Waller’s debut sent multiple strong signals indicating imminent change, including a significantly shortened statement and a reduced duration for the press conference. Waller stated that the Committee is clearly and unanimously committed to achieving price stability and attaining the 2% inflation target. A special task force has been established to review the Federal Reserve’s $6.7 trillion balance sheet and examine whether monetary policy transmission stems from interest rate tools or balance sheet instruments. Waller did not submit his own dot plot interest rate projections, while all other officials did; half of them projected at least one rate hike this year, and the other half anticipated rates would remain unchanged or decline. Following the Fed’s statement and press conference, U.S. equities plunged and Treasury yields surged.

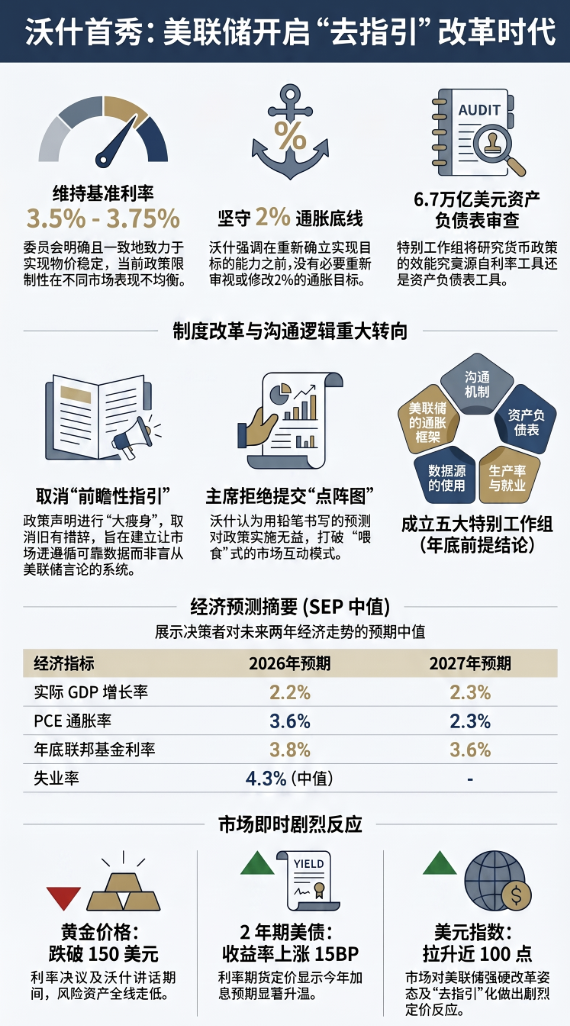

In his first FOMC press conference as the new Federal Reserve Chair, Waller announced that the benchmark interest rate would remain unchanged at 3.5%–3.75%, stating that the Committee is clearly and unanimously committed to achieving price stability and its 2% inflation target.

Simultaneously implementing reforms, the statement issued today eliminated the long-standing 'forward guidance' and announced the immediate formation of five special working groups—on communication mechanisms, balance sheet operations, use of data sources, productivity and employment, and the Fed’s inflation framework—with a mandate to deliver recommendations for improvement by year-end.

One of these special working groups will review the Federal Reserve’s $6.7 trillion balance sheet and examine whether monetary policy transmission stems from interest rate tools or balance sheet instruments.

One of these special working groups will review the Federal Reserve’s $6.7 trillion balance sheet and examine whether monetary policy transmission stems from interest rate tools or balance sheet instruments.

Waller declined to submit his personal economic projections (Summary of Economic Projections, SEP). Among the 18 policymakers who did submit forecasts, there was a clear divergence on the interest rate outlook: half projected at least one rate hike this year, while the other half expected rates to remain unchanged or decline.

From the release of the rate decision until the conclusion of Waller’s remarks, risk assets such as U.S. equities declined across the board; gold plunged by more than $150; the 2-year U.S. Treasury yield rose by 15 basis points; the U.S. Dollar Index surged nearly 100 points; and fed funds futures repriced the expected pace of rate hikes this year upward by 18 basis points, to 39 basis points.

Upholding the 2% inflation floor, he indicated that current policy restrictiveness is 'uneven.'

Facing persistently elevated prices over the past five years, markets are closely watching the Federal Reserve’s tolerance for inflation. Walsh showed no compromise on this point:

“Today, I announce that this Committee has made a clear and unanimous decision that we will achieve [the 2%] target.”

“The members of the FOMC are clear and unanimous in their view that this Committee will achieve price stability.”

When asked whether the Fed might revise its 2% inflation target, Walsh dispelled market speculation with his characteristic bluntness:

“There is no need to revisit the target until we have reestablished our commitment to—and credibility in achieving—the 2% inflation goal.”

