The first Federal Reserve interest rate decision under Waller’s leadership is about to be revealed: a hold on rates is virtually certain, but the dovish tilt in the statement is expected to be dropped, inflation projections are likely to be significantly revised upward, and the dot plot may hint at initial rate hike expectations—the real uncertainty hinges entirely on every word uttered during Waller’s press conference.

The results of Kevin Warsh’s first Federal Open Market Committee (FOMC) meeting since assuming the role of Fed Chair will be announced at 02:00 a.m. There is virtually no doubt that interest rates will remain unchanged, but significant market divergence exists regarding the interpretation of signals from the policy statement wording, the economic projections dot plot, and Warsh’s press conference—making the true variables of this 'debut' far more complex than the interest rate figure itself.

At the level of the policy statement, Goldman Sachs, BofA Securities, and Morgan Stanley all expect the Fed to remove the 'dovish tilt' language that has persisted for several months, signaling that the Committee now views the likelihood of rate cuts and hikes as roughly balanced.

Meanwhile, the updated economic projections are expected to show a substantial upward revision to inflation forecasts—Goldman Sachs projects the median core PCE forecast for 2026 will be revised up from 2.7% in March to approximately 3.3%. The median dot in the interest rate dot plot is likely to shift from the previous 'one rate cut this year' to 'no change this year,' with a few dots reflecting expectations of rate hikes. Progress in the U.S.-Iran agreement has driven oil prices sharply lower from recent highs, somewhat alleviating external inflationary pressures, but persistent core inflation continues to constrain policy space.

Meanwhile, the updated economic projections are expected to show a substantial upward revision to inflation forecasts—Goldman Sachs projects the median core PCE forecast for 2026 will be revised up from 2.7% in March to approximately 3.3%. The median dot in the interest rate dot plot is likely to shift from the previous 'one rate cut this year' to 'no change this year,' with a few dots reflecting expectations of rate hikes. Progress in the U.S.-Iran agreement has driven oil prices sharply lower from recent highs, somewhat alleviating external inflationary pressures, but persistent core inflation continues to constrain policy space.

All eyes will be on Warsh’s press conference. BofA Securities notes that if he characterizes recent inflation as a one-off supply-side shock and emphasizes the disinflationary outlook driven by AI, long-end yields could face selling pressure; if he explicitly endorses a path toward rate hikes, the two-year SOFR could rise by about 15 basis points, providing directional support to the dollar. Goldman Sachs frames this press conference as a pivotal juncture where 'identical rate decisions could lead to divergent market outcomes,' with positions already hedged across asset classes including rates, FX, equities, and gold.

Trump previously appointed Warsh to lead the Fed in anticipation of rate cuts, but the Committee Warsh inherited has quietly shifted sharply toward a hawkish stance. With elevated inflation and a resilient labor market, several officials have publicly stated that rate hikes should remain on the table. His debut will unfold amid conflicting data, fragmented market expectations, and his own deliberate policy ambiguity.

Interest Rate Decision: On Hold—but Not Without Consequences

The meeting is almost universally expected to maintain the target federal funds rate in the 3.50%–3.75% range.

