Source: Barron's

Buffett once said: 'Investing is a baseball game without a strike zone—you're simply waiting for your home run.' Most of the time, skilled investors are just waiting. In his book Value Investing: Tools and Techniques for Intelligent Investment, renowned GMO asset management investor James Montier illustrates through the example of a goalkeeper saving penalty kicks and a behavioral investing experiment that investing should be boring—and sometimes doing nothing may be better than doing something.

Below is the full translation of Chapter 17, 'Beware of Action Man,' from the book:

What do a goalkeeper facing a penalty kick and an investor have in common? The answer is that both tend to take action—they feel compelled to do something. Yet waiting is also an option, and sometimes holding cash is perfectly acceptable. However, for many fund managers, this remains a curse. Perhaps they would do well to remember Paul Samuelson’s advice: investing should be boring. It shouldn’t be exciting. Investing ought to be more like watching paint dry or grass grow.

What do a goalkeeper facing a penalty kick and an investor have in common? The answer is that both tend to take action—they feel compelled to do something. Yet waiting is also an option, and sometimes holding cash is perfectly acceptable. However, for many fund managers, this remains a curse. Perhaps they would do well to remember Paul Samuelson’s advice: investing should be boring. It shouldn’t be exciting. Investing ought to be more like watching paint dry or grass grow.

Imagine you are the goalkeeper facing a penalty kick. You have no idea which direction the kicker will choose to shoot. You must simultaneously make an effective decision: dive left, dive right, or stay in the center of the goal line?

Most professional goalkeepers tend to dive either left or right. Surprisingly, in 94% of cases, choosing a direction is the preferred move. However, this is not the optimal strategy. If you examine the probability of saving a penalty, staying in the center of the goal line actually proves to be a wiser choice (assuming the kicker’s behavior remains unchanged). Goalkeepers exhibit a clear action bias.

Evidence from experimental markets shows that investors also display an action bias. For instance, in an artificial asset market where the fundamental value is easy to calculate and resale of shares is prohibited, trades above fundamental value should not occur. Yet, time and again, experiments demonstrate numerous transactions taking place well above fundamental value. This makes no sense whatsoever. Since resale is banned, participants cannot hope to offload the asset to a greater fool. Their trading behavior appears utterly pointless—action bias is indeed real.

Warren Buffett once likened investing to a wonderful baseball game in which no umpire calls balls and strikes. Investors can simply stand at home plate, watch pitches go by, and wait for the perfect pitch within their sweet spot to swing and hit a home run. Yet, as Seth Klarman noted, 'Most institutional investors feel compelled to abandon the option of choosing how often to swing and instead feel obligated to swing at every pitch.'

The legendary Bob Kirby once suggested we adopt a 'coffee can portfolio'—buying stocks and then ignoring them entirely—an approach he described as 'passive active investing.' However, Kirby also pointed out that this method is unlikely to gain widespread adoption because it could fundamentally alter the ecosystem of our industry and significantly reduce the quality of life for asset management professionals. Sounds like a great idea.

Some may not know that many years ago, when I was still a child, 'Action Man' was a popular toy soldier figure—a symbol of masculine values. One day after school, I came home to find my sister had kidnapped my 'Action Man' and forced him to play house with her Cindy doll. That experience delayed his impact on me somewhat. But setting aside my childhood trauma, would you really want an 'Action Man' managing your investment portfolio?

01. The Goalkeeper as an Action Man

Although not the star of the team during regular play, top goalkeepers become quintessential action-takers during penalty shootouts. A recent study by Bar-Eli et al. (2007) revealed some intriguing patterns in penalty-saving behavior. In soccer (a sport about which I know virtually nothing), when a penalty kick is awarded, the ball is placed 11 meters from the goal, setting up a direct duel between the goalkeeper and the kicker. The goalkeeper is not allowed to leave the goal line before the kick is taken.

Considering that in a soccer match with an average of 2.5 goals, a penalty kick (with an 80% chance of scoring) can significantly influence the outcome of the game. Thus, unlike many psychology experiments, the stakes here are very high.

The author analyzed 311 such penalty kicks from top-tier global leagues and tournaments. A panel of three independent referees was used to assess the direction of the shots and the goalkeeper’s movement. To avoid confusion, all directions (left or right) were reported from the goalkeeper’s perspective.

Very roughly speaking, the shots were uniformly distributed, with approximately one-third aimed at the left, center, and right of the goal, respectively. However, goalkeepers exhibited a clear behavioral bias: they almost always dove either left or right (94% of the time) and rarely stayed in the center of the goal line.

However, to evaluate the “optimal” behavior, we need to know the success rates associated with different combinations of shot and save directions. Table 17.2 illustrates this point. The best strategy is clearly for the goalkeeper to remain in the center of the goal—he saved 60% of shots directed at the center, far exceeding his success rate when diving left or right. Yet, deviating sharply from this optimal strategy, goalkeepers stayed in the center only 6.3% of the time! The behavioral bias exhibited by goalkeepers is evidently suboptimal.

The reason for this behavioral bias appears to be social norms. Goalkeepers feel they have at least made an effort when diving left or right, whereas standing still in the center and watching the ball go into the net on either side feels worse. Bar-Eli et al. confirmed this through surveys of elite goalkeepers.

02. Investors and Action Bias

To introduce you to evidence of investors’ action bias, I must first present the field of experimental economics, particularly experimental asset markets.

