closed down 0.39% at 10,430.62 points.

Sector and individual stock performance:

Among Eurozone blue-chip stocks, Deutsche Bank rose 4.31%, Ferrari gained 4.07%, with Morgan Stanley noting that concerns about the company are overblown; Santander advanced 3.86% to rank third, while TotalEnergies fell 4.43%, Rheinmetall declined 4.60%, and Eni dropped 4.69%.

Among all constituents of the STOXX Europe 600 Index, Hochschild Mining rose 10.72%, Technoprobe gained 7.34%, Kion Group increased by 7.19%, and Boliden advanced 7.08% to rank fourth.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen