On June 12, 2026, SpaceX officially listed on the Nasdaq. Its shares rose 19% on the first day of trading, closing with a market capitalization of $2.1 trillion, making it the sixth-largest publicly traded company in the United States—within Wall Street’s expected range of $1.7–2.5 trillion—and marking an uneventful yet solid debut.

This initial public offering (IPO), the largest in human history, raised a total of $75 billion—nearly half of the entire U.S. IPO fundraising volume for 2025. Given that the company reported revenue of less than $19 billion and a net loss of approximately $4.9 billion in 2025, its price-to-sales (PS) ratio exceeded 100x.

Effectively, the market priced this trillion-dollar giant using venture capital logic typically reserved for early-stage startups. Controversy was thus inevitable: some hailed it as a milestone for human civilization, while others called it the biggest bubble ever inflated by Elon Musk.

But beyond short-term stock performance or Musk’s ranking on wealth lists, we want to focus on an essential point overlooked by most: SpaceX’s true value extends far beyond that of a space company—it is actively validating the fourth-generation corporate model in human business history: the systems-driven enterprise.

But beyond short-term stock performance or Musk’s ranking on wealth lists, we want to focus on an essential point overlooked by most: SpaceX’s true value extends far beyond that of a space company—it is actively validating the fourth-generation corporate model in human business history: the systems-driven enterprise.

The IPO story is straightforward: from a rocket company to a space infrastructure platform.

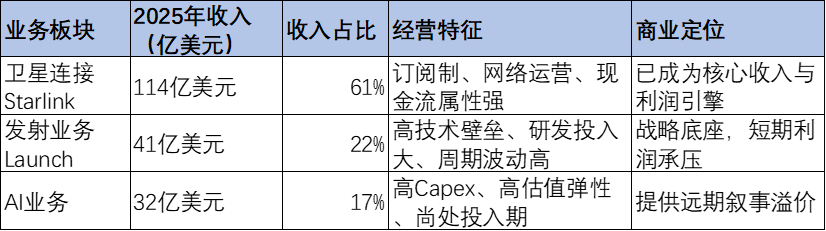

SpaceX operates across three core business segments: Launch, Satellite Connectivity (Starlink), and AI. The launch business provides foundational access capabilities and continues to iterate; Starlink generates recurring operating cash flow and shows steady growth; AI carries the forward-looking narrative that justifies high valuation premiums.

Among these, Starlink is the only profitable segment, while Launch and xAI remain in heavy investment phases.

1. Rockets dominate global launches—the Starship is the real game-changer.

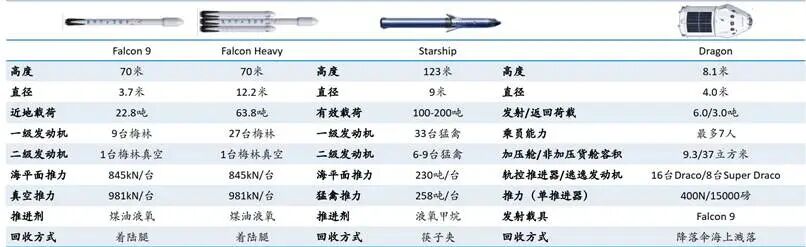

Rockets are the foundation of SpaceX, encompassing Falcon, Dragon, and Starship. Among these, Falcon 9 is currently SpaceX’s undisputed workhorse. As the world’s first orbital-class reusable launch vehicle, it leverages full recovery of its first stage and partial recovery of payload fairings to reduce marginal launch costs to approximately USD 15 million per mission, establishing a significant lead over competitors.

In 2025, SpaceX completed 170 launches, accounting for 87% of total U.S. launches and 83% of global orbital payload mass. Its average launch capacity per mission was roughly 4.4 times that of other providers.

Yet even with a near-monopoly on the global launch market, its total launch-related revenue for the year amounted to just over USD 4 billion—highlighting the inherently limited ceiling of the launch services market. Even if future demand were to increase tenfold, it would still fall short of funding ambitions such as Mars colonization.

Starship represents the true breakthrough. Since its inaugural launch in 2023, SpaceX has already invested USD 15 billion cumulatively into the Starship program.