Regarding whether current interest rates are sufficiently restrictive, Walsh offered a telling assessment—'uneven.' He noted:

“If I look at the housing market as an example, Federal Reserve policy appears somewhat restrictive. But if I were to describe what’s happening in financial markets, it would be difficult to use the word ‘restrictive.’”

This statement signals that the Fed has recognized that soaring asset prices have not reflected the intended tightening effect of its current monetary policy.

Establishing five major working groups tasked with reviewing the Federal Reserve’s balance sheet, reducing data inaccuracies, and other objectives

To fundamentally transform how the Federal Reserve operates, Walsh announced the immediate creation of five special task forces, each focused on: Fed communications, the balance sheet, use of data sources, productivity and employment (including the impact of AI), and the inflation framework. He expects these groups to deliver their findings by the end of this year.

Waller stated that one of the independent working groups he is assembling will “review the benefits and risks of the current ample-reserves regime and the composition of the balance sheet,” and study “whether monetary policy operates primarily through interest rate tools or balance sheet instruments.”

When discussing the data working group, Worshe offered sharp criticism of existing economic statistical methods. He argued that the outdated survey methodologies relied upon by central bank officials fail to accurately reflect the current state of the U.S. economy, and that data releases suffer from significant lags.

“Some of the data we receive… may just be ‘echoes of history.’ We need to narrow these error margins. What truly interests us is what is happening right now—not echoes of history.”

Forward guidance has been discontinued in this meeting, and the Chair unprecedentedly declined to submit the dot plot.

The most surprising development for investors at this meeting was the significant streamlining of the Fed’s policy statement. At the press conference, Waller stated directly:

“You may have noticed one difference in today’s policy statement. It is shorter, more concise, and omits certain longstanding phrases. Notably, so-called ‘forward guidance’ has been excluded—we unanimously agreed it is not suited to the current policy mix.”

Moreover, breaking with precedent, Chair Waller explicitly declined to submit his own Summary of Economic Projections (SEP) and associated dot plot. He explained:

“I reviewed the dot plot, and when I saw what had been submitted, I noticed that all entries were written in pencil—the kind with a large eraser... To me, that offers no help in implementing policy.”

Although Chair Waller did not submit his own forecasts, the median of SEPs submitted by other participants indicates: real GDP growth of 2.2% this year and 2.3% next year; headline PCE inflation of 3.6% this year and 2.3% next year; and an unemployment rate of approximately 4.3%. The median projection for the federal funds rate stands at 3.8% by year-end and 3.6% by the end of next year.

Ending the era of 'spoon-feeding' market interactions, citing AI as a source of massive demand

For a long time, Wall Street has been accustomed to pricing assets based on statements made by Federal Reserve officials. At the meeting, Worshe explicitly stated his intention to break this 'spoon-feeding' pattern of market interaction. Worshe emphasized:

“When financial markets merely reflect what we say, we are discarding our most valuable source of information and turning a blind eye to it.

I want us to build a system that removes these blinders and allows markets to follow data they consider reliable. They will then deliver better information to us through market prices, enabling us to make more informed decisions.”

Addressing the market’s focus on artificial intelligence (AI), Bessent defined AI as 'the most significant change experienced in adult life' and noted that AI has generated substantial demand—evident in data centers, power, and related sectors—but expressed uncertainty regarding the pace of supply-side expansion.

‘AI may be the most transformative development I’ve witnessed in my adult life for the economy, business, and households. If we do our job well, we can achieve a combination of strong growth, low prices, and robust employment.’

The following is a translation of Worshe’s remarks at the press conference:

Worshe

Good afternoon, everyone. It is an honor—truly an honor—to return to the Federal Reserve and assume this responsibility at such a consequential moment. I am especially encouraged by the warm welcome from both old friends and new colleagues. I have also listened carefully to my FOMC colleagues, absorbing many new ideas, fresh perspectives, and a genuine commitment to advancing the Federal Reserve’s mission.Worshe

This week’s FOMC meeting fully embodied the finest traditions of the Federal Reserve: rigorous debate, open-mindedness, commitment to our mission, and a sense of accountability and responsibility for performance. In our field, all of this ultimately comes down to one thing: formulating the right monetary policy—or as close to right as possible. That is our North Star.Worshe

My colleagues and I are here to fulfill our statutory mandate, as you have heard us state before: price stability and maximum employment. These objectives guided all our work during the meeting we just concluded.Worshe

