As the Iran war risk premium fades, traders have largely resumed flocking to pre-conflict trades dominated by short-term U.S. Treasuries, Asian currencies, and the AI computing supply chain. $NVIDIA (NVDA.US)$ 、 $Advanced Micro Devices (AMD.US)$ 、 $Arm Holdings (ARM.US)$ 、 $SK Hynix (000660.KR)$and$Micron Technology (MU.US)$ The AI computing supply chain has emerged as the strongest investment theme in the pre-conflict trading playbook.

Zhitong Finance APP learned that the latest signs indicating the United States and Iran are nearing the end of a new round of Middle East conflict have prompted equity traders this week to unwind hedging positions and collectively turn bullish—just ahead of new Federal Reserve Chair Kevin Warsh’s scheduled remarks on Wednesday (early Thursday Beijing time), in which he is expected to reveal part of his monetary policy stance. Options market data compiled by institutional sources show that, as of Monday, the cost of insuring against a 10% decline in the S&P 500 over the next month has dropped sharply to its lowest level in more than a year, relative to contracts designed to profit from a comparable upside move. Meanwhile, recent research reports from Wall Street titans including Goldman Sachs, Morgan Stanley, and JPMorgan all suggest that the global equity bull market led by the AI computing infrastructure supply chain is far from over.

In other words, as the geopolitical risk premium associated with potential conflict with Iran recedes, traders are once again flocking en masse to the same pre-conflict trade themes: short-term U.S. Treasuries, Asian currencies, and the AI computing infrastructure supply chain—the latter having emerged as the strongest investment narrative prior to the conflict. Within equities, stocks directly tied to AI computing infrastructure—led by NVIDIA, SK Hynix, and AMD, forming what some call the 'AI Computing Superteam'—tend to be the most sensitive, first to move, and exhibit the largest upward momentum during broader market and tech-sector rebounds. The core logic underpinning this vanguard rally is exceptionally 'hardcore': these companies are directly linked to record-breaking, trillion-dollar-scale AI capital expenditures by major technology firms, rather than merely speculative narratives.

The strategy team led by David Kelly, Chief Global Strategist at JPMorgan Asset Management, is urging investors to maintain exposure to equities and other relatively higher-risk assets through the second half of 2026, arguing that an unprecedented boom in AI-related investment and resilient consumer spending should continue to support economic and equity market expansion—even amid persistent inflation and a Fed holding steady in a wait-and-see monetary policy stance.

The strategy team led by David Kelly, Chief Global Strategist at JPMorgan Asset Management, is urging investors to maintain exposure to equities and other relatively higher-risk assets through the second half of 2026, arguing that an unprecedented boom in AI-related investment and resilient consumer spending should continue to support economic and equity market expansion—even amid persistent inflation and a Fed holding steady in a wait-and-see monetary policy stance.

From Goldman Sachs’ perspective, the global bull market centered on the AI computing supply chain is far from complete. The market’s dominant theme has evolved from the long-standing post-2008 paradigm of 'code-driven, asset-light software valuation expansion' to a 'repricing of physical AI computing infrastructure assets.' Goldman Sachs’ latest assessment implies that the next wave of excess alpha returns will no longer be confined solely to leading names in AI GPUs and AI ASICs, but will systematically spread across the entire stack of 'AI factory' infrastructure—including high-performance CPUs for data centers, DRAM/NAND/HBM memory, AI PCBs, liquid cooling systems, data center optical interconnects, ABF substrates/glass substrates, MLCCs, electronic fabrics, and broad-based wafer foundry services. On Wednesday, NVIDIA CEO Jensen Huang further stated that AI infrastructure could revitalize U.S. manufacturing and potentially usher in a new era of industrial and manufacturing growth in America.

Nevertheless, some traders remain highly anxious ahead of Warsh’s first FOMC monetary policy meeting as Fed Chair, believing that certain cautious investors have not actually reflected their prudence in their options positioning. This unusually relaxed posture could leave markets vulnerable to a sharp short-term selloff.

