A Bank of America survey shows that 56% of fund managers believe AI is still in a 'boom phase,' and 80% consider long positions in semiconductors to be the most crowded trade in history. As concerns over an AI bubble intensify, institutions have begun reducing exposure to technology stocks and global equities at elevated levels, increasing cash allocations, and shifting some capital toward defensive sectors such as financials and telecommunications—though most investors remain optimistic about AI’s long-term outlook.

Global fund managers remain highly optimistic about the artificial intelligence (AI) investment theme, with a majority of respondents viewing the sector as still in a 'boom' phase driven by fear of missing out (FOMO). However, as valuations rise and trade crowding reaches record highs, signs of profit-taking at elevated levels have emerged, prompting investors to tactically reduce their risk exposure to technology stocks and global equities.

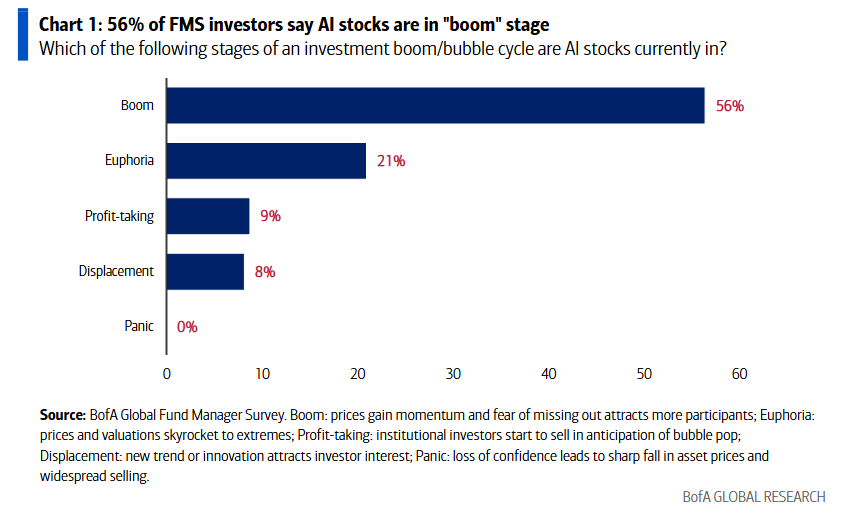

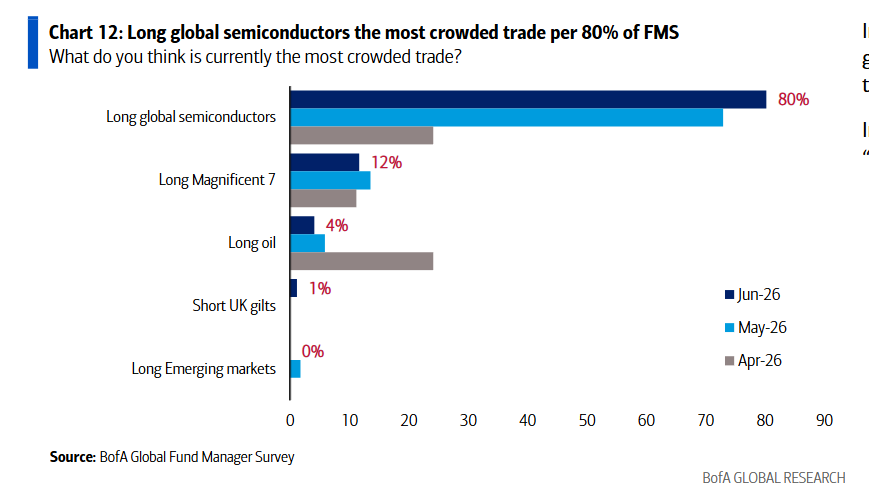

According to Bank of America’s Flow Show trading desk, the latest monthly Fund Manager Survey by star strategist Michael Hartnett reveals that 56% of surveyed managers characterize the current phase of AI stocks as a 'boom.' Additionally, a striking 80% of respondents identified 'being long global semiconductors' as the most crowded trade—a record high in the survey’s history.