As you saw just minutes ago, the Committee decided to maintain the target range for the federal funds rate at 3.5% to 3.75%. To support the Federal Reserve’s dual mandate, the Committee also reaffirmed its policy of maintaining ample reserves in the banking system. Despite heightened uncertainty—partly due to conflicts in the Middle East—the economy continues to expand at a solid pace. Productivity growth and capital investment remain strong, employment growth is keeping pace with labor force growth, and the unemployment rate has changed little. We recognize that inflation has remained well above the Federal Reserve’s long-stated 2% inflation objective. This situation has persisted for more than five years. Persistently high prices are a burden on the American people, but past experience does not necessarily dictate future outcomes.Worshe

I am pleased to report that FOMC members were clear and unanimous in their view that this Committee will achieve price stability. Leadership transitions at any institution present a natural and timely opportunity to reaffirm its mission, review current practices, and consider whether those practices best serve our objectives. My Federal Reserve colleagues and I will work closely together to explore what changes might help improve the implementation of monetary policy.Worshe

At this point, you may have already noticed a difference in today’s policy statement. It is shorter, more concise, and omits some of the older language. This statement simply presents the facts to you as we see them. The so-called ‘forward guidance’ is no longer included, as we unanimously agree it is ill-suited to the current policy mix.Worshe

This afternoon, you will also receive the usual Summary of Economic Projections (SEP). It has been the Committee’s consistent practice for participants to submit these projections, and I encourage my colleagues to continue doing so. However, I myself have not provided any projections, which aligns with my longstanding view regarding the SEP—particularly in its current structure. The median projection among participants shows real GDP growth at 2.2% this year and 2.3% next year; overall PCE inflation at 3.6% this year and 2.3% next year; and an unemployment rate of approximately 4.3%. The median federal funds rate projected by participants stands at 3.8% at year-end and 3.6% at the end of next year.Worshe

Now, please allow me to say a few words about a key initiative we are announcing today. I will appoint a special task force in each of five areas critical to the broad implementation of monetary policy. First, Federal Reserve communications; second, the Federal Reserve’s balance sheet; third, our use of and reliance on existing data sources; fourth, productivity and employment during periods of transition; and finally, the Federal Reserve’s inflation framework.Worshe

These issues are timely and important, and in my view, warrant fresh examination. My colleagues and I have engaged in vigorous and purposeful discussions about them over the past few days. For each individual task force, I am recruiting some of the best talent, both from within and outside the economics profession. They will be supported by subject-matter experts from our outstanding Federal Reserve staff and will be given a clear mandate.Worshe

Starting from first principles, they will ask sharp questions, scrutinize current practices, consider alternatives, and ultimately make recommendations to policymakers on next steps. Since last summer, my colleagues have discussed potential improvements to the form and function of Federal Reserve communications. This new task force will build on that work, and I expect it to propose thoughtful changes—including suggestions regarding the SEP I just mentioned. The second task force, on balance sheet policy, will review the benefits and risks of the current ample-reserves regime and the composition of the Federal Reserve’s balance sheet. It will also assess alternative frameworks for implementing and operating monetary policy.Worshe

The third working group—the Data Working Group—will evaluate new sources of information and consider methodological changes to improve data collection, with the aim of providing policymakers with more accurate, relevant, timely, and perhaps most importantly, actionable information about the state of our economy.Worshe

Fourth, the Productivity and Employment Working Group will examine the pace, scope, and economic impact of new general-purpose technologies, including artificial intelligence, and explore their potential implications for the Federal Reserve’s dual mandate on employment and inflation.Worshe

The final working group—the Inflation Framework Working Group—will study the drivers of inflation and, fundamentally, explore various approaches to achieving price stability in an evolving economy. In the coming weeks, you will hear more about these working groups and this broader initiative. For now, let me make one simple statement: each working group will serve a shared objective held by everyone across the System—and by everyone who sat around the table with me over the past few days—a Federal Reserve that is clear-eyed about its mission, aligned with its goals, and focused on the future. Thank you for your attention, and I’d be happy to take your questions.---

Speaker 2

Hello, Chair Worshe. It’s great to see you again, and welcome back. You’ve moved quickly to launch so many initiatives—what timeline do you envision for each of these working groups?Worshe

I think that will depend on each individual working group—and also on how urgently we need clear answers. My expectation—while I’m still in the process of recruiting and finalizing members—is that the groups will begin their work in the coming weeks. We’ll start receiving more input from them by late summer regarding how they frame the issues. Ideally, most—if not all—will reach conclusions by year-end.Speaker 2

Specifically regarding the inflation framework, you mentioned first principles. Does this include a review of the 2% target itself? You’ve previously said that the digits to the right of the decimal point don’t matter. Does this imply starting from the premise that 'a point target of 2% is overly rigid'?Worshe