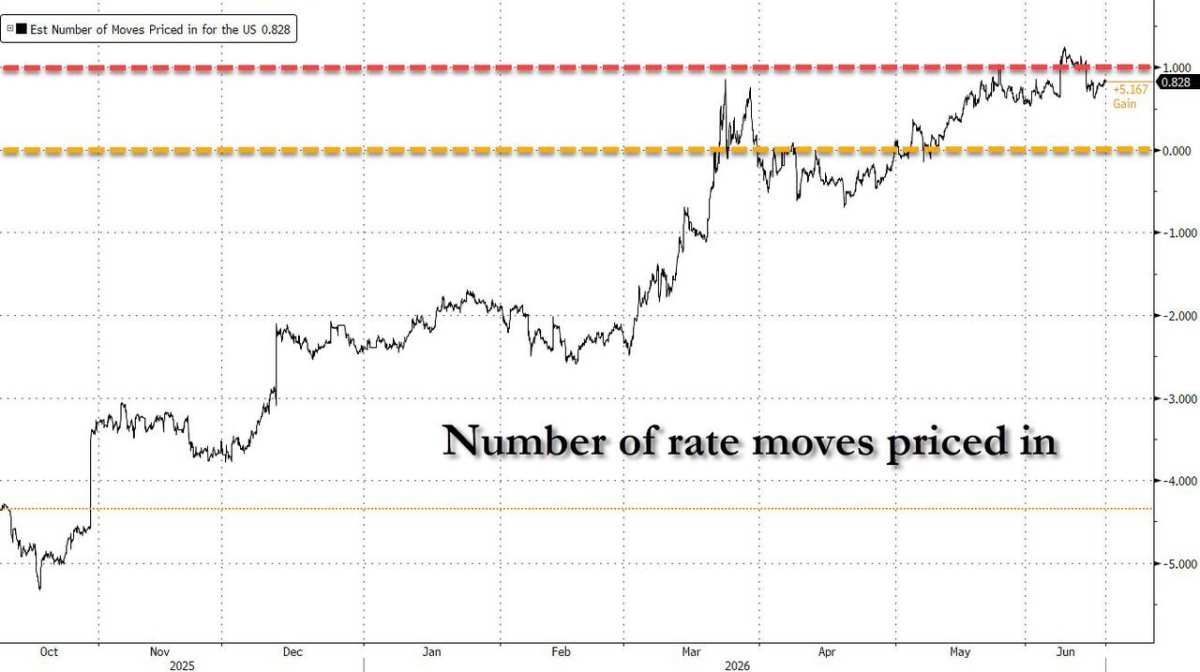

According to a Reuters survey of 102 economists, 72 respondents expect rates to remain unchanged through the end of 2026. In money markets, the U.S.-Iran conflict initially pushed oil prices higher, leading markets to fully price in a rate hike this year; however, as negotiations on a U.S.-Iran deal progressed and oil prices retreated sharply from their peaks, rate hike expectations have moderated. Markets currently price in approximately 18 basis points of cumulative tightening by year-end, implying a roughly 72% probability of a single 25-basis-point hike.

The vote outcome is expected to be unanimous. BofA Securities believes hawkish members will be satisfied with the removal of the dovish tilt, and the sole previous dissenter in favor of a rate cut—former Board member Stephen Miran—has since departed, succeeded by Warsh. Although Warsh is generally seen as dovish, BofA Securities explicitly states he will not advocate for a rate cut at his first meeting.

Statement Wording: The Dovish Tilt Exits, Policy Balance Returns to Neutral

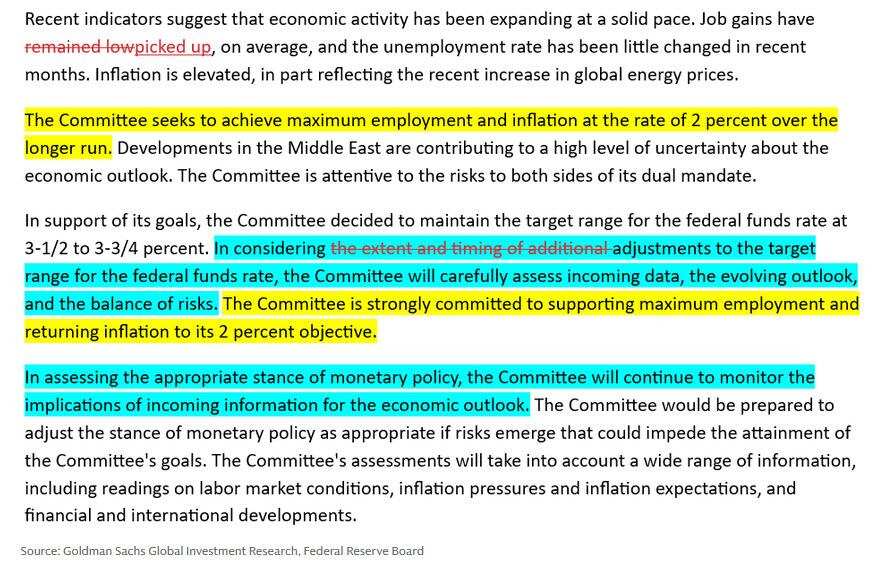

The adjustment in the statement’s wording represents the most certain change from this meeting and serves as the clearest signal of the Committee’s shifting stance. The current phrasing—'in considering the extent and timing of any further adjustments to the target range for the federal funds rate...'—has long been interpreted as implying that the next move is more likely to be a rate cut.

At the April meeting, voting members Kashkari, Hammack, and Logan already dissented on removing the accommodative bias.

Subsequently, Governor Christopher Waller’s remarks became a critical turning point. Previously viewed as a leading dove on the committee, Waller stated publicly in May: 'Based on recent data, I support removing the accommodative bias to clarify that rate cuts are no more likely than rate hikes.' Goldman Sachs believes Waller’s statement reflects a collective shift within the dovish camp.

There is some divergence among institutions regarding the specific approach to revising the wording.

Bank of America Merrill Lynch expects the Committee may either drop the word 'additional,' or go further by removing 'extent and timing' altogether and replacing it with the more neutral phrase 'any adjustments.' Waller might even push to delete the entire forward guidance paragraph—a stance consistent with his longstanding criticism of forward guidance. Goldman Sachs also anticipates the removal of this language and notes that the statement has room for further shortening and simplification due to overlapping content across certain paragraphs.

The description of the labor market is expected to be upgraded concurrently. Bank of America Merrill Lynch forecasts that the current wording—'job gains remain subdued'—will be revised to reflect several consecutive months of strong nonfarm payroll reports, potentially changing to something like 'job growth has picked up, and the unemployment rate has remained broadly stable in recent months.'

Dot Plot: Inflation Forecasts Sharply Revised Upward; Rate Hike Expectations Emerge

This updated Summary of Economic Projections (SEP) is expected to reflect the most pronounced hawkish pivot of the current monetary policy cycle.

At the macroeconomic forecast level, Goldman Sachs expects the median PCE inflation projection for 2026 to be sharply revised upward from 2.7% in March to approximately 3.9%, and core PCE from 2.7% to about 3.3%, primarily reflecting the combined impact of energy price shocks stemming from the Iran conflict and rising memory prices linked to AI. GDP growth forecasts are expected to be downgraded from 2.4% to around 2.2%, while the unemployment rate forecast is projected to be slightly revised downward to 4.3%.

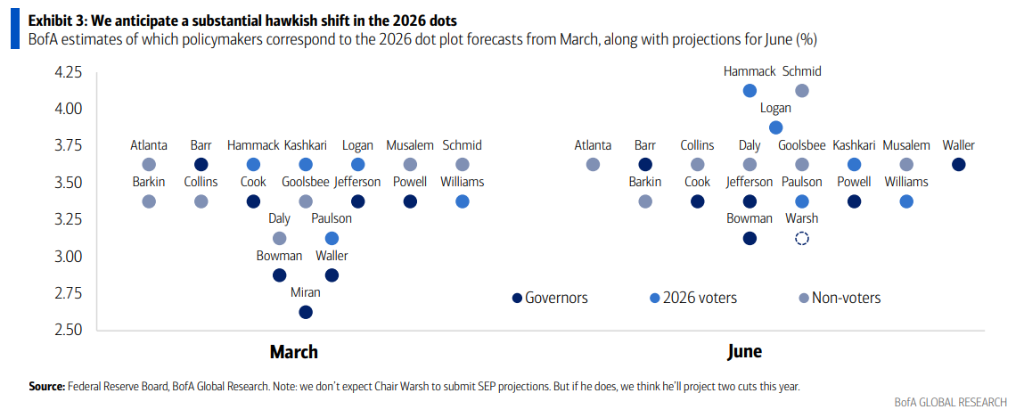

Regarding the interest rate dot plot, Goldman Sachs anticipates the median 2026 rate will remain at 3.625%, but roughly four to five dots will cluster around 3.875%, indicating that a minority of officials have already incorporated a rate hike into their baseline outlook for this year. BofA Securities notes its base case involves Hammack, Logan, and Schmid submitting hike projections, with Kashkari, Musalem, and others potentially following suit. Goldman Sachs strategist Rich Chambers stated, 'With year-end core PCE inflation projected at around 3.4%, market pricing is likely to stay near 3.875%, and the hike premium will persist even if a peace agreement is reached.'

