China Merchants Securities noted that the AI industry chain is experiencing an unusual price divergence: upstream components such as memory, optical modules, and power equipment continue to rise in price due to supply constraints, while downstream tokens are caught in a wave of price cuts. However, lower token prices drive higher usage volumes. Market focus is shifting from capital expenditure expansion toward validating monetization of computing power. As the RMB 2 trillion computing infrastructure investment materializes, domestically produced chips, power, and energy storage may emerge as the strongest thematic drivers.

The pricing dynamics across the AI supply chain are diverging. Upstream components—such as memory, CPUs, and optical modules—are experiencing price increases, while downstream token prices are falling competitively. Both trends are occurring simultaneously and show signs of accelerating.

In a strategy weekly report released on June 15, Zhang Xia of China Merchants Securities wrote: 'The AI supply chain is currently undergoing an unusual structural pricing shift. Upstream computing resource prices continue to inflate due to rigid supply-side constraints, while downstream token consumption prices continue to deflate amid rapid advancements in model capabilities and intensifying market competition.'

This is not merely a simple question of whether AI remains viable. From 2023 to 2025, markets primarily priced in the certainty of capital expenditure expansion by leading overseas tech giants and domestic Chinese enterprises. Entering 2026—particularly after June—market sentiment began to diverge: upstream hardware price hikes still support earnings expectations, whereas downstream applications now face scrutiny over whether declining token prices can translate computing power into stable cash flows and profits.

This is not merely a simple question of whether AI remains viable. From 2023 to 2025, markets primarily priced in the certainty of capital expenditure expansion by leading overseas tech giants and domestic Chinese enterprises. Entering 2026—particularly after June—market sentiment began to diverge: upstream hardware price hikes still support earnings expectations, whereas downstream applications now face scrutiny over whether declining token prices can translate computing power into stable cash flows and profits.

The key question is whether lower token prices will drive sufficient volume growth to offset the decline in unit prices.

Upstream: Supply cannot keep up—price increases are inevitable.

The immediate trigger for upstream inflation is a surge in raw material prices.

Tungsten hexafluoride serves as a prime example. Korean suppliers have notified Samsung and SK Hynix of a 70%–90% price increase for their 2026 tungsten hexafluoride contracts. In April, major Japanese suppliers such as Kanto Denka also issued warnings about potential supply disruptions. According to Caixin, the price of 99.999%-purity tungsten hexafluoride in China has risen to RMB 1,670–1,810 per kg, up 232.7% from RMB 523 per kg a year earlier.

Rising prices for electronic-grade glass fabric are also fueling the upstream trend. Looking further ahead, AI-related hardware—including memory, CPUs, and optical modules—continues to follow an upward pricing trajectory.

Price increases are quickly reflected in market trading because they directly impact EPS. When valuations are already elevated, investors favor earnings upgrades; clear-cut pricing dynamics with easily trackable data naturally become the entry point for capital allocation toward upstream AI stocks.

The more medium-term driver is supply-demand mismatch. Rapidly rising capital expenditures by cloud providers are generating sustained demand for GPUs, memory, optical modules, PCBs, power distribution systems, and related components. However, upstream capacity expansion involves lead times, preventing immediate supply response.