Let me break this into two parts. First, with regard to the review of the inflation framework, its mandate is: What drives inflation? To what extent is the Federal Reserve responsible for inflation? How do we measure inflation? But this would overlap somewhat with my data working group. Regarding the 2% inflation target—this is the long-standing 2% target held by the Federal Reserve. As you’ve heard me say before, I tend to focus on the digit to the left of the decimal point. Well, 2 is now the digit to the left, and zero is to the right. I believe there’s no need to revisit this target until we have reestablished both our commitment to and our capacity for achieving the 2% inflation objective. Therefore, this is not within the scope of our current work.Speaker 3

Kobe, thank you very much. I’m Kobe Smith from The New York Times. You’ve previously stated that inflation is a choice. The policy statement released today includes your reaffirmed commitment to achieving price stability. However, looking at the Summary of Economic Projections (SEP), most of your colleagues expect core PCE inflation to be around 3.3% by year-end, with the 2% inflation target not being reached until 2028. So I’m curious: at this juncture, how much patience does the Federal Reserve have in waiting for one-off inflationary pressures to dissipate and for inflation to subside after years of elevated readings? Under what circumstances would you support the Fed taking action and raising interest rates?Worshe

Alright, there are quite a few questions here. Let me try to unpack them. First, we have both the ability and the commitment to achieve our 2% price stability objective. That is precisely what we intend to do. In the Federal Reserve’s strategic reviews over the past few years—including the one conducted in January, under which we remain bound—the Fed stated clearly that inflation is primarily determined by monetary policy. Of course that’s true. I’ve been saying for years that inflation is a choice. Of course it is. Today, I announced that this Committee has made a clear and unified decision to achieve this goal. The rest of your question sounds like an invitation for me to offer forward guidance. We have abandoned forward guidance. Some members of the Committee—I suspect, based on our discussions over the past few days—have moved away from it because providing forward guidance at this moment feels inappropriate. Others hold a different view, believing as a general proposition that forward guidance is not something we should engage in. But this will be handled by the communications working group and my fellow policymakers. We will listen carefully to expert input and then make our own decisions. However, I cannot provide any forward guidance regarding our next steps. The good news is that we’ll meet again in six weeks.Speaker 3

I’d like to follow up on that: given the data we’re seeing and the forecasts, how restrictive do you consider current policy settings to be?Worshe

I’ve heard various descriptions both inside and outside the Federal Reserve. Let me share my own view: it’s uneven. Take the housing market as an example—Federal Reserve policy is not the sole determinant of conditions in that market. But overall, I would say Fed policy appears somewhat restrictive there. However, if I were to describe what’s happening in financial markets, it would be difficult to use the word 'restrictive.' So I call it uneven. This may reflect differences in how monetary policy is transmitted through various channels, whether via our interest rate tools or balance sheet tools. The good news is that we also have a working group on this issue—the balance sheet working group—which will examine it more deeply.Speaker 4

You mentioned you’re not fond of forward guidance, and it was removed from the statement this time. Yet the dot plot shows nine participants indicating they expect a rate hike by year-end, which markets have interpreted as forward guidance. What does this mean for how you guide markets and for the future of the dot plot?Worshe

I’ll give you the same answer I gave Ms. Smith. We have a working group on this matter. Let me add a bit more. I reviewed the dot plot, and when I saw the submissions, I noticed they were all written in pencil—you know, the kind with a big eraser. That tells me my colleagues, when submitting their dots, understood that the world changes quickly and didn’t feel bound by what might happen six weeks—or even six days—later. In case circumstances change... I’d also like to highlight a few other points. What I heard around the table was that when they submitted their model forecasts—it’s important to clarify—this wasn’t meant to suggest that outcome was more likely than others; it simply indicated it was more probable than alternative scenarios. So I didn’t hear overwhelming confidence. What I heard was humility, and I believe we should have that humility. I did not submit a dot myself. For me, it doesn’t help with policy implementation. As I mentioned in my opening remarks, I anticipate that by year-end, we will review all aspects of our communication—the press conferences, the dot plot, meetings, transcripts, and minutes—and this will be part of that review. I don’t want to prejudge the outcome, but I’m quite open to possible results. Over the past few days—and frankly, over the past three weeks—I’ve been extremely impressed by how open my colleagues have been to change and to simple changes that carry risks. But our primary goal remains getting monetary policy right. And the way to get monetary policy right is to fulfill the mandate Congress has given us—to achieve price stability—and on that point, there is no disagreement.Speaker 4

We might get the same answer about the working group... On communication, what are your thoughts on these press conferences? Do you plan to continue holding one after every meeting? Do you find them useful? What does the future hold for Kevin Warsh’s approach to communication?Worshe