Its value lies not merely in greater payload capacity, but in transforming space launch from a 'customized service' into 'scalable transportation infrastructure.' While Falcon 9’s cost per kilogram is approximately USD 830–880, Starship aims to reduce this to USD 100–200 per kilogram—a reduction of over 80%. In the long term, it targets a launch cadence of once per hour, amounting to tens of thousands of annual launches, thereby elevating annual orbital delivery capacity to the megaton scale.

All long-term initiatives—including next-generation Starlink satellites, in-space computing, lunar landings, and Mars missions—hinge entirely on the commercialization timeline of Starship.

2. Starlink is a high-growth cash-cow business

Launch services constitute a discrete, project-based business with a relatively low ceiling. To realize its long-term vision, Musk opted to internally reuse SpaceX’s low-cost orbital access capability, with Starlink emerging as the first successfully scaled application.

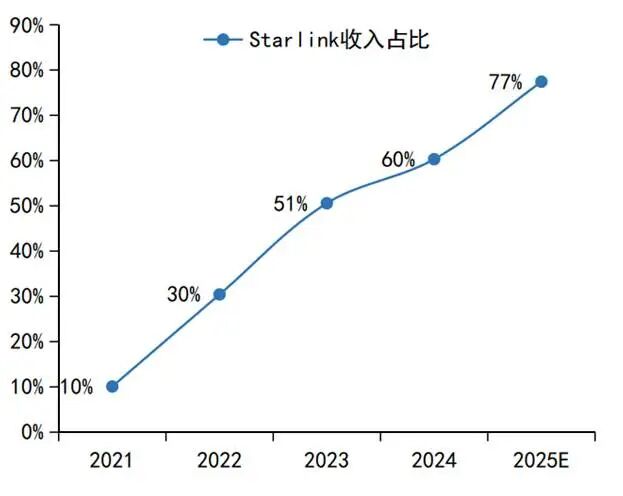

Over the past few years, Starlink’s strategic evolution has been remarkably clear, with its share of SpaceX’s total revenue rising steadily: from just 10% in 2021 to over 50% in 2023, and reaching 77% by 2025. More importantly, it has already turned profitable: generating USD 11.4 billion in revenue in 2025, with net profit of USD 4.4 billion, gross margin nearing 60%, operating margin around 35%, and net margin exceeding 10%.

Starlink’s major commercial significance lies in transforming SpaceX from a project-based company—essentially taking orders to launch rockets—into a communications operator with recurring subscription revenue and compounding growth potential.

It currently operates nearly 10,000 low Earth orbit satellites, delivering download speeds exceeding 200 Mbps—surpassing the average performance of terrestrial fixed and mobile broadband. As of the end of Q1 2026, its subscriber base surpassed 10.3 million, doubling since the beginning of the year.

Its future growth trajectory is also relatively certain. In the second half of 2026, SpaceX will deploy V3 satellites via Starship, offering 10 times the downlink capacity and 20 times the uplink capacity of V2 satellites, at a cost 90% lower than V1. We understand that the company’s long-term plan calls for expanding its satellite constellation to 15,000 by 2031, ultimately building a global satellite internet constellation of 42,000 satellites.

As satellite performance continues to improve and encryption capabilities strengthen, Starlink is poised to fully transition into a mainstream telecom operator. Estimates suggest Starlink’s total addressable market exceeds USD 300 billion: residential broadband could serve 200 million households, representing a USD 200 billion opportunity; direct-to-cellphone satellite connectivity accounts for approximately USD 60 billion; and aviation, maritime, and enterprise segments contribute several hundred billion dollars in additional upside.

3. Long-Term Integration with AI: The Ultimate Valuation Narrative for IPO

AI represents the most debated yet highest-potential component of SpaceX’s valuation. According to its IPO prospectus, the estimated target market size is USD 28.5 trillion—of which the vast majority stems from AI.

In fact, in February 2026, SpaceX completed a stock-swap merger with xAI valued at USD 250 billion: Colossus provides training and inference computing power, Grok focuses on large language models, and the X platform supplies internal data. Many observers believe this move was designed to bolster SpaceX’s IPO narrative by positioning it as an integrated aerospace–communications–AI platform.

