Western Securities believes that the ceasefire agreement contains numerous provisions unfavorable to the United States and fails to impose substantive constraints on Iran's nuclear issue, leaving the underlying geopolitical tensions in the Middle East unresolved. A deeper implication lies in the weakening foundation of the 'petrodollar' system, as cracks in the credibility of the U.S. dollar are widening at an accelerating pace, potentially ushering in gold’s fourth major upward cycle.

Trump announced a U.S.-Iran ceasefire, prompting a sharp rally in global risk assets. However, the unusual signal of gold rising in tandem is warning investors that this 'TACO rally' differs from previous episodes, with its hidden cost potentially being an accelerating erosion of dollar credibility.

On June 14, Trump announced that the U.S. and Iran had reached a ceasefire agreement, prompting a broad rally in global risk assets the following day. The strategy team at Western Securities noted that recently$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$yields surged again, briefly breaking above 4.5%, and the resulting liquidity risk was the primary reason “forcing” Trump to urgently seek a ceasefire. However, unlike the situation in May last year when Trump suspended the tariff war, this ceasefire agreement contains numerous provisions unfavorable to the United States and fails to impose substantive constraints on Iran’s nuclear program. Consequently, the fundamental tensions underlying Middle Eastern geopolitical risks remain unresolved.

More concerning is that gold prices have risen concurrently with the rally in risk assets—a 'synchronized' signal that starkly diverges from market behavior during the May 2025 pause in the tariff war. Western Securities argues that Trump’s urgency to disengage from the U.S.-Iran conflict has instead sent a critical signal to markets: the U.S. may no longer be able to unilaterally uphold order in the Middle East, the foundation of the 'petrodollar' system is weakening, and cracks in dollar credibility could widen rapidly, potentially triggering gold’s fourth major upward wave.

More concerning is that gold prices have risen concurrently with the rally in risk assets—a 'synchronized' signal that starkly diverges from market behavior during the May 2025 pause in the tariff war. Western Securities argues that Trump’s urgency to disengage from the U.S.-Iran conflict has instead sent a critical signal to markets: the U.S. may no longer be able to unilaterally uphold order in the Middle East, the foundation of the 'petrodollar' system is weakening, and cracks in dollar credibility could widen rapidly, potentially triggering gold’s fourth major upward wave.

Two TACOs, vastly different contexts

To understand the limitations of this ceasefire-driven market rally, it must be contrasted with the tariff-war-related TACO episode in May 2025.

In mid-May last year, U.S. Treasury yields breached 4.5% and surged rapidly, and the resulting liquidity risks compelled Trump to announce a delay in the global tariff war. At that time, Trump held full discretion over whether to impose global tariffs; once he opted for TACO, tariff-related risks were temporarily resolved, U.S. Treasury yields quickly retreated, and global risk assets experienced a 'synchronized rally.'

This time, the situation is entirely different.

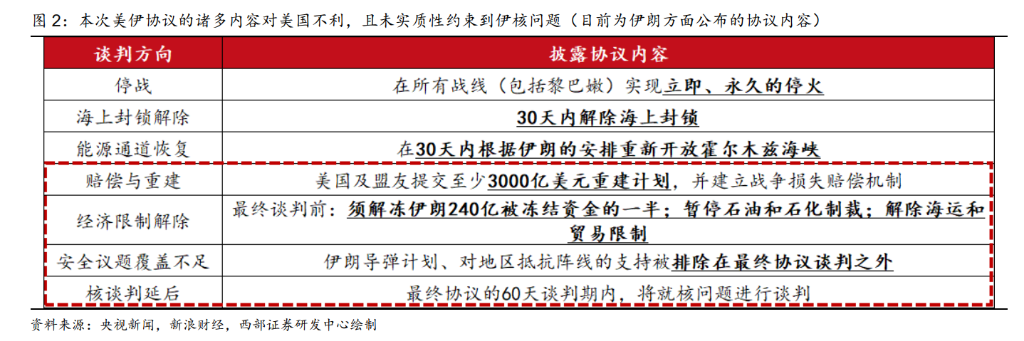

The report notes that, according to disclosures by Iran’s Mehr News Agency, the U.S.-Iran ceasefire agreement requires the United States and its allies to provide no less than $300 billion for Iran’s national economic recovery plan—effectively a form of 'war reparations'—introducing significant uncertainty into future negotiations. According to Xinhua News Agency, citing Trump on Tuesday, the U.S. will not invest any funds in Iran.

More importantly, resolving Middle East geopolitical risks does not hinge solely on Trump’s will—the extent of U.S. influence over Israel’s potential escalation of regional tensions remains uncertain, and Iran holds primary leverage over whether the Strait of Hormuz can return to pre-conflict conditions of free navigation.

U.S. Treasury yields are 'prone to rise but hard to fall,' and the ceasefire fails to address the underlying contradictions.

Western Securities had previously noted in its report that unless the U.S. can swiftly de-escalate the U.S.-Iran conflict, U.S. Treasury yields may face upward pressure with limited room to decline. This assessment remains valid under current circumstances.