These cautious traders argue that the market’s consensus shift toward bullishness has left equities exposed to any negative surprise, as investors are betting that little volatility will occur while they await Warsh’s first press conference following the Fed’s monetary policy decision—scheduled for 2:30 p.m. Washington time. If this bullish assumption proves incorrect, a resurgence in VIX volatility could abruptly end the market’s increasingly fervent optimism, currently buoyed by hopes of a U.S.-Iran ceasefire.

A delicate moment after risk aversion fades: With hedging protection vanishing, the S&P 500 stands at the crossroads of 'AI-driven prosperity' and 'inflationary hawkishness.'

“Fear has been taken out of the market,” said John Salama, a proprietary equity derivatives trader at Maverick Trading. “This could signal significant complacency, exposing traders to substantial downside risk—or it could mark the beginning of a low-volatility period over the coming weeks.”

Investors and Wall Street strategists broadly expect the Federal Reserve to hold interest rates steady when it concludes its two-day FOMC monetary policy meeting on Wednesday Eastern Time. An anticipated U.S.-Iran peace framework agreement, expected to be formally signed in Switzerland, has alleviated concerns about persistently high oil prices and their inflationary impact, helping push the S&P 500 to within just 1.3% of its all-time high.

Yet this scenario is not without risks for Wall Street strategists, as Warsh faces a delicate balancing act: reconciling President Donald Trump—who nominated him as Fed Chair and is calling for rate cuts to stimulate growth—with fresh data showing inflation accelerated in May to its fastest pace in three years.

Of course, traders are pricing in a certain degree of risk. According to data compiled by Piper Sandler, a well-known Wall Street investment firm, the options market is pricing in a move of 0.9% to 1.2% in either direction for the S&P 500 on Wednesday—significantly higher than the average fluctuation of approximately 0.6% observed on Federal Reserve monetary policy decision days over the past 12 months.

However, few appear concerned enough to hedge against downside risk. With the U.S. tech earnings season still a month away and geopolitical risks easing, investors see little catalyst to drive equities significantly in either direction.

In the options market, waning anxiety has pushed the measure of one-week implied price volatility below the expected volatility one month out. The relationship between these two metrics inverted in early June, reflecting greater near-term market anxiety compared with concerns about the future.

“Investors believe that the anticipated peace agreement between the U.S. and Iran—which is expected to lower oil prices and ease inflationary pressures—has reduced the pressure on Walsh to raise rates,” said Max Wasserman, founder and senior portfolio manager at Miramar Capital. “But we still haven’t resolved all the issues, and we don’t yet know every detail of the agreement.”

Fed officials have stated that robust job growth and rising price pressures linked to the conflict with Iran have left policymakers with little room to cut rates. Traders continue to speculate that the Fed’s next move could be a rate hike rather than a cut.

This puts the Fed’s updated economic projections front and center, with any shift in the quarterly “dot plot”—which shows policymakers’ rate expectations—drawing intense scrutiny. Walsh has repeatedly advocated reducing the frequency of dot plot releases or even eliminating them altogether. Investors are now speculating whether the Fed under Walsh might streamline its quarterly Summary of Economic Projections, and if so, whether increased opacity in the Fed’s communication and transparency toward financial markets could trigger significant valuation collapses.

However, any sign of concern from Walsh about persistent inflation or setbacks in disinflation progress could trigger a correction in the AI-driven super bull market—or even spark sharp global equity swings—following the Fed meeting. If the dot plot shows a collectively more hawkish stance among policymakers, it could prompt some degree of selling. For instance, PGIM, a U.S. asset management firm, is betting that the Fed will hike rates three times this year to cool the economy before reversing those hikes in 2027.

After months of calm, price volatility around economic data releases has risen again. Data compiled by Rocky Fishman, strategist and founder of Asym Research, shows that over the past three months, the S&P 500’s average realized volatility has been 19 on days when key reports—including the Consumer Price Index, monthly government employment figures, and Fed rate decisions—were released, compared with a reading of 15 on other trading days.