However, 2025 data paints a stark picture: AI-related revenue amounted to only USD 3.2 billion, while losses exceeded USD 6 billion, against capital expenditures of USD 12.7 billion. Although short-term growth over the next three years will be driven by rapid scaling of compute leasing—with long-term agreements already signed with Anthropic and Google expected to generate stable annual revenue of USD 25 billion—the underlying business model remains unattractive from a valuation perspective.

The real story, however, is about moving AI from the ground into space.

Musk proposed that Starlink satellites are not merely communication nodes but also computing nodes: leveraging the high-speed laser links of V3 satellites, a meshed, distributed computing infrastructure can be established in orbit. Each AI satellite is equipped with computing chips powered by solar energy and cooled via radiative heat dissipation in space, thereby completely eliminating reliance on terrestrial power, land, and cooling constraints.

SpaceX has already planned a constellation of AI-capable satellites numbering in the millions, with initial deployment expected as early as 2028. Once fully deployed, the total annual power consumption of AI computing capacity launched into space could reach 100 GW—equivalent to the total global ground-based data center construction scale projected for 2027.

In this vision, space-based solar energy is virtually inexhaustible, and radiative cooling costs are far lower than those on Earth, resulting in overall costs an order of magnitude lower than terrestrial data centers—making it the only scalable path toward exascale (TW-level) AI computing. According to Starcloud, a startup focused on space-based data centers, the cost of space-based energy (including launch expenses) will be ten times cheaper than ground-based alternatives.

Controversy stems precisely from this: the industry competitiveness of the Grok model remains unproven, and real challenges include core talent attrition and soaring capital expenditures. The market estimates SpaceX’s total capital expenditure in 2026 will reach USD 60 billion, of which USD 50 billion will be allocated to AI.

At the same time, there are also counterarguments in the market questioning the current economic viability of space-based computing. After all, many of Musk’s bold claims have yet to materialize. Nevertheless, it is undeniable that it is precisely the AI narrative that has enabled SpaceX to break entirely out of the valuation framework typical of traditional aerospace companies.

Reassessing SpaceX Through the Lens of Business Models: The Fourth-Generation Business Model

Setting aside technical details and valuation debates, from the perspective of business history, what makes SpaceX truly unique is that it is pioneering a new form of corporate organization—the fourth-generation business model: the systems-oriented company.

The evolution of commercial civilization fundamentally reflects the advancement of how enterprises integrate resources and solve problems. Within our framework, three dominant generations of business models have emerged to date.

1. The first generation is vertical integration.

Vertical integration refers to a company operating across multiple core stages of its value chain—ranging from upstream raw material sourcing and manufacturing to product distribution and end-customer sales—thereby completing an entire value chain internally and establishing internal supply-demand relationships.

Its primary advantage lies in building a cost moat by locking in upstream raw materials and controlling downstream channels or end markets, thereby reducing reliance on external partners and mitigating risks from supply chain volatility. This model is especially effective during the early stages of an industry’s development when the supply chain is immature.

However, its drawbacks include a nonlinear increase in management complexity, reduced organizational agility, and potentially diminished specialization and innovation efficiency due to involvement across multiple business segments, making it difficult to respond swiftly to market shifts. Additionally, low capacity utilization can lead to idle assets, resource waste, and amplified gross margin volatility.

Notable examples include Ford Motor’s historical control over the entire chain—from rubber plantations and steel mills to automobile assembly plants; BYD’s vertical integration spanning batteries, motors, electronics, and complete vehicles; and Muyuan’s closed-loop operations covering feed production, breeding, farming, and slaughter.

2. The second generation is the conglomerate model.

The conglomerate business model entails a diversified portfolio of businesses across different sectors, achieving stable compounding returns within a unified governance structure through strategic capital allocation, organizational design, and platform capabilities.

Its strength lies in risk diversification—'when one business falters, another may thrive'—as cyclical fluctuations across segments can offset each other, while shared resources such as brand equity, distribution channels, and management expertise enhance efficiency. However, a clear drawback is the tendency toward 'conglomerate disease,' characterized by resource fragmentation and insufficient focus on core businesses. Consequently, many conglomerates are now pursuing spin-offs and separate listings, as exemplified by GE and ThyssenKrupp.

Representative paradigms include Siemens’ integrated platform combining hardware, software, industrial software, and services; GE’s high-barrier equipment ecosystem built around installed base and long-term service contracts; and Japan’s sogo shosha model of global resource integration through investment, trading, and industry-finance synergy. Other notable companies adopting this approach include Xiaomi, Honeywell, Tencent, Midea, PepsiCo, and LVMH.

3. The third-generation business model is based on specialized division of labor across the industrial chain.

Over the past three decades, under the wave of globalization, the dominant business model has been for enterprises to specialize and collaborate across different segments of the value chain—focusing exclusively on what they do best. This approach offered clear advantages: significantly enhanced efficiency and quality at lower costs. So compelling were these benefits that specialization came to be regarded as the ultimate form of business organization.

Apple, one of the most successful examples, exemplifies extreme specialization in its supply chain: design is handled in the U.S., chips are manufactured by Taiwan Semiconductor, assembly is carried out by Foxconn, and components are sourced globally. Other notable cases include the semiconductor industry’s division of labor, Uniqlo’s focus on branding and retail, and Zhongji Xuchuang’s specialization in optical module assembly.

However, the drawbacks have been selectively overlooked. Finer specialization increases transaction costs, and during disruptions, information silos and coordination inefficiencies across organizations are significantly amplified. In the current era of deglobalization, international supply chains are more prone to supply disruptions, and external dependencies on critical technologies or raw materials can create 'choke points.'

This is especially true when industries enter uncharted technological frontiers—such as general-purpose AI, controlled nuclear fusion, or space colonization—where no mature solutions or established suppliers exist along the value chain, causing the specialization model to fail collectively.

Recent bottlenecks in AI development all stem from this failure of specialization: optical modules face severe shortages in photonic chip capacity; meanwhile, the industry shows limited willingness to invest in the new CPO (co-packaged optics) direction, forcing NVIDIA to step in directly. Similarly, PCB production suffers from insufficient HDI capacity, while upstream materials like electronic-grade glass fabric and copper foil are becoming scarce. Even if semiconductors, optical modules, and PCBs are available, electricity itself has become hard to secure.

4. The Fourth-Generation Business Model Emerges

To address these challenges, we observe the emergence of a fourth-generation business model—systematization—whose solution is to deliberately integrate vertically, adopt an end-to-end mindset, and systematically resolve every bottleneck across the entire value chain by working backward from the ultimate objective.

Early manifestations of this model can already be seen in Apple, CATL, Taiwan Semiconductor, Tesla, Amazon, and Google—with Google being the most representative, possessing a closed-loop system spanning chips, communication technologies, cloud infrastructure, data, models, and applications. Yet, the most complete embodiment is arguably SpaceX.

Reconstructing SpaceX Through a Systems Lens

From its inception, SpaceX’s mission has been to make humanity a 'multiplanetary species.' Since no existing solutions addressed the myriad challenges involved, Elon Musk had no choice but to tackle each problem individually based on first principles.

What was the state of the entire aerospace industrial chain when Musk founded SpaceX in 2002?

• Rocket engines: No mature commercial suppliers existed.

• Reusability technology: The entire industry deemed it impossible.

• Low-cost satellites: The industrial chain simply did not exist.

• Satellite internet: Spectrum allocation, technology, and user terminals were all undeveloped.

• Space-based computing: The concept did not even exist.

The aerospace industry at the time was still dominated by the military's 'cost-plus' contracting model: layers of subcontracting with pricing set at cost plus a 15% profit margin. Efficiency was ignored, and there was no mature commercial supply chain. Musk’s choice was clear: if the existing industrial chain could not deliver what he needed, he would build an entirely new one himself.

1. Rockets: Few suppliers for SpaceX could be found.

Traditional rocket companies outsourced their engines, whereas SpaceX developed all its engines—from Merlin to Raptor—in-house. In fact, SpaceX achieves over 80% in-house development and manufacturing for Starship, covering everything from engines and airframe structures to laser communication modules and flight software.

Although vertical integration required massive upfront investment, it later enabled exceptionally rapid iteration cycles and superior cost control. The Merlin engine achieved the world’s highest thrust-to-weight ratio at a fraction of the cost of traditional engines. The Raptor engine became humanity’s first practical full-flow staged combustion cycle engine.