Well, we probably have another 15 to 20 minutes left, so I don’t want to prejudge the outcome. Press conferences can be a very useful way to communicate with households, businesses, and more broadly through media outlets like yours. I had a great late mentor named George Shultz, whose maxim was: press conferences are useful—but when you hold one, make sure you have something important to say. Today, I believe we do have something important to say: our commitment to achieving price stability and our commitment to rethinking our practices to move the Federal Reserve forward. To ensure that you and the American people see these commitments not as wishful thinking but as concrete ideas, we will seek out the best minds—whether from within the Fed, or from business, economics, academia, technology, and other fields I’m familiar with—to share their perspectives. That’s what we’ll do here: pursue the truth. I think we’ll come up with some new and interesting ideas. We’ve already made some changes today. I expect more changes ahead, some of which may well warrant a press conference.Speaker 5

Hello, I’m Chris Rugaber from the Associated Press. Thank you for taking our questions. Could you share your longer-term view on inflation? I understand you may not comment on short-term fluctuations, but is this primarily being driven by energy prices and the conflict involving Iran? Or do you have concerns about underlying inflationary pressures in the economy? Thank you.Worshe

I can’t say it better than the Committee just did, so let me reiterate. Inflation remains elevated relative to the Committee’s 2% objective, partly reflecting supply shocks that have pushed up prices in certain sectors, including energy. The statement goes on to say—but make no mistake—the Federal Reserve will achieve price stability. My own judgment is that the Committee has devoted considerable time over not just these two days but several weeks to discussing this issue. That is what we are prepared to say about inflation at this time. But our commitment to achieving this goal is resolute, consistent, and clear. I believe this is an important message we’ve missed over the past five years, and we will correct that.Speaker 5

Okay. Also, regarding your data working group and other aspects—I mean, generally speaking, I think people feel the Fed has already taken all data into account. Certainly, that was the perception before. Is there any data you feel hasn’t received sufficient attention? I mean, you’ve previously mentioned the tendency toward ‘mean reversion,’ but again, that’s well known among most Fed officials. So what is this working group looking at? What might the outcomes be? I know you don’t want to prejudge the results, but are there examples of data you expect will receive more emphasis? Thank you.Worshe

So, you’re asking me a question. Let me say this: I don’t want to prejudge the outcome, nor do I want to over-specify what they will do, because I still need to make a call or two before I finalize who will lead this effort. I am very interested in what external experts think about this matter. Here’s what I’ll say: broadly speaking, much of the data consumed by U.S. central bankers and other government officials comes from old-fashioned survey methodologies based on national accounts... and the picture they paint of the U.S. economy looks vastly different from what the U.S. economy will look like in 2026. Survey response rates fall short of what we need, and the questions being asked may have been perfectly appropriate a generation ago but are far less relevant today. Therefore, even within official statistics, I’m open to recommendations—from the working group and our own best thinking—on how to use new analytical methods to bring these official statistics up to a standard befitting our era. I’d also add that nearly every CEO running their own business relies on real-time information that isn’t subject to massive revisions and tells them what just happened. As you know, monetary policy operates with normal, long, and variable lags. What we’re truly interested in is what’s happening right now—not the echoes of history. From my remarks, you can probably infer that some of the data we receive—like the employment cost index or other indicators released on the first Friday of each month—may merely reflect historical echoes, even if they become quite useful by their third revision. We need to narrow these error margins because we must make difficult decisions in real time. I’m highly confident we can learn a great deal from new data sources in the private sector, reforms in official statistics, and advanced analytical techniques that are far more sophisticated than simply asking whether something is core or non-core.Speaker 6

Thank you. Welcome, Mr. Chair. I’m with Fox Business. If you don’t provide much ongoing forward guidance, won’t markets experience greater volatility? Shouldn’t Americans have a clearer sense of your thinking about the future?Worshe

I believe financial markets perform best when they respond directly to incoming data. I think they are less efficient when they instead ask, 'How will the Federal Reserve react to incoming information?' The more markets focus on what is actually happening in the real economy—judging what constitutes good data versus weaker data—the better they can price in both the most likely outcomes and tail risks. Financial market prices may be the single most important source of information guiding central bankers. However, when financial markets merely reflect what we say, we are effectively taking away our most valuable source of information and turning a blind eye to it. I would like us to build a system that removes those blinders, allowing markets to follow the data they deem credible. They will pay attention to the data, and so will we. Through market prices, they will deliver better information to us, enabling us to make more informed decisions. But ultimately, the objective I set at the outset—to achieve the price stability mandate assigned to us by Congress—is what we must pursue.Speaker 6