In light of potential market overheating risks, institutional investors are adopting a 'take-profit' strategy to lock in gains. Survey data shows that fund managers have sharply reduced their overweight position in global equities from 50% last month to 38%, while their overweight in technology stocks has declined from 33% to 26%, reflecting increased caution ahead of summer and a notable shift toward defensive positioning.

In light of potential market overheating risks, institutional investors are adopting a 'take-profit' strategy to lock in gains. Survey data shows that fund managers have sharply reduced their overweight position in global equities from 50% last month to 38%, while their overweight in technology stocks has declined from 33% to 26%, reflecting increased caution ahead of summer and a notable shift toward defensive positioning.

Moreover, rising macro tail risks are prompting portfolio reallocations. Investors have slightly increased cash holdings and, in regions such as Asia-Pacific, capital is rotating away from crowded AI-related beneficiaries toward defensive sectors like financials and telecommunications—highlighting a delicate balance between chasing growth and managing downside risk.

Enthusiasm for AI coexists with concerns over 'crowded trades'

Among global fund managers overseeing $465 billion in assets, the AI theme remains the dominant force shaping markets.

The survey indicates that more than half (56%) of investors believe AI stocks are currently in a 'boom' phase—a stage characterized by accelerating momentum and FOMO-driven participation.

By contrast, only 21% of respondents consider the sector to be in an extreme-valuation 'euphoria' phase, while 9% view it as being in a 'profit-taking' stage where large investors begin to sell.

Despite overall positive sentiment, concerns about concentration in the tech sector are intensifying. Four out of five (80%) respondents regard buying and holding global semiconductor stocks as the most crowded trade.

This figure not only has topped the ranking for two consecutive months but also marks the highest level ever recorded in Bank of America’s Fund Manager Survey. Additionally, 12% of respondents identified being long the 'Mag 7' as a crowded trade.

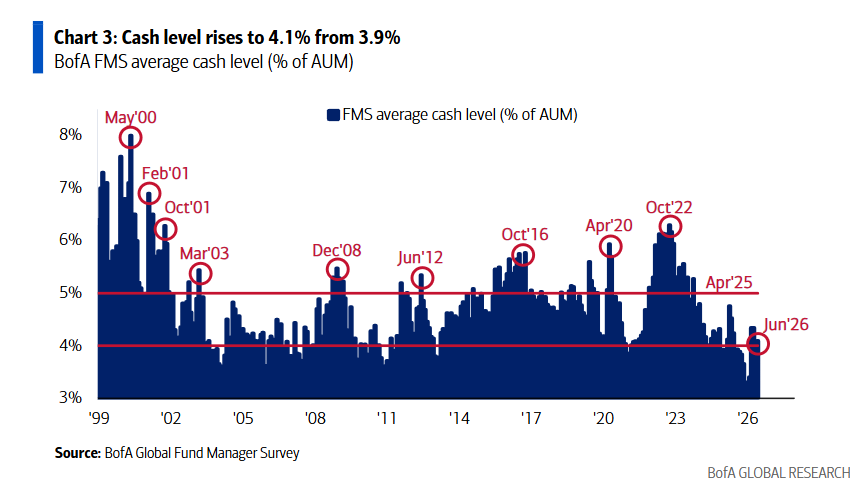

Institutions tactically reduced positions, with cash levels slightly rising.

Amid concerns over crowded trades and potential bubbles, fund managers have shown a clear defensive tilt in their overall asset allocation.

Bank of America’s report noted that although investors remain broadly bullish, the degree of bullishness has cooled compared to May. Respondents cut their net overweight allocation to global equities by 12 percentage points to 38% and reduced their net overweight position in the technology sector to 26%.

