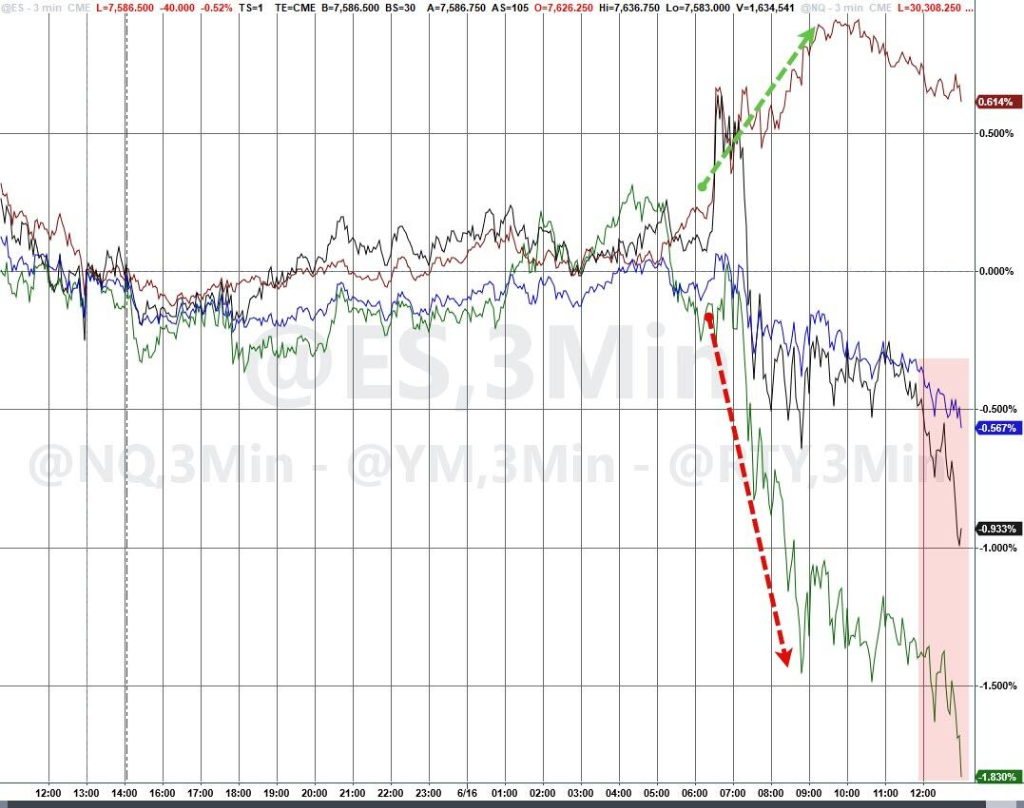

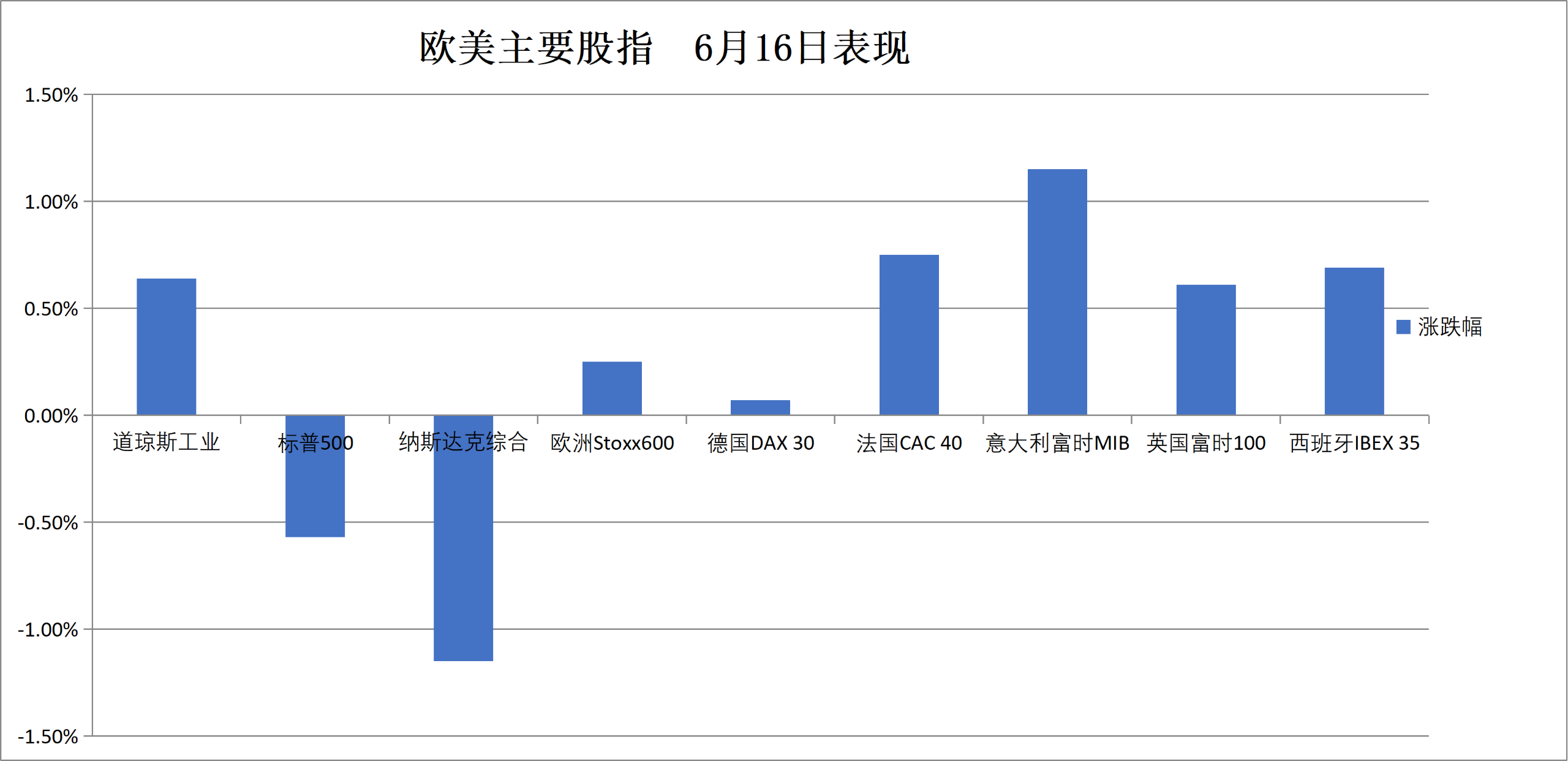

The Dow Jones Industrial Average rose 0.64%, reaching a new all-time high, while the Nasdaq Composite fell 1.15% and the S&P 500 declined 0.57%. Semiconductor stocks plunged, with the Philadelphia Semiconductor Index dropping 5.7% in a single day. Details of the U.S.-Iran peace agreement continue to emerge, pushing WTI crude oil futures below $75 per barrel intraday—the lowest level this year—and driving U.S. Treasury yields lower, with the 30-year yield closing below the 5% mark.

Technology stocks faced heightened selling pressure, crude oil prices underwent a sharp correction, and U.S. Treasury yields declined, leading to a markedly divergent performance across U.S. equities on Tuesday, as market attention shifted entirely to the Federal Reserve’s upcoming policy meeting—the first chaired by new Fed Chair Kevin Warsh.

The Dow Jones Industrial Average rose 0.64%, hitting a new all-time high, while the Nasdaq Composite fell 1.15% and the S&P 500 declined 0.57%.

Semiconductor stocks plunged sharply, $PHLX Semiconductor Index (.SOX.US)$ dropping 5.7% in a single day. Microsoft (MSFT.US) announced the cancellation of a roughly $3 billion cloud capacity leasing agreement with Oracle, further dampening sentiment in the technology sector.

Semiconductor stocks plunged sharply, $PHLX Semiconductor Index (.SOX.US)$ dropping 5.7% in a single day. Microsoft (MSFT.US) announced the cancellation of a roughly $3 billion cloud capacity leasing agreement with Oracle, further dampening sentiment in the technology sector.

