Bank of America believes the computing power race is evolving into a battle for electricity, with China's data centers poised for a surge in power consumption. Traditional materials and power equipment—including high-end copper foil, low-Dk glass fiber, transformers, and gas turbines—are fully integrating into the AI value chain. Meanwhile, liquid cooling adoption is expected to soar from 30% to 70%, creating substantial structural investment opportunities.

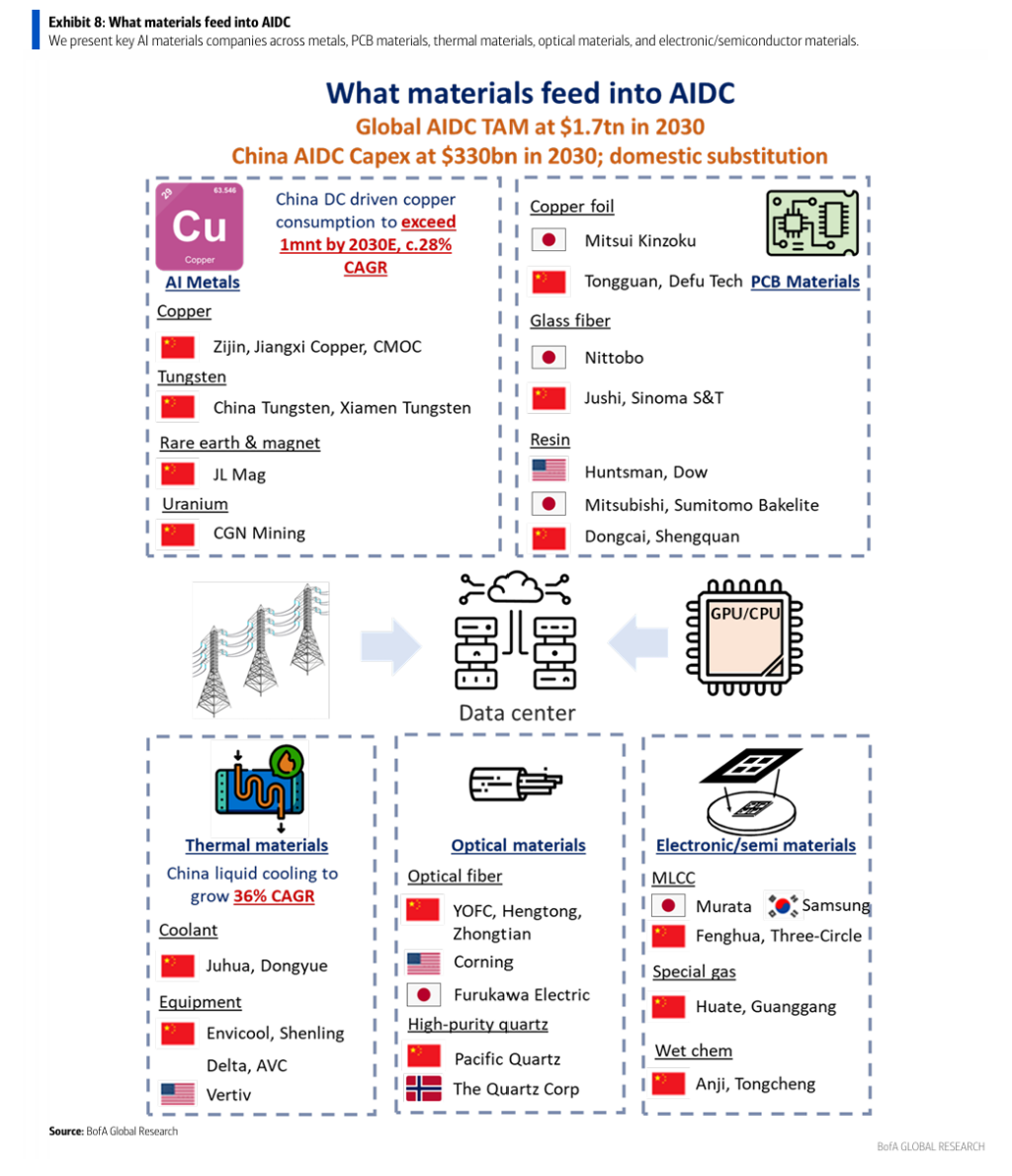

In its latest AI infrastructure research report, Bank of America Securities significantly raised its forecast for China's AI data center (AIDC) capital expenditure to USD 327 billion by 2030 and systematically outlined structural investment opportunities for traditional sectors—including copper, PCB materials, optical fiber, and transformers—to integrate into the AI value chain. Related stocks received a series of buy ratings.