A key variable is whether Waller himself participates in the SEP. Both BofA Securities and Deutsche Bank expect he will not submit a forecast, citing his short tenure as one reason, but more fundamentally due to his systemic skepticism toward forward guidance as a policy tool. If Waller abstains from the dot plot, the median would implicitly shift in a hawkish direction, as his potentially low-rate forecast would be excluded from the calculation.

Goldman Sachs' baseline forecast indicates that the Federal Reserve's final two rate cuts will occur in June and December 2027, respectively. However, Goldman Sachs also notes that a flat path of 'rates on hold for an extended period' has become an alternative scenario with a probability close to that of the baseline case. The overall probability-weighted interest rate forecast remains more dovish than market pricing, primarily reflecting Goldman Sachs’ assessment of a low likelihood of further rate hikes.

Press Conference: Walsh’s Policy Style Makes Its Debut

Walsh’s first post-meeting press conference represents the key market risk event of this meeting. How he balances the hawkish stance of the committee with his own dovish inclinations will provide markets with their first direct insight into his policy framework.

From his public statements, Walsh repeatedly emphasized during his Senate confirmation hearing his opposition to excessive forward guidance and advocated for balance sheet reduction and a return to interest rates as the primary policy tool. He favors using the Dallas Fed trimmed-mean inflation measure (currently around 2.35%) as a reference for underlying inflation pressures, arguing that it better captures persistent inflationary trends than core PCE, and has questioned the accuracy of the current inflation measurement system. He has also appointed conservative policy analysts Paul Winfree and Daniel Hall as advisors.

BofA Securities’ baseline expectation is that Walsh will deliver a moderately dovish message at the press conference: characterizing the Iran conflict as a one-off energy shock that does not materially alter the inflation fundamentals; highlighting the disinflationary potential of AI-driven productivity gains; and reiterating that monetary policy should remain forward-looking and not be swayed by month-to-month fluctuations in energy prices. However, BofA Securities explicitly states that recent data are still insufficient to justify near-term rate cuts, and Walsh will emphasize patience while preserving room for easing later in the year.

Goldman Sachs’ trading desk expects Walsh to acknowledge that inflation remains above target and the labor market is solidifying, but he will refrain from providing clear direction on the future tightening path. Instead, he will express a 'neutral stance, ready to respond in either direction'—a formulation that would help him build consensus within the committee and avoid unnecessary market volatility at his inaugural meeting.

BofA Securities also notes that Walsh may announce a change to hold post-meeting press conferences quarterly rather than after every meeting—a shift that would itself signal a significant reform in communication practices. Goldman Sachs, meanwhile, does not expect Walsh to address topics such as reducing the size of the FOMC, balance sheet runoff, or formally eliminating forward guidance at this meeting.

Economic Context: Persistent Inflation Amid Resilient Labor Market

Ahead of this meeting, economic data have shown a pattern of 'relatively strong employment and sticky inflation,' setting the tone for the committee’s policy deliberations.

On the employment front, the May nonfarm payrolls report marked the third consecutive month of robust job growth, with a three-month average of approximately 188,000. Goldman Sachs projects that even if economic growth remains below potential and higher oil prices exert some drag on consumption, the unemployment rate will only rise modestly to 4.4%, keeping the labor market broadly on a solid trajectory.

On inflation, the energy shock has pushed up headline inflation. Goldman Sachs expects full-year PCE inflation to exceed 4%, with core PCE remaining above 3% for the year. As the U.S.-Iran agreement progresses and oil prices retreat, some economists believe May could mark the peak month for headline inflation, contingent on the smooth resumption of navigation through the Strait of Hormuz. Goldman Sachs notes that the combined impact of tariffs, energy prices, and AI-related memory price increases on core PCE has passed its most extreme phase, and month-over-month core inflation is likely to gradually decline over the remainder of the year; however, inflation will remain persistently above the Federal Reserve’s 2% target in the foreseeable future.

Goldman Sachs points out that strong labor market data has allowed the Committee to focus its attention on whether inflationary pressures have deteriorated to a degree that warrants further rate hikes. The anchoring of core inflation expectations and the breadth of elevated inflation readings will be key dimensions guiding the Committee’s future policy decisions.