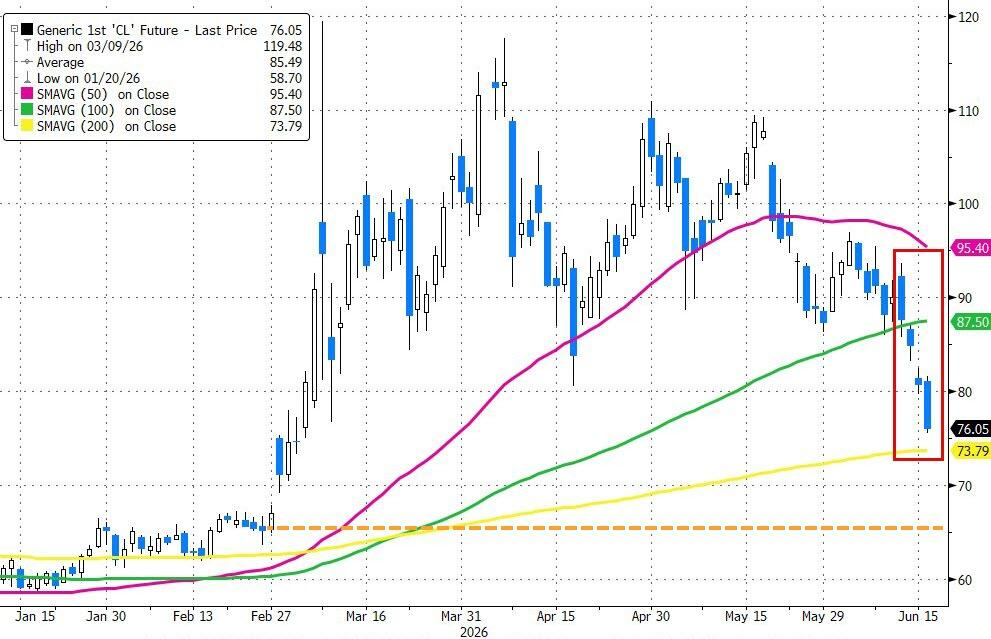

Meanwhile, details of the U.S.-Iran peace agreement continued to emerge, pushing WTI crude oil futures below $75 per barrel intraday—the lowest level this year—and driving U.S. Treasury yields lower, with the 30-year yield closing below the 5% mark.

Oil prices continued to slide as details of the Iran deal materialized

Mohammad Bagher Ghalibaf, a hardline Iranian figure, confirmed that a de facto peace agreement with the United States has already been signed, fueling expectations of the imminent reopening of the Strait of Hormuz.

At the G7 summit in Évian-les-Bains, France, Trump reiterated that the U.S. and Iran have signed an agreement and that bilateral relations have been "normalized." He plans to release the full text of the agreement and submit it to Congress for review, with the second phase of negotiations expected to proceed as scheduled.

He also emphasized that vessels have already begun transiting through the Strait of Hormuz, which will fully reopen by the 19th, adding that passage will be free of charge once permanently opened.

Driven by this, WTI crude oil has declined approximately 14% from its weekend high and has fallen more than 30% from its May peak, closing at $76.56 per barrel—approaching the 200-day moving average (around $73.79) and nearing pre-war levels.

In the physical market, prompt Brent crude prices have also continued converging toward pre-war levels, reflecting ample short-term supply.

Goldman Sachs promptly revised its forecast downward, lowering its Brent crude price target for Q4 2026 to $80 per barrel and setting a 2027 annual average target of $75, citing an earlier-than-previously-expected timeline for Middle Eastern supply recovery. Retail gasoline prices are expected to decline significantly as a result.