If I may bring you back slightly into the meeting—this was your first meeting. The Board members appeared quite hawkish. As you listened to their remarks overall, was there any discussion about potential future rate cuts?Worshe

Today? There was only one proposal on the table. No other proposals were discussed. Regarding that proposal, I would say the discussion was quite limited. There was consensus and clarity around it. It is customary for this central bank—and others—to have a range of alternatives available. Today, we had just one. I believe the further discussion helped deepen our understanding and clarify what we need to do and how to achieve it. I don’t want to prejudge what may happen in the future, but for us, there was only one key issue. We accepted it. We had several days of productive internal debate, and ultimately, I think we are in a better position as a result.Speaker 7

Thank you very much. I’m Claire Jones from the Financial Times. You know, when reading the very concise statement—which I think all of us here greatly appreciate—one might wonder: given what you’ve said here about inflation risks in the U.S. and your responsibilities, why not raise rates today? So my first question is, why not? What would you need to see before taking action to hike rates? Second, regarding your working group, would you consider drawing on any best practices from other central banks? Thank you.Worshe

I’m glad they’re used to letting you ask two questions, because my answer to your first question will be very brief: beyond the statement itself, I have nothing further to add. In response to an earlier question about how markets react to our unfiltered remarks, I believe that is more helpful than issuing a statement and then improvising afterward. On best practices for the working group—this is something I’ve thought about. I’ve also participated in a working group or two myself over the years. Best practices include: identifying the smartest people; ensuring the group comprises individuals with diverse backgrounds and perspectives so they can engage in internal debate; and making sure that the teams who will ultimately receive the group’s output feel they have a stake in it. That’s why we are currently identifying—though the list isn’t finalized yet—some of the top talents from within our building and across the regional Reserve Banks, covering every relevant discipline, and seconding them to this group for several months. This way, the working group’s leadership can understand how the world’s most analytically rigorous central banks approach these issues and incorporate those insights into our own best practices. We are not outsourcing decision-making to anyone. The Board and the Reserve Banks selected the 19 individuals currently at the table. These will be our decisions. We may agree with some recommendations and disagree with others, and we’ll have robust internal debates about them. But I hope and believe their work will make our internal discussions better, stronger, and more dialectical, ultimately helping us achieve our price stability mandate.Speaker 7

Just a quick follow-up on the market view you mentioned. If you look at two-year Treasury yields, they actually suggest the market believes more tightening is needed. Is that also how you interpret the message conveyed by two-year yields?Worshe

Hmm? We were in a very good place. I think that’s precisely why we’re not answering the third question. I’m not going to comment on the market’s reaction over the past 30 or 60 minutes. What we’ve given the market is a new chapter for the central bank—some new thinking. What we’ve given markets, households, and businesses, I believe, is a commitment to ask ourselves tough questions so that we can deliver on promises we’ve previously made. That represents a lot of change for financial markets to digest. I won’t be particularly focused on their initial reactions over the first few minutes or even days. What matters most, I believe, is that financial markets—and at least equally important, households and businesses—understand that this central bank will achieve price stability.Speaker 8

Hello, Chair Worshe. I’m Brian Zhong from NBC News. Thank you for taking our questions. When you say we’ve abandoned forward guidance, to an average person that might sound as though the Fed will communicate less or offer less insight into where borrowing costs are headed. So, how would you explain this to someone you might meet in a grocery store—someone whose grocery bills are rising faster than their wages? I don’t know—maybe ‘working groups’ are the answer. But how would you communicate this era, this new chapter for the Fed?Worshe

If I told someone standing in front of the milk shelf that I had a working group to handle this, I think that would go over very poorly. So thank you for your question. If I met someone in the grocery store, I’d tell them: We can’t have a significant impact on specific prices—like today’s oil price or even the price of a dozen eggs. Those aren’t what primarily drive what we do. But we have a very important job: to ensure that changes in the prices of oil, beef, eggs, or milk don’t spread through the economy and trigger second- and third-round effects. That is our job, our commitment, our capability—and we will deliver on it.Speaker 8

Is the Federal Reserve’s relationship with the Treasury Department also under review? There are typically breakfast meetings with the Treasury Secretary. Do you intend to continue those? Have you spoken with the President since your swearing-in?Worshe