These are brilliant constructs for studying human behavior in financial market settings—stripped of any complicating factors. These markets are extremely simple, consisting of only one asset and cash. The asset is a stock that pays a dividend once per period. The dividend paid depends on the state of the market (four possible states). Each state is equally likely (i.e., each has a 25% probability of occurring in any given period).

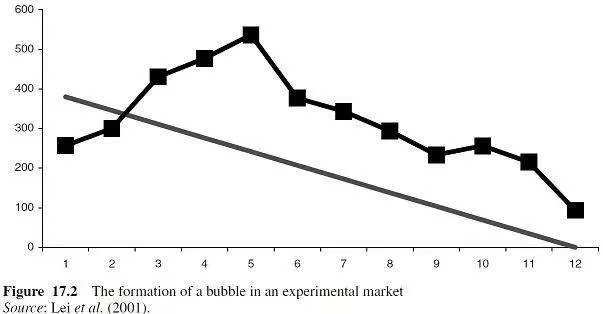

Figure 17.2 shows typical results from one such asset market. The asset was initially significantly undervalued, then surged well above its fundamental value, and finally reverted to its fundamental value in the last few periods. This is simply a classic bubble formation and collapse. What does this have to do with action bias? Figure 17.2 comes from a particularly interesting version of an experimental asset market run by Lei, Noussair, and Plott (2001).

In this special version of the game, once you purchase a stock, you are prohibited from reselling it. This eliminates the possibility of bubbles driven by the greater fool theory. In other words, because you cannot resell the stock, there is no reason to buy it at a price above its fair value—you cannot sell it to someone else for a higher profit. In fact, participants trade merely out of boredom! Consequently, investors do tend to act.

03. Buffett on the Key Pitch

The irony of this action bias lies in its direct contrast with Warren Buffett’s advice. He often likens investing to baseball, noting that aside from the absence of an umpire calling balls and strikes, the two are remarkably similar. Thus, investors can stand at home plate and simply watch pitches go by without being forced to swing. However, as Seth Klarman points out in Margin of Safety, 'Most institutional investors... feel compelled to be constantly invested. They behave as if an umpire were calling balls and strikes—mostly strikes—forcing them to swing at nearly every pitch and thereby forfeiting their choice over how often to hit.'

04. The Preference for Action Is Especially Pronounced After Poor Performance

One final aspect of this preference for action deserves particular attention—it tends to intensify following losses (i.e., after a period of underperformance in a domain where we consider ourselves competent). Zeelenberg et al. (2002) used a loss-framing paradigm to illustrate how the tendency toward inaction shifts to a bias for action.

Zeelenberg et al. asked participants to consider the following scenario: Stinland and Strathov are both soccer coaches. Stinland coaches the Blue-Blacks, while Strathov coaches E.D.O. Both teams lost their previous match by a score of 4–0. This Sunday, Stinland decides to make a change: he fields three new players. Strathov chooses not to alter his lineup.

This time, both teams lose again, this time by a score of 3–0. Which coach—Stinland or Strathov—feels more regret?

Participants received this scenario in one of three versions. Some saw the full description as above (i.e., framed by prior losses), others received only the latter part (i.e., without any prior context), and a third group read a version in which both coaches had won their previous matches but lost this week’s game.

Figure 17.3 shows the percentage of respondents who indicated which coach would feel more regret. When both teams had won the previous week, 90% of respondents believed the coach who made changes would feel more regret after losing this week’s match (a classic manifestation of omission bias). However, observe what happens when both teams lost in consecutive weeks (as described above). Now, nearly 70% of respondents believe that the coach who took no action would experience greater regret—demonstrating that the urge to act becomes exceptionally strong when dealing with losses.

05. Conclusion

Psychological and experimental evidence appears to strongly suggest that investors are inclined to act. After all, they engage in 'active' management—but perhaps they would do well to remember that waiting is also an option. As Paul Samuelson once said, investing should be boring. It shouldn’t be exciting. Investing ought to resemble watching paint dry or grass grow. If you’re seeking thrills, take $800 to Las Vegas—though getting rich isn’t easy there, at Churchill Downs, or even at your local Merrill Lynch office.

The legendary Bob Kirby once wrote about the 'Coffee Can Portfolio' (Kirby, 1984), in which investors must buy stocks and then ignore them—he described this idea as passive activism.

Kirby stated: 'I suspect this concept is unlikely to gain popularity among investment managers, because if widely adopted, it could fundamentally alter the ecology of our industry and potentially significantly reduce the quality of life for professionals in the asset management business.'

The concept of the coffee can portfolio dates back to the Old West, when people stored their valuables in a coffee can and placed it under their mattress. Coffee entails no transaction costs, management fees, or any other expenses. Success depends entirely on the wisdom and foresight used to select the assets initially placed into the coffee can…

Without these activities, what results would skilled fund managers achieve? The answer lies in another question: Are we traders or genuine investors? Most accomplished fund managers are likely investors at heart. Yet, terminals, news services, and computers that generate vast amounts of investment performance data daily drive them to behave like traders. They begin with sound research, identifying attractive companies within promising industries for the long term. Then, based on monthly news flow and rumors of every shape and size, they trade these stocks two or three times a year.

Perhaps Blaise Pascal put it best: 'All of humanity’s problems stem from man’s inability to sit quietly in a room alone.'

Editor /rice