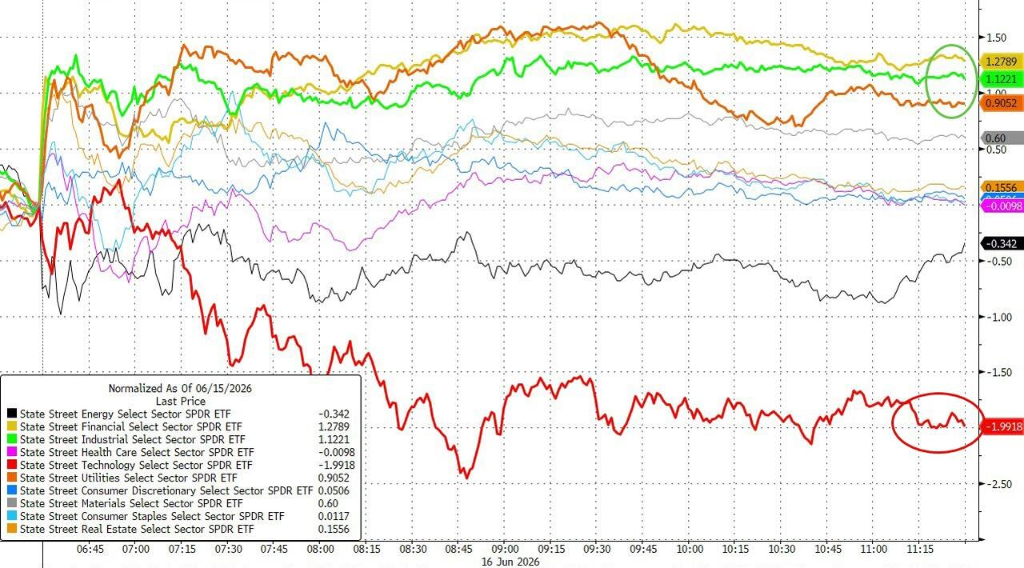

Technology stocks under pressure as sector rotation deepens

On Tuesday, U.S. technology stocks became the epicenter of selling pressure, with the Nasdaq dropping more than 1.5%, while the Dow Jones Industrial Average continued to close at record highs—marking the third-largest single-day divergence between the Dow and the Nasdaq this year.

U.S. semiconductor, memory, and software subsectors faced broad-based position reductions, amid news that Microsoft (MSFT.US) terminated a roughly $3 billion cloud capacity lease agreement with Oracle (ORCL.US) citing security concerns.

Notably, on the same day, more components of U.S. equity indices advanced than declined, further supporting the view that market leadership is broadening beyond the AI sector.

Meanwhile, financial stocks rose 1.5% and industrial stocks gained 0.7%, with defensive sectors outperforming across the board—further reinforcing the market narrative of sector rotation rather than systemic risk.

$SpaceX (SPCX.US)$ It became the most actively traded options underlying asset of the day, with its intraday market capitalization briefly surpassing $3 trillion—surpassing Amazon and nearing Microsoft—before closing up 4.8% at $201.80.

SpaceX’s share price has risen 49% from its IPO offering price of $135 per share, reflecting sustained strong investor demand and alleviating concerns that the record-breaking IPO might be too large for the market to absorb. The stock’s performance paves the way for potential public offerings this year by AI rivals Anthropic PBC and OpenAI, both of which are valued at approximately $1 trillion.

Angelo Kourkafas, Senior Global Investment Strategist at Edward Jones, noted that only about 4.2% of shares are freely tradable, and the significant price volatility is partly attributable to the extremely limited float.

Max Gokhman, Senior Vice President of Investment Solutions at Franklin Templeton, cautioned that once lock-up agreements begin to expire and insiders start selling shares, the stock could face heightened downward pressure.

UBS Group traders characterized the day’s trading activity as marked by “low liquidity and fragmentation,” emphasizing that it reflected “signs of fatigue in crowded AI/semiconductor positions rather than systemic deleveraging.”

Goldman Sachs’ trading desk rated the day’s market activity at 4 out of 10, noting a net skew of 9% toward selling across the board. Long-only institutions showed clear willingness to sell in the information technology and consumer discretionary sectors, while hedge fund selling skew reached 17%.

Bond markets strengthened, with Wallsh’s “debut” emerging as the key variable.