Regarding the President, I have nothing to tell you. As for the Treasury Secretary, he has been posting photos of his breakfast. So I suppose I can't deny the long-standing tradition of weekly meetings between the Chair of the Federal Reserve and the Treasury Secretary. I believe we’ve had three such meetings so far. He’s overseas this week, so that will be an exception. I find these discussions very useful. The objectives of the central bank, as well as our roles and responsibilities, are quite clearly distinct from those of the fiscal authorities. In my view, monetary policy is independent in what we do. That doesn’t mean we’re uninterested in what’s happening at the Treasury. My way of thinking about it is that this central bank needs broad vision but focused responsibilities. We need to be highly attentive to what’s going on in the world. I won’t reveal anything here by saying we’re very interested in developments in the Middle East—that does affect our day-to-day work to some extent. That doesn’t mean it’s our responsibility, but I believe we maintain a broad perspective. My meetings with Secretary Bessent so far have helped broaden that perspective, enabling us to be aware of developments that could impact our daily work, even if they’re not directly within our purview.Speaker 9

Steve Liesman, CNBC. Mr. Chairman, thank you—and thank you for taking my question. Before you became Chair, you said you believed productivity was a reason the Fed could lower interest rates. Do you still hold that view?Worshe

The Committee discussed productivity today. AI was mentioned. My prior view—and one I’ve expressed in public commentary—is that artificial intelligence, as the latest generation of general-purpose technology, may represent the most significant transformation the economy, businesses, and households have experienced in my adult lifetime. It is full of enormous opportunities and risks. I take both very seriously. You may have heard me say that AI is shorthand for American ingenuity. That doesn’t mean it will be easy. It certainly doesn’t mean it won’t be disruptive. But over the long run, my belief—echoed with considerable support in today’s Committee discussion—is that the United States stands to win, and that America will ultimately be better off as we move forward along this path. Now, returning to policy implementation—the timing, scale, speed, and impacts on output and employment—this is precisely one of the things our working group was established to address.Speaker 9

If you don’t mind a follow-up from a different angle: when you see strong job growth, elevated inflation, solid GDP performance, and surging stock markets—when you look at the economy overall, do you consider the federal funds rate to be restrictive?Worshe

So that’s your second question. I’ll give the same answer I gave earlier. When I think about policy implementation, what matters is the effect of policy—not what we say, but what actually happens. The best way I can describe the current situation is uneven. I do see some restrictiveness in certain areas, such as the housing market. But it’s difficult to apply that same description elsewhere. Let me add one more point. You mentioned one part of our dual mandate—the employment aspect. I don’t believe we face a cruel trade-off. I disagree with the view expressed generations ago that a Fed Chair standing at this podium must declare that you have to choose—you must decide whether you’re willing to tolerate higher inflation to achieve greater employment. I don’t believe that. What I do believe is that if we do our job well, we can make strong growth, low prices, and robust employment mutually compatible. So what you heard from the Committee today is that we still have work to do on price stability.Speaker 10

Thank you. I’m Nick Timiraos from The Wall Street Journal. Chair Waller, you’ve said many times that credibility is earned through delivery. If credibility must be earned through delivery, then the action should be tightening—or at least threatening to tighten. Yet you did not do that today. Why?Worshe

That judgment you expressed has not been voiced by any of the 19 people in this room. We will meet again in six weeks and revisit this issue.Speaker 10

If I may ask a question about AI: infrastructure development is generating enormous demand—capital expenditures, data centers, power—and the productivity returns may be further out. In your assessment today, does AI primarily boost demand or supply?Worshe

That’s an excellent question for both central banks and the economics profession. We spend most of our time measuring demand. It’s easier—we can see it, calculate it, check it, and revise it. But what we’re trying to do is infer supply. You’ll notice that in the second paragraph of what one of your colleagues described as a very brief statement, we have one sentence on the demand side and another sentence of equal length on the supply side. Both are important; just because we can measure one more precisely doesn’t mean we favor it over the other. Regarding AI and the growth in data centers and related infrastructure, we are clearly capturing the demand-side effects, which are already showing up in GDP data. However, when it comes to inferring the timing and magnitude of supply-side effects, we are far less certain. Intuitively, the supply side will likely expand—but it will take longer. I’d describe it this way: there’s a race between supply and demand. As Milton Friedman once said, the only thing we know in economics is that there’s a supply curve and a demand curve, and eventually they intersect. What does this mean for policy? The good news is that we have a working group focused on this issue.Speaker 11

Thank you, Mr. Chair. It sounds like, with regard to the data working group, you’re considering a comprehensive overhaul of the national accounts system—the way the government measures the economy. Is that your objective?Worshe

In one word: No. In a few words: Much of this data collection occurs at other government agencies, for which we have great respect and deference. However, if during the process we offer suggestions—suggestions that Federal Reserve staff have already begun developing—on what they could do to help us as policymakers obtain information, we will not hesitate. Again, I do not wish to try to define the precise boundaries of what the data working group will examine. But I do believe there will be a review of official statistics, and equally—if not more—importantly, consideration of best practices from the private sector and new analytical tools enabled by AI. This would allow us to integrate them in a way that provides us with better real-time information. As I mentioned earlier, this means that when we make decisions, we are acting on genuinely concurrent data, rather than what we call concurrent data but is, in fact, a historical echo.Speaker 11