For the S&P 500, which has added over $10 trillion in market capitalization since late March, this could be a dangerous setup. “If Walsh says anything unexpected regarding U.S.-China trade, tariffs, or inflation, it would spook the market,” Salama noted.

AI investment boom reignites stock bull market—JPMorgan heavily bets on sustained surge in AI computing infrastructure investment and expanding wealth effect

JPMorgan’s global asset management division is urging investors to maintain exposure to equities and other higher-risk assets through the second half of 2026, arguing that the AI investment boom and resilient consumer spending should sustain economic and equity market expansion amid persistent inflation and a Federal Reserve on hold.

This view challenges growing concerns that this year’s strong rally has left equities vulnerable to a pullback. Instead, the Wall Street powerhouse, which manages $4.3 trillion in assets, contends that economic momentum is strengthening as companies ramp up spending on AI computing infrastructure, while high-income consumers continue to spend, supported by the so-called wealth effect from rising stock and home prices.

In its updated mid-year 2026 outlook, JPMorgan Asset Management also noted that bonds have become attractive again due to still-elevated yields, and emerging markets warrant overweight positions given their deepening ties to Asia’s semiconductor supply chains. To achieve portfolio diversification, the firm recommends not only increasing allocations to leaders in the AI computing infrastructure ecosystem but also adding defensive alternative assets such as real estate, infrastructure, and transportation, along with exposure to Europe and Japan.

“In our base-case forecast, the good news is that we expect the economy to strengthen by mid-year,” said David Kelly, Chief Global Strategist at JPMorgan Asset Management. He added that this strength should be partly driven by income tax refunds and AI-related spending.

Kelly noted that whether the economy continues expanding into the fourth quarter hinges on whether Washington delivers additional fiscal stimulus, although the team’s base case assumes Democrats will regain control of the House of Representatives, thereby limiting the prospects for fiscal stimulus in 2027.

“For Americans, this is a remarkably resilient economic expansion; for global equities, it’s an exceptionally favorable backdrop,” he said. “What truly matters for stocks is earnings and interest rates—and earnings growth has been outstanding.”

Although inflation remains elevated, the economic backdrop has grown stronger. Consumer prices rose 4.2% year-over-year in May, the fastest pace in three years. Nevertheless, Kelly expects inflationary pressures to gradually ease over the remainder of 2026 and into next year, assuming a durable resolution to tensions in the Strait of Hormuz. Declining energy costs, slowing housing inflation, and contained wage growth are expected to help moderate price increases.

“We do not forecast a recession,” he said. “The wealth effect and the AI boom are keeping us moving forward.” On interest rate expectations, the JPMorgan team stated they do not anticipate the Federal Reserve raising rates at any point over the next two years. Kelly also raised the possibility that the central bank could cut rates next year.

Kelly described the 2026 investment landscape as defined by the tension between rising political and economic risks and the persistent supportive force of an AI-driven surge in spending on computing infrastructure.

“That really captures where we stand economically and in financial markets at mid-2026,” Kelly said, adding, “There are many crosscurrents,” and citing excessively high market valuation multiples, economic nationalism, political polarization, ongoing Middle East conflicts, immigration issues, and tariff risks.

Yet, 'at the same time, amid all these circumstances, we are witnessing an enormous, unprecedented AI infrastructure boom—both in terms of the potential of this technology and, more specifically, from the perspective of the massive capital expenditures currently being undertaken by hyperscale cloud providers.'

Kelly noted that earnings growth in international equity markets is increasingly driven by long-term secular trends tied to the AI infrastructure and AI application wave, rather than the business cycle. He also cautioned against excessive leverage in allocations to Asian tech stocks, stating that markets such as South Korea and Taiwan now have exposures to 'hardware-centric, chip-related technologies' that are approaching roughly twice that of the U.S. He expects both markets to rank among the top performers. 'Given the gains we’ve already seen, we are in the fourth year of a very strong equity bull market—and concentration risk is growing,' he said.