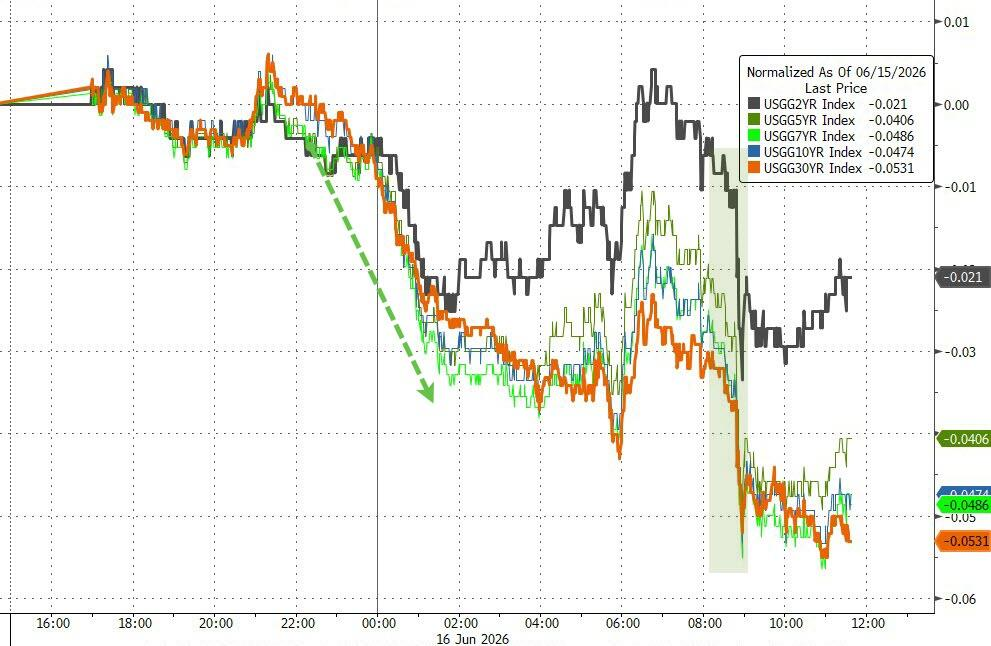

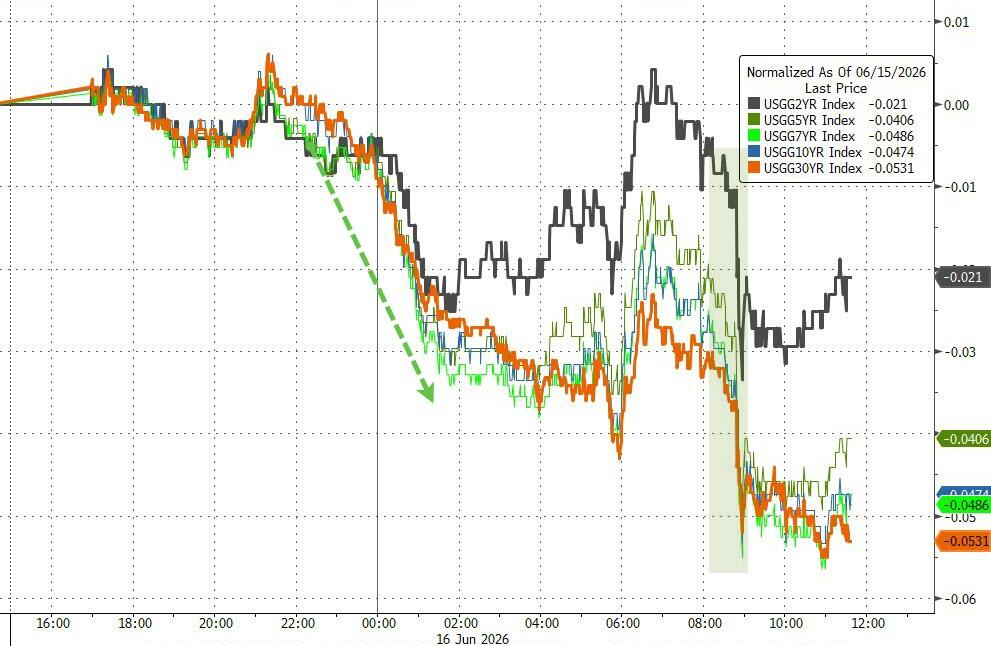

U.S. Treasury yields declined amid falling oil prices and weak housing starts data, further supported by stronger-than-expected demand at the 20-year bond auction. The 30-year Treasury yield closed below 5%, marking its lowest close since April 24; the 10-year yield dropped 4 basis points to 4.44%.

David Robin, interest rate strategist at TJM Institutional Services, stated that oil prices have fallen sharply in the short term, but the market struggles to interpret their inflationary implications, saying:

The absence of clarity on whether the short-term effects or long-term uncertainties carry more weight is currently limiting the transmission of oil price movements to the interest rate market.