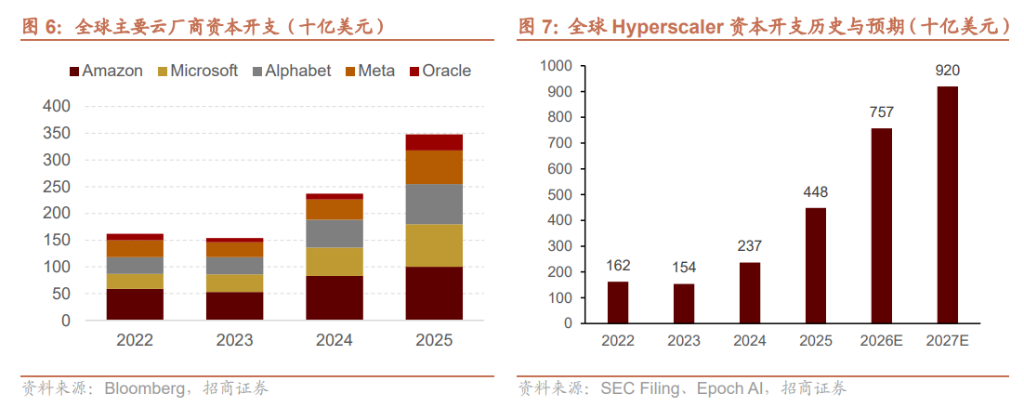

Global hyperscaler capital expenditures are projected to rise from $162 billion in 2022 and $154 billion in 2023 to $448 billion in 2025, with expectations of $757 billion in 2026 and $920 billion in 2027. The demand curve is so steep that upstream prices struggle to remain stable.

Both Samsung and SK Hynix indicated in their April–May 2026 earnings reports and investor communications that AI-driven memory shortages will persist through 2027 and beyond, with some key customers already securing 2027 capacity in advance.

Downstream: Prices are falling, but usage is exploding.

Token prices downstream are indeed falling—and falling rapidly.

The Silicon Data LLM Token Spend Index, which measures total market token expenditure, has recently posted its first significant decline following a one-sided rally since February this year—enterprises are now anticipating further reductions in mainstream large model token pricing and are deferring purchases accordingly. OpenAI is considering a substantial reduction in token fees, driven by competitive pricing pressure from Anthropic; Tencent Cloud has already announced a 66.67% price cut for inputs on certain models.

Yet at the same time, usage volume is growing explosively.

Economics features the 'Jevons Paradox'—when the efficiency of a resource improves and its cost declines, total demand often rises rather than falls, as lower usage barriers unlock new applications. This pattern has been observed historically with coal, electricity, and communication bandwidth—and now it is tokens’ turn.

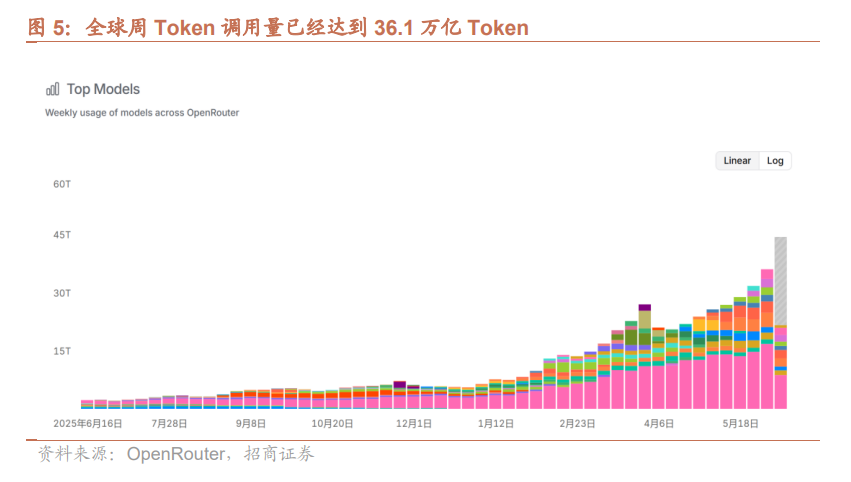

According to OpenRouter data, as of June 8, 2026, global weekly token usage had already reached 36.1 trillion and continues to grow exponentially.

Domestic figures are even more striking: the number of generative AI users in China grew from 249 million at the end of 2024 to 515 million by mid-2025—roughly doubling—while daily average token consumption surged from approximately 100 billion to 14 trillion by Q1 2026—an increase of about 1,400 times. With user numbers up only twofold but consumption up 1,400-fold, the primary driver of growth is clearly not new users, but deeper per-user utilization and the rapid adoption of agent-type applications.

Chinese vendors’ low-price strategy has proven highly effective in this competition. The most widely used models globally are DeepSeek and Tencent HunYuan—not the overseas flagship models that score higher on capability benchmarks. By late 2025, open-source models already accounted for nearly one-third of total token usage by weight, with a large number of developers beginning to substitute DeepSeek and Qwen for certain closed-source APIs.

From an investment perspective, the key variable determining the revenue potential of the AI industry is not the price per token, but the growth rate of total token consumption. As long as the latter continues to outpace the rate at which token prices decline, the industry’s aggregate revenue will not shrink.