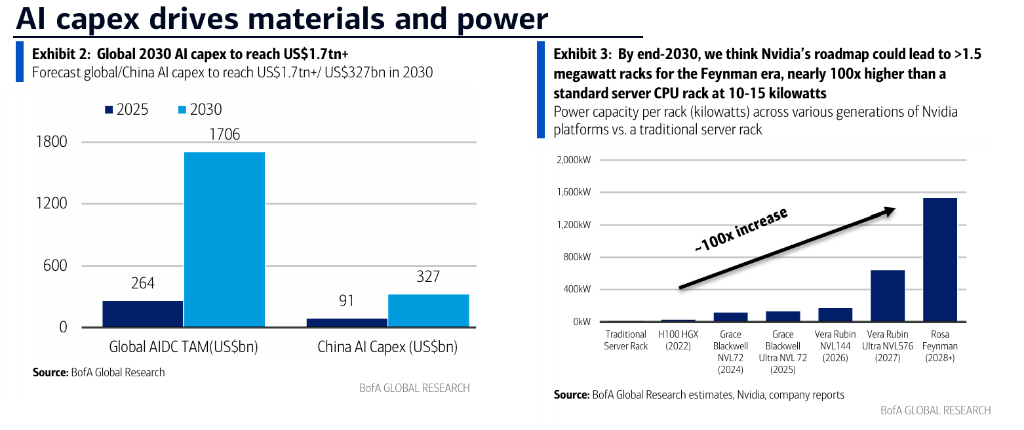

According to reports, China’s AIDC capital expenditure over the next five years could reach approximately RMB 2 trillion. Per Wind Trading Desk sources, Bank of America forecasts that China’s AI-related capital expenditure will grow from approximately USD 140 billion in 2026 to USD 327 billion by 2030, representing a compound annual growth rate (CAGR) of 24%, accounting for roughly 20% of global AI capital expenditure by then. Meanwhile, Bank of America’s global team simultaneously revised upward its 2030 global AI capital expenditure forecast to over USD 1.7 trillion, a substantial increase from USD 260 billion in 2025.

The report centers on two main themes. The first is AI materials, covering five categories: copper, PCB materials (copper foil and glass fiber), optical fiber, magnetic materials/tungsten/uranium. Several high-end sub-segments within these categories are facing structural supply shortages, providing strong upward price momentum. The second theme is AI power infrastructure, encompassing five opportunity areas: transformers, gas turbines, diesel engines, energy storage systems, and power supplies. China is well positioned to benefit significantly from the global AIDC construction wave and expand its export market share, thanks to advantages in electricity costs, grid infrastructure, and a robust equipment manufacturing supply chain.

The report centers on two main themes. The first is AI materials, covering five categories: copper, PCB materials (copper foil and glass fiber), optical fiber, magnetic materials/tungsten/uranium. Several high-end sub-segments within these categories are facing structural supply shortages, providing strong upward price momentum. The second theme is AI power infrastructure, encompassing five opportunity areas: transformers, gas turbines, diesel engines, energy storage systems, and power supplies. China is well positioned to benefit significantly from the global AIDC construction wave and expand its export market share, thanks to advantages in electricity costs, grid infrastructure, and a robust equipment manufacturing supply chain.

The core rationale behind these conclusions is that the AI computing race is increasingly becoming a competition over power infrastructure. Global data center installed capacity is projected to expand from approximately 100 GW today to nearly 300 GW by 2030. Rack power density is expected to surge from the traditional server range of 10–15 kW to 100–120 kW under current NVIDIA platform roadmaps, with potential to exceed 1 MW in next-generation systems. This shift is driving upstream material and power equipment demand into a structurally ascending trajectory.

Power Demand: China’s data centers will consume 318 terawatt-hours (TWh) of electricity by 2030

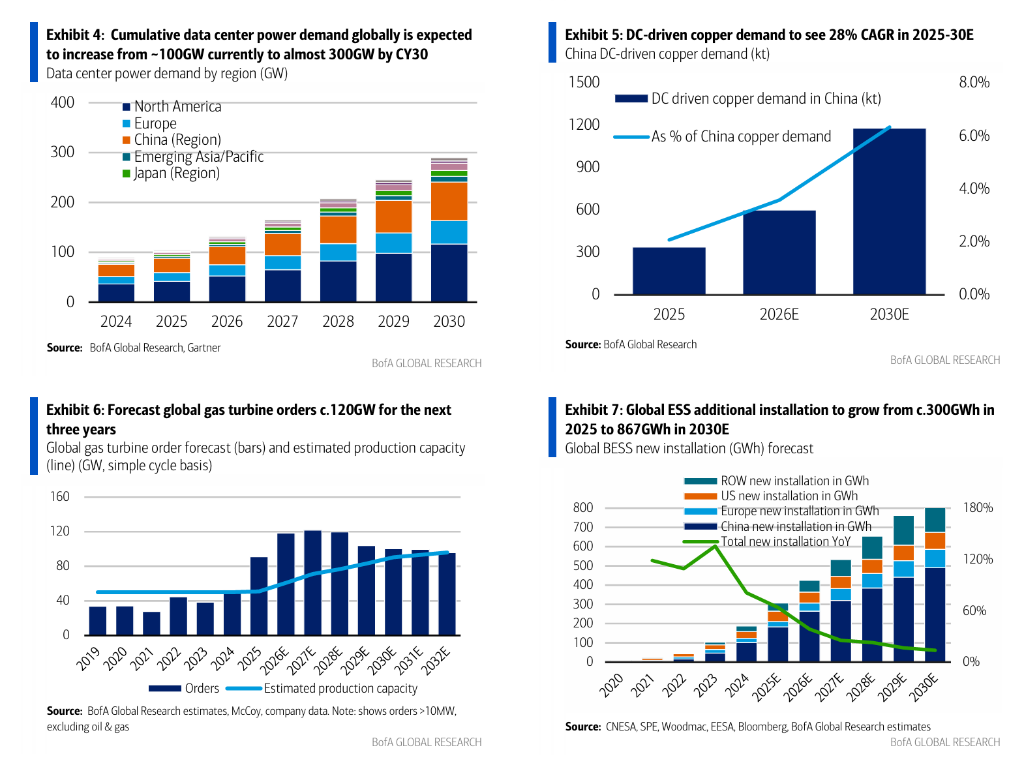

According to data from the International Energy Agency (IEA), global data center electricity consumption in 2025 will approach 500 TWh, accounting for approximately 1.6% of total global electricity use. Bank of America estimates this figure will grow at a compound annual rate of 22%, reaching 1,208 TWh by 2030—about 3.7% of global electricity consumption.

In China, data center installed capacity is projected to rise from 29 GW in 2025 to 77 GW by 2030, with corresponding electricity consumption increasing from 121 TWh to 318 TWh—accounting for roughly 2.5% of national electricity use. Bank of America also notes that due to chip-related constraints prompting some internet companies to relocate computing capacity to Southeast Asia, actual domestic data center power consumption in China may lag behind the true growth rate of AI demand.

Three key factors are driving the sharp increase in power demand: rapid growth in AIDC workloads; higher per-chip power consumption as GPUs replace CPUs; and significant system-level power expansion required to support rack power densities rising from 10–15 kW to 100–120 kW or higher.

AI Materials: Structural Supply Tightness Across Five Key Categories

Regarding copper, Bank of America forecasts that China’s data center-related copper demand will grow from 341 kilotonnes (kt) in 2025 to 1,190 kt by 2030—a CAGR of 28%—raising its share of total Chinese copper demand from 2.1% to 6.4%. This incremental demand will primarily stem from data center operations (650 kt), grid expansion (504 kt), and power plant construction (36 kt). Addressing market concerns about 'optical fiber replacing copper,' Bank of America argues that copper remains irreplaceable in power transmission, short-distance interconnects, and intra-server connections. Coupled with an anticipated global copper supply deficit of 491–754 kt between 2026 and 2027, the fundamental support for copper prices remains robust.

In PCB materials, structural overcapacity persists in low-end copper foil. However, AI servers are driving an increase in PCB layer counts and higher specifications for high-frequency signal transmission, sharply expanding demand for high-end copper foil. High barriers to capacity conversion, equipment bottlenecks, and customer certification cycles typically exceeding one year make it difficult to close the supply-demand gap in the near term, supporting sustained pricing and profitability for high-end products.

Supply of high-end electronic glass fiber (specialty yarns with low Dk and low CTE) has historically been dominated by a few Japanese manufacturers such as Nittobo (3110 JP). However, Chinese producers have gradually achieved breakthroughs after years of R&D. Currently, there are five qualified domestic suppliers, with Taishan Fiberglass, a subsidiary of Sinoma Science & Technology, leading the market. Bank of America has assigned a Buy rating to Sinoma Science & Technology, forecasting its specialty fiberglass capacity to expand from the current 24 million meters to 94 million meters by 2027.

Fiber optic demand is accelerating its shift from traditional telecom toward AIDC applications. While overall capacity remains sufficient, a structural supply bottleneck exists in preforms—the key upstream raw material for high-end fiber optics—due to their long capacity expansion cycle and high technical barriers, thereby underpinning fiber optic prices. Bank of America has assigned a Buy rating to Jiangsu Zhongtian Technology, expecting its compound annual EPS growth rate from 2026 to 2027 to reach approximately 75%.

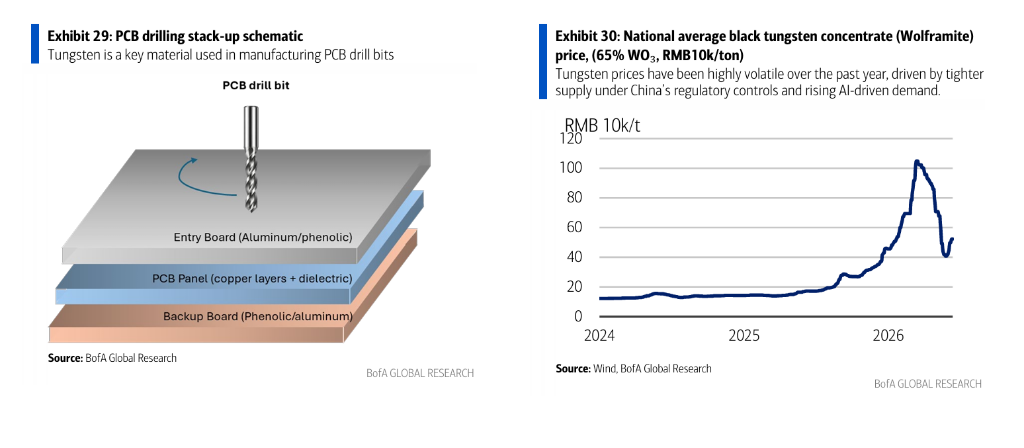

In magnetic materials, tungsten, and uranium: high-performance neodymium-iron-boron (NdFeB) permanent magnets benefit from dual drivers—liquid cooling systems in AIDC infrastructure and humanoid robotics—maintaining structurally tight supply conditions. Tungsten has entered the AI value chain due to growing demand for high-density PCB drilling, with China’s resource controls keeping supply inelastic. Uranium is viewed as a core strategic resource for scalable, zero-carbon, and stable baseload power in the AI computing era. Bank of America’s global commodities team forecasts uranium prices to rise by 47% and 29% year-over-year in 2026 and 2027, respectively, driven by a structural supply deficit of 2%–7% annually and demand growing at a compound annual rate of approximately 4%.

AI Power Supply: China Holds Unique Competitive Advantages

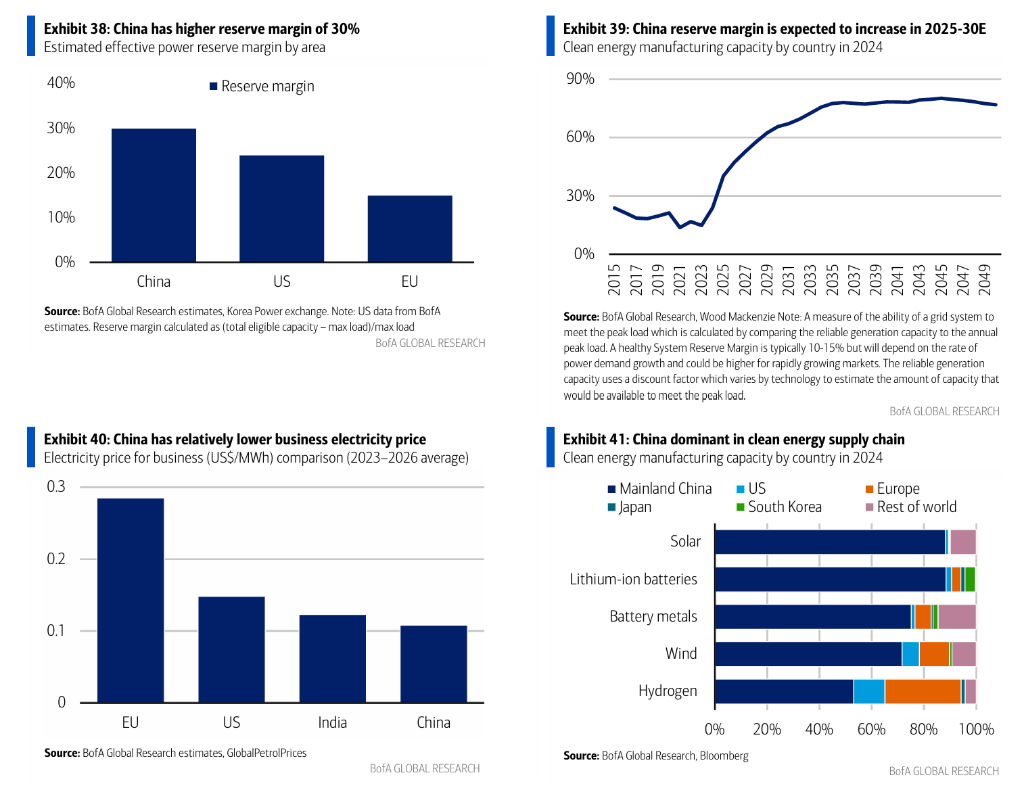

Bank of America emphasizes that China possesses multiple structural advantages in AI power supply: commercial electricity tariffs are 30%–60% lower than those in the U.S. and EU; available reserve capacity margin stands at approximately 30%, higher than the U.S.’s sub-25% and the EU’s ~15%; transmission and distribution infrastructure has an average age of less than 20 years (compared to over 40 years in the U.S. and Europe), ensuring greater grid stability; and China operates a comprehensive network of 46 ultra-high-voltage transmission corridors alongside a robust power equipment manufacturing ecosystem. Additionally, China has announced plans to expand nuclear power installed capacity from 62 GW by end-2025 to approximately 110 GW by 2030 under its 15th Five-Year Plan.

Opportunity 1: Transformers. Bank of America forecasts China’s transformer exports to grow by 30% year-over-year in 2026, with domestic grid investment rising by 12% to approximately RMB 715 billion. The global transformer shortage is expected to persist through at least 2029, with lead times for high-voltage transformers stretching up to three years. China is effectively filling overseas capacity gaps thanks to its robust supply chain.

Opportunity 2: Gas turbines. Bank of America’s Global Industrials team projects annual global gas turbine orders of approximately 120 GW from 2026 to 2028. Current new order lead times extend to 3–6 years, creating a window for Chinese manufacturers to enter the market on the basis of competitive pricing and shorter delivery timelines (as short as 13 months). Dongfang Electric is the only Chinese company capable of exporting medium- and large-scale gas turbines. Its G50 50MW units have already secured sales of 10 units to a Canadian data center client and have been exported to Kazakhstan and Indonesia. Management plans to scale export capacity to 23 units by end-2027 and 45 units by end-2029.

Opportunity 3: Diesel engines. Chinese manufacturers of large-bore diesel engines have obtained UL and EPA certifications in the U.S., becoming the first to enter the North American AIDC backup power market. Bank of America forecasts demand for AIDC backup diesel engines in China to reach 8,500 units in 2026, with supply tightness expected to ease in 2027 as capacity expands.

Opportunity 4: Energy storage systems. Bank of America forecasts the global BESS (Battery Energy Storage System) market to grow at a compound annual rate of approximately 23% from 2025 to 2030, with AIDC-related BESS growing at about 27%. By 2030, annual new AIDC BESS installations globally are projected to reach 70 GWh, accounting for roughly 8% of total global new BESS installations.

Opportunity Five: Power Supply Systems. Bank of America forecasts that China’s AIDC power supply systems market (comprising UPS, HVDC, and SST) will grow at a compound annual growth rate (CAGR) of approximately 25% from 2025 to 2030. Nvidia is actively driving its supply chain toward an 800V DC high-voltage direct current (HVDC) architecture along its hardware roadmap to address continuously rising rack power densities. The average selling price (ASP) of high-capacity power supply systems is significantly higher than that of traditional units, and the combination of high R&D barriers and customization requirements creates a strong competitive moat.

Liquid Cooling: Penetration Rate to Jump from 30% to 70%

Liquid cooling is the fastest-growing segment within China’s data center cooling market. As rack power densities continue to exceed the practical limits of air cooling (approximately 40 kW per rack), coupled with increasingly stringent domestic energy efficiency regulations, the adoption of liquid cooling is accelerating. Liquid cooling offers thermal conductivity 20 to 50 times higher than air cooling, enabling power usage effectiveness (PUE) to drop to approximately 1.1.

Bank of America projects that the penetration rate of liquid cooling in China’s data centers will rise from 30% in 2025 to 70% in 2030, with demand expanding from 1.4 GW to 9.5 GW—a compound annual growth rate (CAGR) of 47%. The overall data center cooling market in China is expected to grow from 2025 to reach RMB 70 billion by 2030, representing a CAGR of 36%. Currently, cold plate liquid cooling accounts for over 90% of the market share, while immersion liquid cooling is projected to increase its share from approximately 5% in 2025 to around 17% in 2030, reaching a market size of RMB 16 billion.

Editor/Deng