Market expectations for the Federal Reserve holding rates steady have become highly aligned, but Wallsh's debut is seen as a more substantive event. According to the CME FedWatch Tool, the probability of a 25-basis-point rate hike in December stands at approximately 43%.

eToro analyst Bret Kenwell noted:

Within just a few months, the market narrative has shifted from 'how many rate cuts this year' to 'how many rate hikes,' marking a significant reversal that places Wallsh in a difficult position: he could express patience by citing falling oil prices, but if the broader inflation trajectory veers off course, he cannot afford to appear complacent.

Bloomberg macro strategist Cameron Crise, meanwhile, is watching whether Wallsh might adjust the monetary policy communication framework itself, including whether to retain the Summary of Economic Projections (SEP) and the 'dot plot.'

He specifically highlighted that whether Wallsh submits his own forecast in this dot plot will be the first key signal to watch.

TD Securities strategists expect this meeting to show a diminished dovish tilt, upward revisions to inflation forecasts, and median rate projections for both 2026 and 2027 indicating no rate cuts. However, they anticipate Wallsh will avoid sending an overly hawkish signal to preserve his credibility.

Bloomberg macro strategist Michael Ball summarized that with the U.S.-Iran deal lowering immediate geopolitical tensions, this FOMC meeting will determine whether the current rally can broaden its participation. If Wallsh signals policy patience, it would mechanically lower real interest rates, effectively amounting to a dovish policy stance.

The dollar retreated toward its previous session’s low.

Gold prices edged higher, approaching the prior session’s high.

$Bitcoin (BTC.CC)$ Prices fell below $66,000.