First, the Shiite 'Axis of Resistance'—comprising Lebanon, Iran, and Yemen—has not yet disintegrated. One prerequisite for a U.S.-Iran ceasefire is restraining Israel from further attacks on Lebanon, which appears difficult to achieve at present.

Second, traffic through the Strait of Hormuz remains subdued, and it will take time for normal navigation to resume.

More critically, unless the U.S. gains actual control over the Strait of Hormuz, even if freedom of navigation is nominally restored, major global economies will remain concerned about the risk of Iran reimposing a blockade, potentially prompting significant oil stockpiling. This implies that the vicious cycle of high oil prices, elevated inflation, and high U.S. Treasury yields is unlikely to be broken in the near term, limiting the downside potential for Treasury yields.

Widening cracks in U.S. dollar credibility may herald the start of gold’s fourth wave

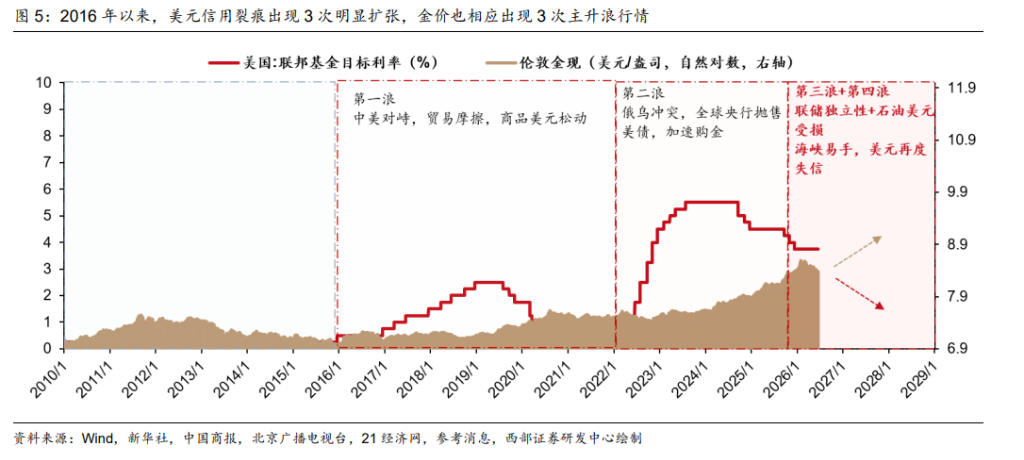

Western Securities believes the deeper impact of the current U.S.-Iran conflict lies in its undermining of the foundation of the 'petrodollar' system—a key to understanding the unusual phenomenon of simultaneous rallies in both gold and risk assets. The firm explicitly states that this development could trigger gold’s 'fourth wave' rally.

The firm has outlined three episodes since 2016 during which cracks in U.S. dollar credibility widened:

During the 2016 South China Sea tensions between China and the U.S., America attempted to suppress renminbi internationalization to reinforce dollar dominance, inadvertently weakening the 'commodity-dollar' system; consequently, gold prices rose sharply against the backdrop of the Federal Reserve’s 2016–2019 tightening cycle;

During the 2022 Russia-Ukraine conflict, the U.S. sought to bolster dollar credibility by disrupting Russia-Europe economic integration, which instead accelerated global central banks’ gold purchases,

leading gold prices to rise again during the 2022–2024 Fed hiking cycle despite higher interest rates.

In the current U.S.-Iran conflict, the United States initially sought to strengthen the 'petrodollar' by driving up global oil prices. However, the substantive shift in control over the Strait of Hormuz has instead undermined the Middle Eastern geopolitical foundation of the petrodollar. Western Securities notes that deindustrialization has led to a structural weakening of U.S. military capabilities, which is the primary reason for the widening credibility gap of the U.S. dollar—and each U.S. attempt to restore dollar credibility has paradoxically accelerated the expansion of this fissure.

Trump’s urgency to extricate TACO from the U.S.-Iran conflict underscores the fragility of U.S. Treasury debt, the dollar, and equity market liquidity, and formally signals to the market that following the loosening of the 'commodity-dollar' system, the 'petrodollar' system may also be on the verge of unraveling.

Based on the above assessment, Western Securities recommends continuing to focus on a 'barbell strategy' for asset allocation centered on 'AI plus inflation-driven gains.'

On one hand, monetary policy remains accommodative, and AI has not yet entered a bubble phase, though investors must accept the high volatility inherent in AI computing hardware (including telecommunications equipment, semiconductors, and memory). On the other hand, potential Federal Reserve quantitative easing (QE) could present an opportunity to repair domestic balance sheets burdened by debt; investors should both capitalize on the PPI-driven price-increase chain (coal, oil, chemicals, and new energy) and patiently await the CPI-driven price-increase chain later this year, which will be propelled by balance sheet repair (real estate, baijiu, etc.).

Editor/melody