Market trading dynamics are shifting.

Between 2023 and 2025, the market priced in the certainty of CAPEX expansion—if major players kept spending heavily, upstream hardware suppliers would secure orders.

By June 2026, this logic began to diverge. Upstream segments continued to rally, while downstream sectors intensified competition, prompting the market to confront a harder question: Can computing power be converted into sustainable cash flows and profits?

Last week, A-share market performance delivered a negative signal regarding deflationary pressures in AI downstream segments. However, from a macro perspective, the key determinant of the sector’s growth potential is not the price per token, but the growth rate of total token consumption. As long as demand growth consistently exceeds the pace of price declines, the AI industry’s overall revenue scale can still expand.

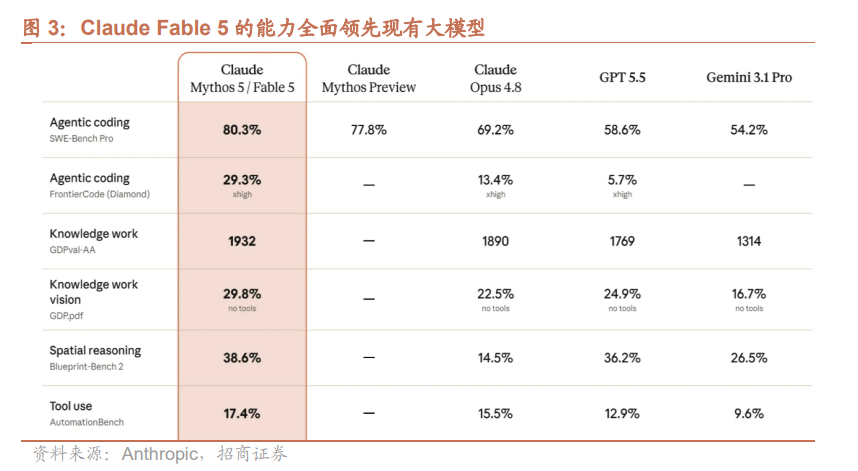

Anthropic’s release of Claude Fable 5 on June 9 serves as a prime example of how top-tier AI firms are recalibrating their strategic priorities.

Fable 5 surpasses all previously publicly available models across the board, with its lead widening significantly on longer and more complex tasks. Yet, its pricing is less than half that of the earlier Mythos Preview—$10 per million input tokens and $50 per million output tokens.

Rather than charging premium prices at peak capability, the company adopted a more aggressive pricing strategy. The reason is straightforward: for enterprise clients, benchmark-leading performance is no longer the top priority; what matters most is the ability to deploy AI solutions at scale and at low cost.

Where is the RMB 2 trillion in computing infrastructure investment flowing?

On the policy front, the 'Guidelines on National Data Infrastructure Development,' issued in January 2025, clarified investment priorities for the upcoming Five-Year Plan period. Industry estimates suggest that data infrastructure will attract approximately RMB 400 billion in direct annual investment, catalyzing a total investment of roughly RMB 2 trillion over the next five years. Meanwhile, this round of computing infrastructure development mandates that at least 80% of AI chips must come from domestic suppliers such as Huawei and Cambricon, effectively excluding NVIDIA and AMD.

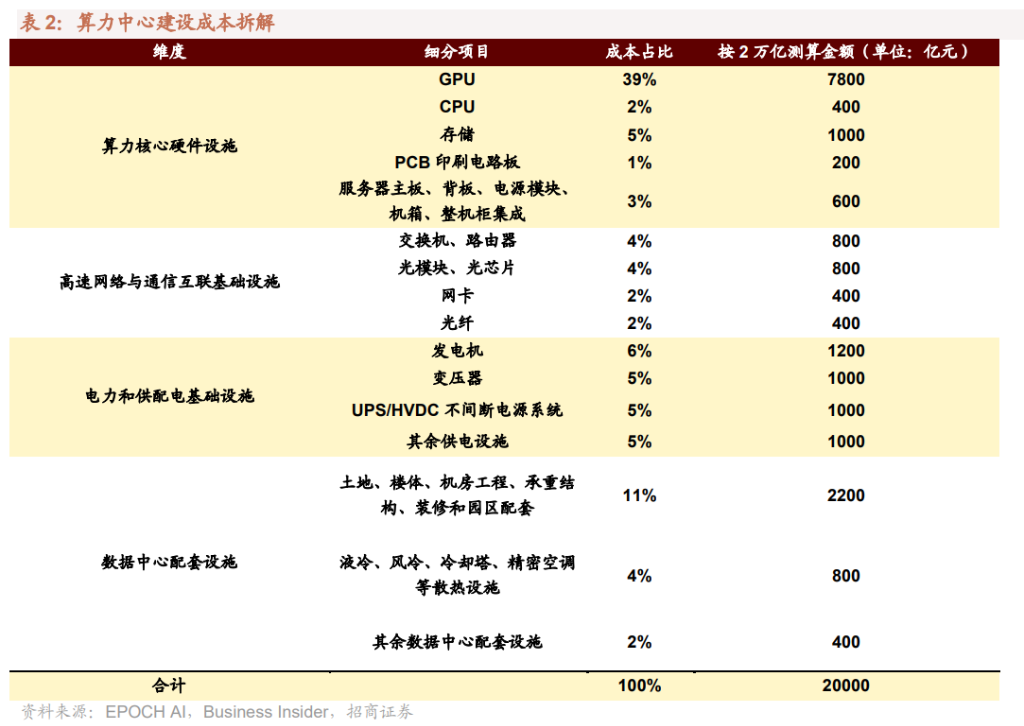

According to EPOCH AI estimates, the upfront capital expenditure for a typical 1 GW AI data center is approximately USD 38 billion. Based on the total investment of RMB 2 trillion, the estimated benefits by segment are as follows:

GPU chips: accounting for 39%, equivalent to approximately RMB 780 billion—this is the segment with the highest elasticity across the entire supply chain.

Power and power distribution systems: accounting for 21%, or approximately RMB 420 billion (with generators, transformers, and UPS each contributing roughly RMB 100–120 billion).

Land, building structures, and data center construction: accounting for 11%, or approximately RMB 220 billion.

Optical modules, switches, and cooling infrastructure: each accounting for 4%, or approximately RMB 80 billion per category, together representing 12% of the total.

Based on the RMB 2 trillion total investment estimate, approximately RMB 780 billion will flow into domestically produced computing chips. Spread over five years, this translates into annual demand exceeding RMB 150 billion for domestic AI chips.

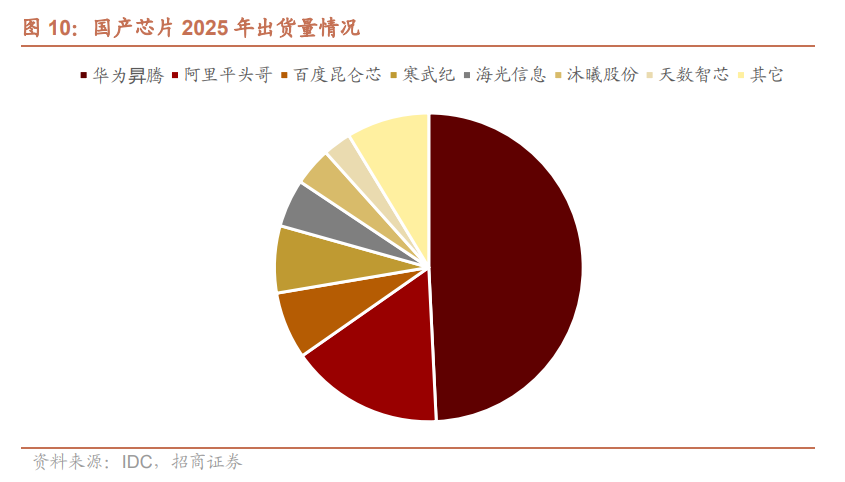

Domestic substitution is progressing faster than many anticipated. In 2025, domestically produced chips are expected to capture approximately 41% of the overall market share, rising above 52% in the first half of 2026—surpassing NVIDIA. Huawei Ascend emerged as the biggest winner, shipping 812,000 units in 2025, accounting for nearly half of total domestic chip shipments; Alibaba Pingtouge ranked second with 265,000 units; Baidu Kunlunxin and Cambricon each shipped approximately 116,000 units.