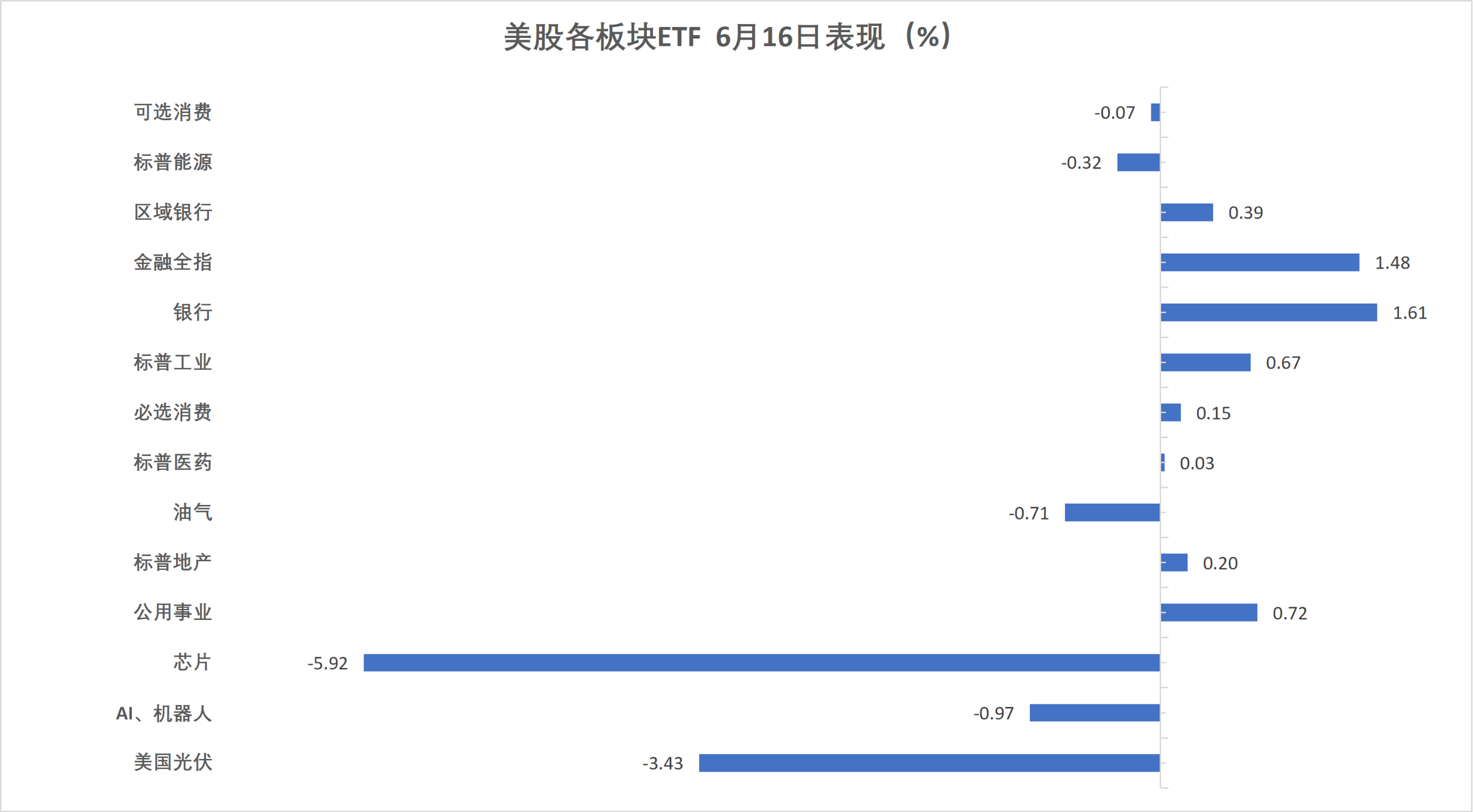

On Tuesday, the U.S. semiconductor ETF fell by 4.8%, leading losses among U.S. sector ETFs, while the S&P financials sector rose nearly 1.5%.

U.S. benchmark indices:

The S&P 500 Index declined 42.94 points, or 0.57%, closing at 7,511.35.

The Dow Jones Industrial Average rose 328.64 points, or 0.64%, closing at 51,999.67 and setting another record high, with a cumulative gain of 4.17% over the past four trading days.

The Nasdaq Composite fell 307.597 points, or 1.15%, closing at 26,376.344. The Nasdaq 100 Index dropped 575.789 points, or 1.89%, ending at 29,968.13.

The Russell 2000 Index declined 0.87%, closing at 2,939.195.

The CBOE Volatility Index (VIX) rose 1.30%, closing at 16.41.

U.S. stock sector ETFs:

The semiconductor ETF fell 4.81%, while technology sector ETFs and global tech equity index ETFs declined by at least 2.65%. In contrast, the banking sector ETF gained 0.57%, and the financials sector ETF rose 1.47%.

Mag 7:

The Wind U.S. Magnificent 7 Index declined 0.37%.

$NVIDIA(NVDA.US)$ down 2.37%, Tesla down 1.58%, Microsoft down 1.48%, Amazon down 0.01%, $Apple(AAPL.US)$ up 0.95%, Google-A (GOOGL.US) up 1.06%, Meta up 1.13%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ closed down 805.399 points, or 5.71%, at 5953.27.

Taiwan Semiconductor (TSM.US) ADRs down 3.51%, Advanced Micro Devices (AMD.US) down 7.30%, $Intel (INTC.US)$ Dropped more than 8%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 2.50% at 6192.86, breaking below its April 8, 2025 closing level of 6198.18 and approaching its September 23, 2024 closing level of 5917.72.

Among actively traded Chinese ADRs, ASE Semiconductor fell 4.5%, Pony AI, Xpeng Group (XPEV.US) down over 4%, Tencent, Meituan, $Nio (NIO.US)$ Baidu, and NetEase down over 3%.

Other individual stocks:

$Circle(CRCL.US)$ Down 4.34%.

Eurozone blue-chip stocks rose more than 0.4%, extending their record closing highs, with UniCredit leading gains by climbing approximately 4.2%. Italy's banking sector closed up 3%, alongside the broader Italian and Spanish equity markets, which also hit new record closing highs.

Pan-European Index:

The pan-European STOXX 600 index closed up 0.25% at 636.00 points, marking its second consecutive trading day at a record closing high.

The Eurozone STOXX 50 index closed up 0.45% at 6,257.42 points, also reaching another record closing high.

Major Stock Indexes Around the World:

Germany's DAX 30 index closed up 0.07% at 24,910.41 points.

France's CAC 40 index closed up 0.75% at 8,447.27 points.

The UK's FTSE 100 index closed up 0.61% at 10,494.21 points.

Sector and individual stock performance:

Among Eurozone blue chips, UniCredit closed up 4.17%, Adyen gained 3.66%, Intesa Sanpaolo rose 2.91% to rank third, BBVA advanced 2.43%, and Hermès added 2.19%.