Market Implications: Divergent Responses Across Rates, FX, and Equities

Each asset class has already established its own framework for responding to this FOMC meeting.

In rates markets, Bank of America Securities believes that the baseline scenario—characterized by Waller’s neutral-to-dovish tone—is interpreted as relatively hawkish under a data-dependent stance. They recommend investors go long on 2-year U.S. Treasury yields (currently around 4.07%, with a target of 4.25%) and maintain a flattening trade between the 2- and 10-year segments of the curve. Goldman Sachs strategist Josh Schiffrin noted that there is limited room for front-end rates to fall significantly, and a clear weakening in the labor market would be required for market expectations to shift from rate hikes to cuts.

In the foreign exchange market, Bank of America Securities noted that the hawkish adjustments in the statement and the Summary of Economic Projections (SEP) have largely been priced in. The biggest upside risk for the U.S. dollar stems from a more hawkish-than-expected press conference by Waller; should he downplay recent inflation pressures citing the U.S.-Iran deal, the dollar could face temporary downside pressure. Goldman Sachsoptions strategyforeign exchange strategist Harriet Bull pointed out that the current meeting gap for G10 currenciesoptions pricingis approximately 45 to 55 basis points, sitting in the relatively high end of the range seen over the past year. However, with improved risk sentiment, baseline volatility has declined somewhat, making long positions in option volatility around the meeting period still attractive from a risk-reward perspective.

In equity markets, Goldman Sachs derivatives strategist Cindy Lu noted that event risk is two-sided: if Waller adopts a dovish or neutral stance, it could extend the recent equity rally; however, an explicitly hawkish tone would pose a significant threat to risk asset positions. Given the VIX expiration and front-endimplied volatility,volatility near recent lows, holding gamma-long options straddling the event offers relatively compelling value.

In gold markets, Goldman Sachs data shows that CTAs, ETFs, and futures markets have all turned net short on gold, with GLD call skew dropping to a decade-low and put skew rising to a historical high. Goldman Sachs believes that if the Fed delivers a neutral or dovish message and the Iran deal materializes smoothly, gold could see a short-covering-driven rebound. They recommend positioning for upside risk through risk reversal strategies.

The Iran Deal: Waller’s ‘Cushion’ and the Biggest Tail Risk

Easing U.S.-Iran tensions represent the most critical macro backdrop variable for this meeting.

At the height of the conflict, surging energy prices briefly led markets to fully price in a rate hike within the year; as a framework for peace talks has taken shape, Brent crude has retreated sharply from its peak to around $82—its lowest level in over three months. Market pricing for a rate hike this year has now narrowed to approximately 18 basis points, with the formal signing of the agreement expected to be completed this Friday.

Goldman Sachs noted that historically, the Federal Reserve’s monetary policy response to oil price shocks has typically been muted. The correlation between high oil prices and hawkish rhetoric is weak, and current wage inflation remains moderate, with no signs of overheating in the labor market—fundamentally undermining the case for aggressive rate hikes. Goldman Sachs expects that the extreme upward pressure on monthly inflation from oil prices and AI-related memory chip costs has largely passed and will gradually fade over the remainder of the year.

Alan Stewart, Head of Global Emerging Markets and G10 Spot at Goldman Sachs,foreign exchange tradingnoted that this provides ample justification for Waller to characterize recent inflationary shocks as transitory supply-side events, thereby offering both political and logical support for a 'wait-and-see' stance. However, he also warned that if the agreement process encounters setbacks or the resumption of transit through the Strait of Hormuz falls short of expectations, 'the previously cooled rate-hike expectations could rebound swiftly.'

Under Goldman Sachs’ baseline forecast, the Federal Reserve will hold rates steady throughout 2026, with its final two rate cuts delayed until June and December 2027. Goldman Sachs’ probability-weighted Fed path remains significantly more dovish than current market pricing, primarily due to its skepticism regarding any rate hike scenario. The firm’s report stated bluntly: 'Trump appointed Waller to cut rates, not to raise them—and Waller knows it himself.' This does not mean he will act rashly at his first meeting, but it reflects his similarly cautious stance toward rate hikes. Waller’s debut is most likely to be 'bomb-free'—yet a misstep in wording could ignite the fuse at any moment.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/joryn