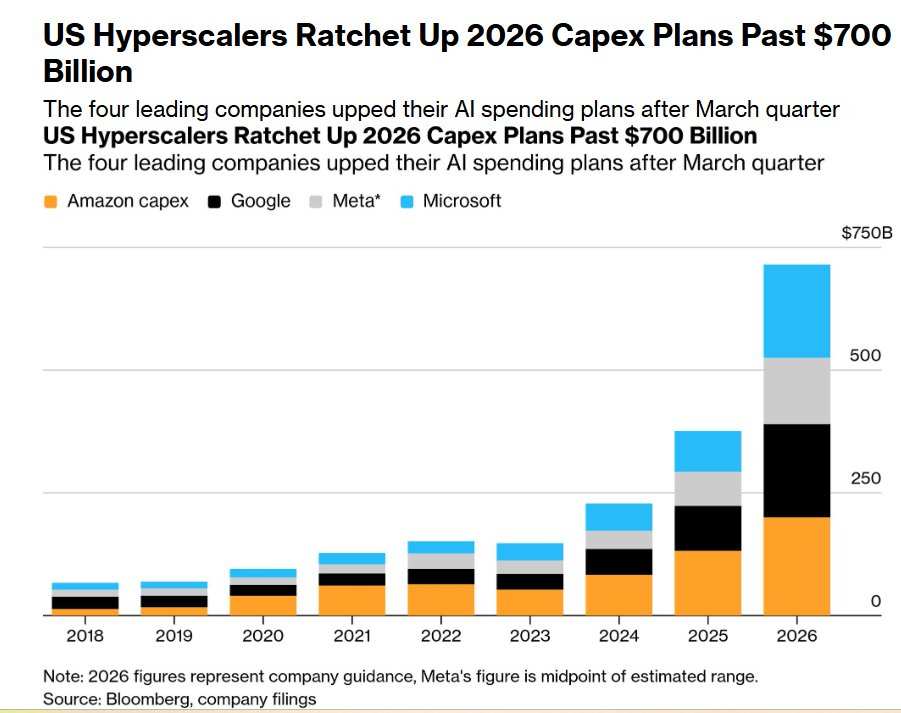

$7.6 Trillion Infrastructure Surge Arrives! From Code Dividends to the AI Infrastructure Super Cycle, the AI Bull Market Is Far from Over

A recent Goldman Sachs research report indicates that AI CapEx—the capital spending associated with artificial intelligence—is no longer limited to large-scale purchases of NVIDIA Blackwell/Rubin AI GPU compute clusters. Instead, it now encompasses a comprehensive, system-wide investment across the entire AI factory value chain, including data center power equipment, liquid cooling systems, data center CPUs, DRAM/NAND/HBM memory, optical communications and interconnects, high-performance Ethernet networking infrastructure, data center interconnect (DCI) high-speed links, transformers, and gas turbines. On Wednesday, NVIDIA CEO Jensen Huang stated that artificial intelligence could usher in a new era of manufacturing and industrial growth in the United States.

According to Goldman Sachs’ base-case framework, hyperscale cloud providers are projected to invest approximately $770 billion in 2026—nearly equivalent to their total operating cash flow. The firm forecasts cumulative AI infrastructure capital expenditures of around $7.6 trillion between 2026 and 2031, with annual AI CapEx reaching at least $765 billion in 2026 and rising to approximately $1.6 trillion by 2031. In the view of Goldman Sachs analysts, the market’s pricing logic for the AI wave is shifting from 'who develops the most powerful AI foundation models or AI application software' to 'who can rapidly build AI compute clusters, deliver massive-scale power and cooling, accelerate intra-data-center optical interconnects and inter-data-center DCI links, and continuously iterate the next generation of AI factories.'