Among all constituents of the STOXX Europe 600 Index, Allegro.eu SA rose 7.78%, GEA Group gained 5.08%, Belimo Holding advanced 4.27%, UniCredit posted the fourth-largest gain, and Camurus AB fell 6.39%, marking the third-largest decline.

Long-end U.S. Treasury prices posted notable gains, with the two-year real yield rising by more than 6.6 basis points. Sovereign bonds across the eurozone broadly declined, with the 10-year Italian government bond yield dropping by over 4 basis points.

U.S. Treasuries:

At the close of New York trading, the yield on the 10-year U.S. Treasury note fell 5.13 basis points to 4.4217%.

The yield on the two-year U.S. Treasury note declined 2.31 basis points to 4.0432%, while the 30-year U.S. Treasury yield dropped 5.31 basis points to 4.9274%.

European bonds:

At the close of European trading, the yield on Germany’s 10-year government bond fell sharply again, ending down 2.4 basis points at 2.930%, having traded within a range of 2.959%–2.920% during the session.

The yield on the UK’s 10-year gilt declined 2.4 basis points to 4.788%. The two-year UK gilt yield rose 1.1 basis points to 4.184%.

The 10-year sovereign bond yields in France, Italy, Spain, and Greece declined by up to 4.1 basis points.

The Bloomberg Dollar Spot Index fell 0.12% to 1204.72, trading within a range of 1207.31–1204.02 during the session.

Dollar:

At the close of New York trading, the ICE U.S. Dollar Index declined 0.09% to 99.543, with intraday trading ranging between 99.791 and 99.461.

The Bloomberg Dollar Spot Index fell 0.12% to 1204.72, trading within a range of 1207.31–1204.02 during the session.

Non-USD currencies:

At the New York close, the euro rose 0.18% against the US dollar to USD 1.1612, while the British pound gained 0.13% to USD 1.3431. The US dollar fell 0.17% against the Swiss franc to CHF 0.7931.

Among commodity-linked currencies, the Australian dollar was largely flat against the US dollar, showing a V-shaped intraday pattern on the day the Reserve Bank of Australia held rates steady. The New Zealand dollar rose 0.26% against the US dollar, while the Canadian dollar was broadly unchanged, exhibiting an M-shaped trading pattern overall.

Japanese yen:

At the New York close, the US dollar rose 0.05% against the Japanese yen to JPY 160.41, trading within a range of JPY 160.05–160.46 during the session.

The euro rose 0.23% against the yen to JPY 186.27, and the British pound gained 0.17% to JPY 215.438.

Offshore renminbi:

At the New York close, the US dollar traded at CNY 6.7566 against the offshore renminbi, up 27 pips from Monday’s New York close, with intraday trading ranging between CNY 6.7635 and CNY 6.7551.

Cryptocurrencies:

At the New York close, Bitcoin spot prices declined 1%, while Ethereum fell 1.14%.

Abu Dhabi Murban crude oil futures dropped 6.94% to USD 71.87 per barrel, briefly falling to USD 71.56 at 00:32 Beijing time, approaching the February 25 level of USD 70.21 and the February 18 low of USD 69.42.

Crude Oil:

WTI July crude oil futures settled down $4.70, or 4.99%, at $76.05 per barrel.

Brent August crude oil futures declined by $4.21, or 5.06%, to settle at $78.96 per barrel.

Middle East Abu Dhabi Murban crude oil futures dropped 6.94% to $71.87 per barrel.

Natural Gas:

NYMEX July natural gas futures settled at $3.2390 per million British thermal units (MMBtu).

Spot gold rose approximately 0.5%, silver was flat, and platinum gained 2%.

Gold:

At the New York close, spot gold rose 0.48% to $4,332.23 per ounce.

COMEX gold futures rose 0.08% to $4,355.20 per ounce.

Silver:

At the New York close, spot silver was largely unchanged at $69.9850 per ounce, trading within a range of $69.0730–$71.1951 during the session, with the day’s high reached at 21:00.

COMEX silver futures were largely unchanged at $70.160 per ounce, having reached $71.310 at 21:00.

Other metals:

At the close of New York trading, COMEX copper futures fell 0.11% to $6.5510 per pound.

Spot platinum rose 2.02%, while spot palladium gained 0.75%.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen