Barclays and Citi turned bullish on the same day! Gold has undergone a 25% deep correction, a U.S.-Iran memorandum of understanding is imminent, oil price expectations have fully reversed, and inflationary headwinds are fading. Citi raised its three-month target to $4,500 and sees prices reaching $5,000 in six to twelve months; Barclays asserts this round represents a 'price reset,' not the end of the bull market.

After a deep correction lasting 2.5 months and amounting to a 20%–25% decline, gold now stands at a critical inflection point.

On June 15, Barclays and Citi both issued statements on the same day: the former explicitly declared it was 'time to increase gold exposure,' while the latter raised its three-month gold price target from USD 4,000 per ounce to USD 4,500 per ounce. Both institutions share the view that this correction resembles a price reset rather than the end of the bull market.

The key catalyst driving this renewed optimism is the announcement by the U.S. and Iran that they will formally sign a Memorandum of Understanding (MoU) this Friday. According to Citi Research, this development is expected to restore trade flows through the Strait of Hormuz to near-normal levels by mid-to-late July, allowing oil markets to refocus on weak supply-demand fundamentals. Citi has consequently revised down its Brent crude oil price forecasts for Q3 2026 through 2027 to USD 75, USD 70, and USD 65 per barrel, respectively (previously USD 110, USD 90, and USD 80 per barrel).

Citi believes that with geopolitical tensions easing, inflationary pressures are likely to subside, potentially removing a key macro headwind that had been weighing on gold prices. Citi maintains its bullish 6- to 12-month gold price forecast of USD 5,000 per ounce but cautions that significant volatility risks remain.

Barclays conducted a comprehensive review of this correction across three dimensions: foreign exchange, equity strategy, and derivatives. The bank attributes the sharp selloff to a combination of factors: a roughly 2.5% strengthening of the U.S. dollar, a more than 10% rise in the S&P 500 index, and the unwinding of crowded long positions. However, medium-term support for gold remains intact: persistently high inflation, ongoing policy uncertainty, and strategic demand from central banks for reserve diversification. Once geopolitical pressures stabilize, these factors are expected to reassert their influence over gold’s trajectory. Barclays estimates that for every 1 percentage point increase in U.S. CPI, gold prices rise by approximately 5%, suggesting that this inflation transmission mechanism will serve as the core driver of the current rebound.

U.S.-Iran Memorandum of Understanding: Key Catalyst Emerges, Oil Price Outlook Reverses

According to Citi Research, the breakthrough in U.S.-Iran negotiations is viewed as one of the most significant events in commodity markets this year. Citi notes that while markets have already priced in the announcement of the MoU signing, they have not yet fully reflected the scenario of sustained recovery in Strait of Hormuz traffic over the medium term—if they had, crude oil prices would be approximately USD 10–15 per barrel lower than current levels, implying further downside potential.

Citi’s base case scenario (60% probability) assumes continued progress in negotiations following the formal MoU signing, leading to an estimated paper surplus of around 4 million barrels per day in the oil market by 2027, which would likely push crude prices below USD 70 per barrel. Citi also outlines two tail-risk scenarios: a bullish scenario (20% probability) involving a temporary de-escalation followed by renewed conflict, and a bearish scenario (20% probability) characterized by rapid production ramp-ups in the UAE, Saudi Arabia, and Iran, coupled with a Russia-Ukraine ceasefire agreement.

The spillover effects of falling oil prices directly benefit precious metals. Citi argues that energy-driven inflation stemming from Middle East conflicts was a key factor pressuring gold prices—high oil prices fueled inflation expectations, compelling central banks to maintain hawkish stances and limiting room for real interest rates to fall. As oil-related inflationary pressure eases, this transmission channel is expected to gradually reverse, opening an upward path for gold prices.

Barclays: This Correction Is a 'Reset,' Not the End

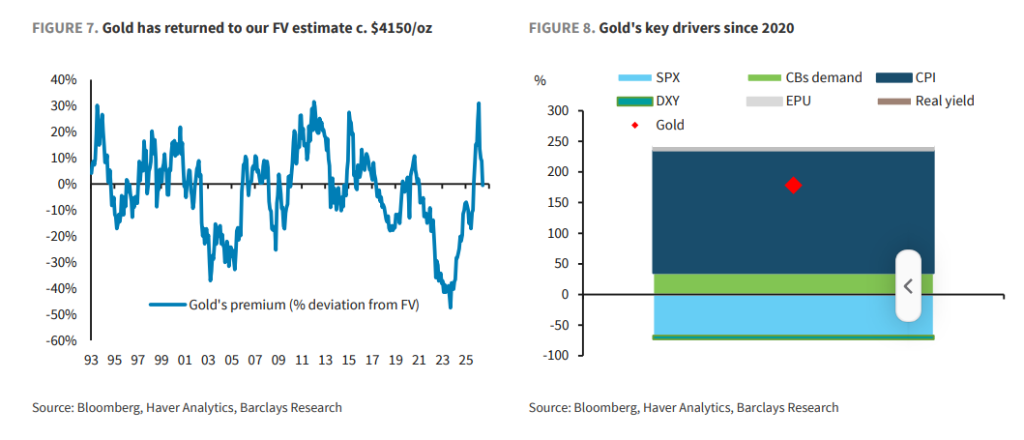

According to Barclays Research, gold has posted cumulative gains of over 100% since January 2024. After peaking at around USD 5,500 per ounce in January this year, it subsequently experienced a correction of approximately 25%, bringing prices back to levels last seen in November 2025. Barclays noted that, given the priorTechnical Analysisextreme valuation stretch and clear overextension relative to macro fundamentals—particularly real interest rates—the current pullback is not surprising.