Meanwhile, investors’ average cash levels rose slightly from 3.9% in May to 4.1%. Hartnett stated in the report that this suggests traders are taking some chips off the table ahead of summer.

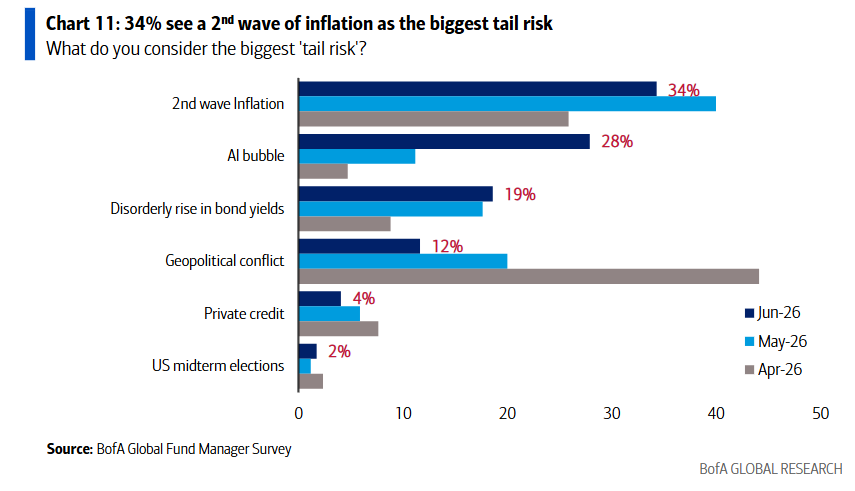

In terms of risk appetite, market perceptions of tail risks have also shifted significantly.

Thirty-four percent of fund managers identified 'a second wave of inflation' as the biggest tail risk to markets, while the share citing an 'AI bubble' as the top risk surged to 28%, up sharply from 5% two months ago. In contrast, concerns over geopolitical conflict dropped precipitously to 12% from 44% two months prior.

Divergence emerges in Asia-Pacific markets as capital rotates into defensive sectors.

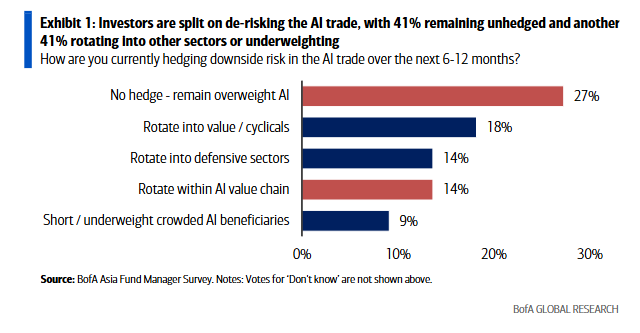

In the Asia-Pacific region, investors are showing clear divergence in their hedging strategies against the downside risks of AI-related trades.

According to Bank of America’s survey of Asian fund managers, 41% of respondents chose not to hedge and maintained their overweight positions in AI-related trades; equally, 41% opted to reduce risk by shorting or underweighting crowded AI beneficiary stocks, or rotating into other segments of the AI value chain and defensive sectors to mitigate potential volatility.

From a sector allocation perspective, significant rotation is underway in the Asia-Pacific region (excluding Japan). In June, investors rotated out of materials and consumer discretionary sectors and into financials and telecommunications. Currently, fund managers’ overweight position in tech hardware has surpassed that in semiconductors, and financials have emerged as the new favored sector.

Regarding specific markets, Taiwan, China is still regarded as the biggest beneficiary of the AI cycle, receiving recognition from 41% of respondents. In Japan, earnings expectations are increasingly becoming a key driver of equity markets, with technology hardware and banks jointly emerging as the second-most favored sectors, trailing only semiconductors.

Although there are signs of profit-taking at elevated market levels, only 9% of global investors believe the positive impact of AI on equity markets has been fully priced in, underscoring the theme's enduring appeal over the long term.

Editor/Deng