In May 2026, the China Information Technology Security Evaluation Center listed “AI training and inference chips” as a separate evaluation category for the first time. Nine products—including the Ascend 310/910 and Cambricon Zhenwu M530/M890—received Level I certification, valid for three years. This certification carries direct implications for procurement decisions by government agencies, central state-owned enterprises, and telecommunications operators.

Power infrastructure—a beneficiary segment that has been underestimated

Of the RMB 2 trillion invested in computing infrastructure, approximately RMB 420 billion will drive supporting investments in power systems, cooling solutions, and network equipment.

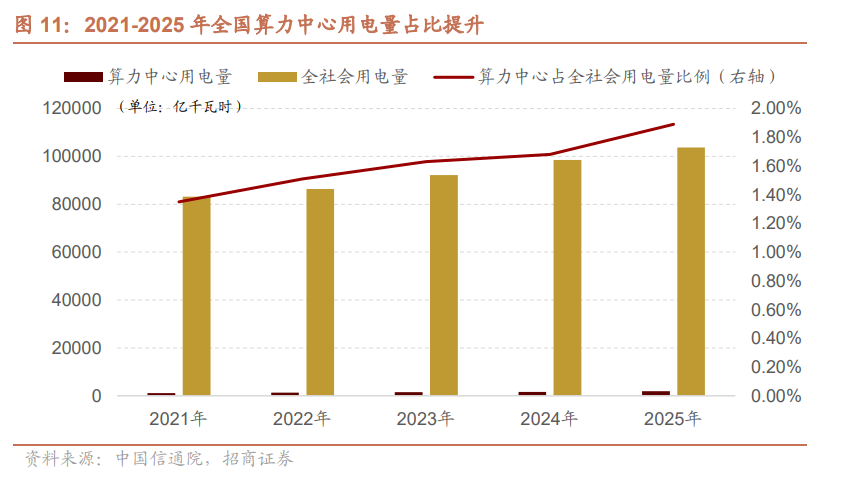

According to data from the China Academy of Information and Communications Technology (CAICT), national data center power consumption reached 196 billion kilowatt-hours in 2025, growing significantly faster than the average growth rate of total societal electricity consumption. The National Energy Administration forecasts that during the 15th Five-Year Plan period (2026–2030), annual新增 power demand from computing infrastructure will exceed 100 billion kilowatt-hours, reaching approximately 800 billion kilowatt-hours by 2030—accounting for about 6% of total national electricity consumption.

"East Data West Computing" and "computing-power-electricity coordination" have been clearly established as national policy directions. The underlying logic is as follows: computing demand is concentrated in the east, while the west is rich in wind, solar, and hydro resources—relocating computing capacity westward can absorb green electricity, while "west-to-east power transmission" still requires highly efficient transmission infrastructure. High-density AI server racks impose stringent demands on power supply stability, directly driving demand for high-efficiency energy-saving transformers and high-voltage direct current (HVDC) power systems.

The role of energy storage is also evolving. Data centers require uninterrupted 24/7 power supply; energy storage can serve not only as an emergency backup alternative to diesel generators but also as a primary power source that supplies routine electricity via grid connection. By the end of 2025, China had commissioned 136 GW / 351 GWh of new-type energy storage capacity, an 84% increase from the end of 2024—AI infrastructure is emerging as a key driver of incremental energy storage demand.

Finally, consider three factors: pricing, usage volume, and capital expenditure.

This round of differentiation within the AI industry chain cannot be adequately summarized simply as 'strong upstream, weak downstream.'

Upstream price increases must be assessed based on whether they can be passed through to profitability. Short-term price hikes in materials, memory, optical modules, and power distribution equipment are more readily reflected in market transactions, but it also depends on whether post-expansion supply-demand dynamics ease.

Downstream token price reductions should be evaluated against usage volume. As long as the growth rate of total token consumption outpaces price declines, the overall revenue scale of the AI industry can still expand. Conversely, if price cuts fail to generate sufficient additional usage, pressure on application-layer players will become more pronounced.

Computing infrastructure hinges on whether CAPEX can be effectively deployed. A RMB 2 trillion investment in data infrastructure, domestic substitution of AI chips, and supporting power and energy storage systems represent the most concrete levers in this value chain.