Not waiting for suppliers or complaining about the industrial chain, but instead taking matters into its own hands to address every weakness—this is the defining trait of a systems-oriented company.

2. Starlink: Rejecting Industry Norms

The prevailing industry consensus in traditional satellite communications used to be: a single satellite costs hundreds of millions of dollars, has a lifespan of over a decade, serves several hundred thousand high-value customers, and delivers an ARPU (Average Revenue Per User) of several thousand dollars. Satellite internet was always seen as a niche business, incapable of competing with terrestrial operators.

SpaceX completely overturned this logic: it miniaturized, standardized, and mass-produced satellites, driving the per-satellite cost below $500,000; it launched them using its own rockets, reducing launch costs by an order of magnitude compared to the industry average; it developed its own user terminals, slashing the price of customer equipment from thousands of dollars to just a few hundred; and it pioneered inter-satellite laser links, enabling global network coverage without relying on ground stations.

The result? Constellations that would take traditional satellite operators decades to deploy were completed by SpaceX in just a few years. While traditional satellite services required an ARPU of several thousand dollars to be viable, SpaceX achieved profitability at an ARPU of just a few hundred dollars—and plans to drive it even lower, eventually entering the pricing range of conventional terrestrial operator plans, thereby becoming a formidable competitor.

This exemplifies the second hallmark of a systems-oriented company: rejecting the industry’s entrenched cost structures and business models, and instead reconstructing the entire value chain from first principles.

3. Space-Based Computing Power: Redefining Problems Beyond Industry Boundaries

While everyone else was racing to secure GPUs, compete for power supply, and build data centers, SpaceX posed a fundamental question: Why must AI computing power reside on Earth?

Space offers 24/7 uninterrupted solar energy, natural radiative cooling, unlimited physical space, and freedom from land-use approvals, environmental reviews, and power constraints. More importantly, as AI computing demand scales from gigawatts (GW) to terawatts (TW), Earth’s power and land resources simply cannot keep up—a 100 GW computing cluster would require the electricity output of an entire medium-sized country.

SpaceX’s answer: move computing power into space. This is not mere fantasy, but a choice grounded in the laws of physics. It embodies the third defining characteristic of a systems-oriented company: refusing to be confined by current industry boundaries, and instead redefining the solution space by reasoning backward from the ultimate objective.

4. Return to the core: Space + X, where X represents infinite possibilities

Once you understand the logic of a systematized company, SpaceX's business model becomes immediately clear.

It has vertically integrated the entire chain—from rockets and satellites to launch services, ground terminals, and applications—using Starlink’s steady cash flow to reinvest in rocket development, leveraging lower orbital launch costs to unlock new business scenarios, and channeling the resulting profits into next-generation technologies, thereby creating a virtuous cycle.

Over the past two decades, the cost of accessing space has dropped by two orders of magnitude: from $16,000 per kilogram on the Delta IV Heavy, to $3,000 per kilogram on Falcon 9, to $1,500 per kilogram on Falcon Heavy, with Starship targeting $100 per kilogram.

Therefore, at its core, SpaceX employs a systematic approach to reduce the cost of space access to a sufficiently low level, thereby unlocking one previously impossible market after another:

● When launch costs fall to $1,000 per kilogram, Starlink becomes feasible.

● When launch costs fall to $100 per kilogram, space-based computing becomes feasible.

● When launch costs fall to $10 per kilogram, space manufacturing, space tourism, lunar bases, and Mars colonization all become feasible.

This is the true meaning behind the 'X' in SpaceX: it is not a rocket company, not a satellite company, and not even an AI company. Its core business is continuously lowering the barrier to human access to space. Once that barrier is low enough, X can become anything. Rockets are the leading '1'; Starlink is the first '0'; AI is the second '0'; and countless more '0's may follow.

The debate over whether a $2.1 trillion valuation is too expensive or indicative of a bubble will not be resolved in the short term. Yet, viewed through the lens of business history, the significance of this development has already transcended share prices themselves.

Over the past century, we have witnessed the rise of vertical integration, the rise and fall of conglomerate empires, and the miracle of globalized specialization. Now, we are witnessing firsthand the emergence of humanity’s fourth-generation corporate model—entering reality directly from space.