From a valuation perspective, Barclays analysts stated that gold prices have now reverted to the fair-value range estimated by their model—at approximately USD 4,150 per ounce. This model identifies U.S. CPI, the S&P 500, the U.S. dollar index, and central bank gold purchases as the four key drivers of gold prices. So far this year, the simultaneous strength in both the dollar and equities has exerted downward pressure on gold. Additionally, some emerging market central banks have sold gold reserves to stabilize their domestic currencies amid Middle East conflicts, creating additional selling pressure and further weighing on prices.

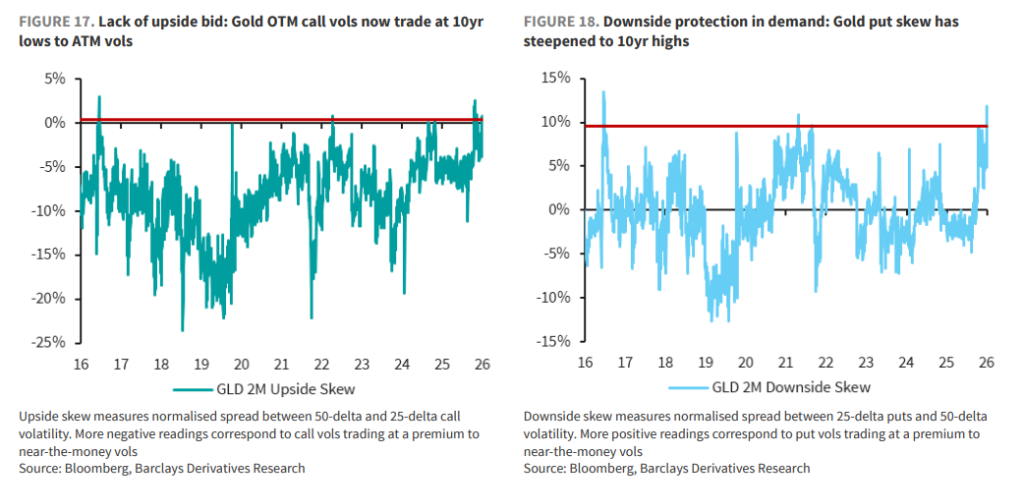

At the options market level, Barclays’ derivatives strategy team observed that positioning andoptions pricingmetrics have normalized significantly from their extreme levels at the start of the year.

Most notably, call optionimplied volatility,premiums have reversed from deep levels of overvaluation at the beginning of the year to their lowest levels in nearly a decade, while put skew has risen to a near-decade high due to increased hedging demand. This structural shift implies that the risk-reward profile for capturing asymmetric upside via options has improved substantially, and the broader clearing of market sentiment has laid a healthier technical foundation for a potential new upswing.

The Long Tail of Inflation: The Strongest Structural Support for Gold Prices

Barclays views U.S. inflation as the dominant variable shaping gold’s medium- to long-term trajectory.

Their model estimates that a one-percentage-point increase in U.S. CPI translates into roughly a 5% rise in gold prices. This implies that the cumulative upward pressure on CPI stemming from Middle East energy shocks will remain embedded in gold’s bullish narrative as persistent inflation—even after oil prices eventually retreat.

From a broader structural perspective, Barclays believes multiple long-term tailwinds for gold remain firmly intact.

First, the ongoing trend toward de-dollarization continues to erode global demand for dollar-denominated reserves.

Second, developed-market central banks are increasingly inclined to tolerate inflation moderately above target over the long term, which will persistently erode fiat currency purchasing power.

Third, the expectation of currency depreciation driven by fiscal deficit expansion and tariff policies has provided gold with additional premium support beyond its historical correlations.

Central bank gold purchase data also indicate that structural demand remains robust.

According to the latest data from the World Gold Council (WGC), central banks’ gold purchases in Q1 2026 rose by 17% quarter-over-quarter in ounces and surged by 38% in U.S. dollar terms due to elevated gold prices. The primary buyers in the first quarter were the central banks of Poland and Uzbekistan. Tether, the world’s largest stablecoin issuer, also continued to increase its holdings, purchasing 12.6 tonnes in Q1, bringing its total reserves to 154 tonnes—ranking it fourth globally, ahead of most major central banks. Turkey and Russia, however, recorded significant net sales due to domestic currency stabilization needs. Barclays believes that as geopolitical tensions ease, emerging market central banks that previously sold gold reserves are likely to resume accumulation.