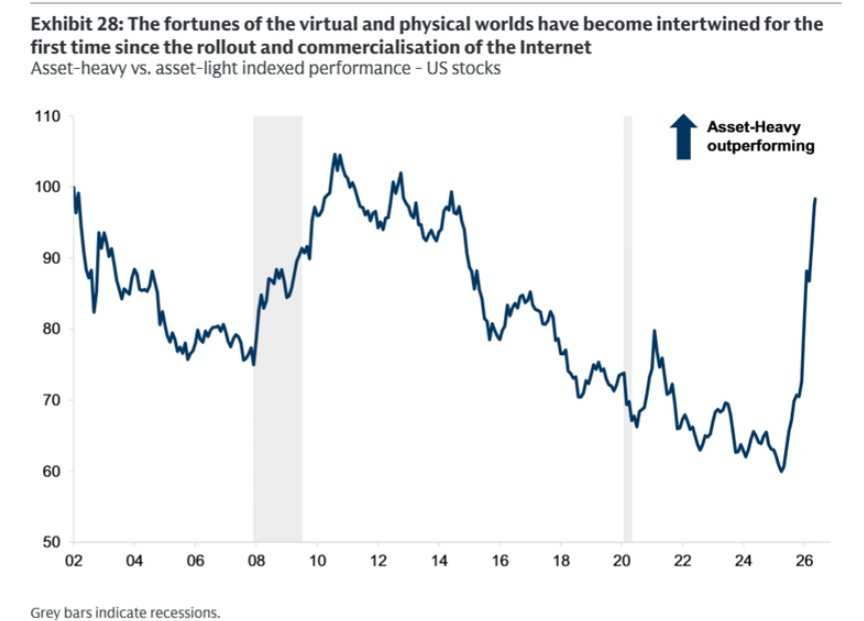

Goldman Sachs Global Investment Research points out that AI infrastructure companies with substantial physical assets have already begun outperforming asset-light technology firms. This stems from a fundamental shift: today, advances in artificial intelligence require not only clever code and software engineering but also robust physical infrastructure. Building the backbone of machine learning systems entails investing in data centers, power grids, cooling systems, raw materials, and heavy machinery.

This stands in stark contrast to the investment landscape that prevailed in financial markets following the 2008 global financial crisis. For much of the past decade-plus, asset-light software companies—despite minimal capital expenditures—commanded premium valuations. Low interest rates and sluggish economic growth made software firms and digital super-platforms the preferred choice for growth-seeking investors. Meanwhile, traditional industrial sectors struggled due to prolonged neglect, overcapacity, and persistently disappointing returns.

The current economic environment is reversing this dynamic. Strong nominal output growth, persistent price pressures, and sustained massive capital expenditures on AI projects are creating new revenue streams for sectors long overlooked by investors. According to Goldman Sachs’ data, asset-intensive equities—after years of underperformance relative to asset-light stocks—have recently staged a significant reversal and are now outperforming them.

According to analysts at Bank of America, another Wall Street financial giant, AI computing infrastructure is entering a more durable and expansive capital expenditure cycle. Around the same time, Morgan Stanley, yet another Wall Street powerhouse, published a research report indicating that the AI computing arms race has entered a phase of system-level expansion, with demand for AI infrastructure displaying an unusual 'inelastic' trend—meaning that regardless of cost curves, major tech firms continue to ramp up investments in AI data centers. This 'demand inelasticity' is expected to further bolster U.S. economic resilience and drive overall earnings growth for the S&P 500. The report forecasts that nearly $3 trillion in AI-related infrastructure investment will flow through the global economy by 2028, with over 80% of that spending still ahead.

At Taiwan Semiconductor’s recent annual shareholder meeting, CEO C. C. Wei stated that demand will exceed supply for many years to come, and even with new U.S. capacity coming online, the company will struggle to fully meet AI-driven demand in the coming years. On the specific outlook for AI-related capital expenditures, Wei’s remarks—'I don’t know where the peak is' and 'we don’t see any signs of demand slowing down'—were arguably the most bullish statements from a major player in the AI compute supply chain during the event.

Editor/Deng