Okay, thank you. Another question I’d like to ask relates to the building renovation. Are you considering making any changes to the renovation project, given that it has, to some extent, become a political football over the past year?Worshe

I’ve heard some things about that. I don’t think I’m revealing anything confidential, but my view is simply that when you join a new institution, it’s good practice to meet with the Inspector General. I intend to continue that practice. I’ve already had one meeting with the Inspector General. He told me something I believe is widely known—that he will issue a report later this summer regarding the building and the building project. I will be very interested in reading that report. From my perspective, looking forward—from now until project completion—what can or should we do to be the best possible stewards of taxpayer funds and ensure we fulfill the commitments we’ve made? There is still work to be done. You probably won’t be surprised that in my first few weeks, I’ve been somewhat preoccupied with other matters, but I commit to fully addressing all aspects of the Federal Reserve’s responsibilities in the coming weeks.Speaker

Victoria Guida from Politico. I know you didn’t submit a forecast, but you are authorized to speak on behalf of the FOMC. So I wonder if you could tell us whether, in the SEP, the rise in inflation expectations is entirely due to the war involving Iran? And what was the discussion like regarding the increase in inflation expectations and the slowdown in potential growth?Worshe

My interpretation of the discussion at the meeting—and I must acknowledge that the SEP shows half of my colleagues believe that, given all developments, the policy rate should remain at its current level or lower by year-end, while the other half believe it should be higher. The 19th voter is me, and I did not submit a projection. There was a range of views on first-round versus second-round effects, with no consensus or firm conclusions reached. But we will meet again in six weeks. I believe by then we’ll know more, and I think my colleagues will be closely attentive to any new developments between now and then.Speaker

Could I quickly follow up on the SEP? You mentioned you’re still encouraging your FOMC colleagues to submit their projections, even though you yourself are not doing so. What do you see as the benefit of them doing that (even if you don’t)?Worshe

This is a commitment made by the FOMC—one that I hope we will fulfill. Our commitment is to achieve price stability. I expect that we will deliver on it by the end of this year. As I mentioned, I wouldn’t be surprised if a new communications framework emerges. There will be some changes. Regarding the SEP, that is a matter for committee discussion—a vigorous discussion. I believe we will have such a discussion. I am confident we will arrive at a better communications package to fulfill our commitment. But I don’t want to prejudge what those changes will be. Until then, however, I will continue to expect my colleagues to submit their SEPs. Some of them, I think, believe the current procedural structure is acceptable, but I’ve heard considerable interest in truly reforming all these aspects. You didn’t ask this, but I’ll answer anyway: The past few days have been very collegial, and the past few weeks quite constructive. This institution is eager to figure out how we can do better. It’s returning to first principles. I’m encouraged that what we’re doing in our statement—and the changes we’re considering regarding the SEP—reflect a genuine instinct to turn the page. By year-end, I hope we will have achieved something meaningful both in form and substance.Speaker

Could you please outline some of the principles guiding your own reaction function and tell us about the conditions under which you believe the Federal Reserve should respond?Worshe

That would be a very unsatisfying final answer to a question. The Federal Reserve has many responsibilities—not only monetary policy, but also supervision and regulation, consumer affairs, and payments. My own view is that our credibility comes from delivering on what we say across everything we do. In my first three weeks, I’ve spent more time on monetary policy than on all other matters combined. However, the more we fulfill our commitments as effective supervisors and regulators, the greater the benefits we accrue—and the stronger our credibility becomes in monetary policy. Look: When we achieve our price stability objective—and we will—the American people will feel that the hardships they’ve endured over the past five years due to inflation are behind them. And that credibility will generate dividends across all our activities. This institution will go into press conferences with a real momentum for reform and a drive to do better. But we will achieve something tangible.Speaker

Labor market data vary across regions. How would you characterize the labor market overall?Worshe

Is the labor market stable right now, or could it be a source of inflation? Thank you. Well, yes. If I were to capture the Committee's view, the Committee considers the labor market to be stable. Some members of the Committee believe the trend is even stronger than that. Trends matter more than individual data points. What happens over a three- or six-month period is more important than any single data point or any one data release. I would say employment data has continued to move in a positive direction. If there’s one other thing I’ve heard on this topic in the past few days, it’s that strong productivity-driven growth is not something we fear—it’s something we welcome. Thank you all very much.

Editor/Liam