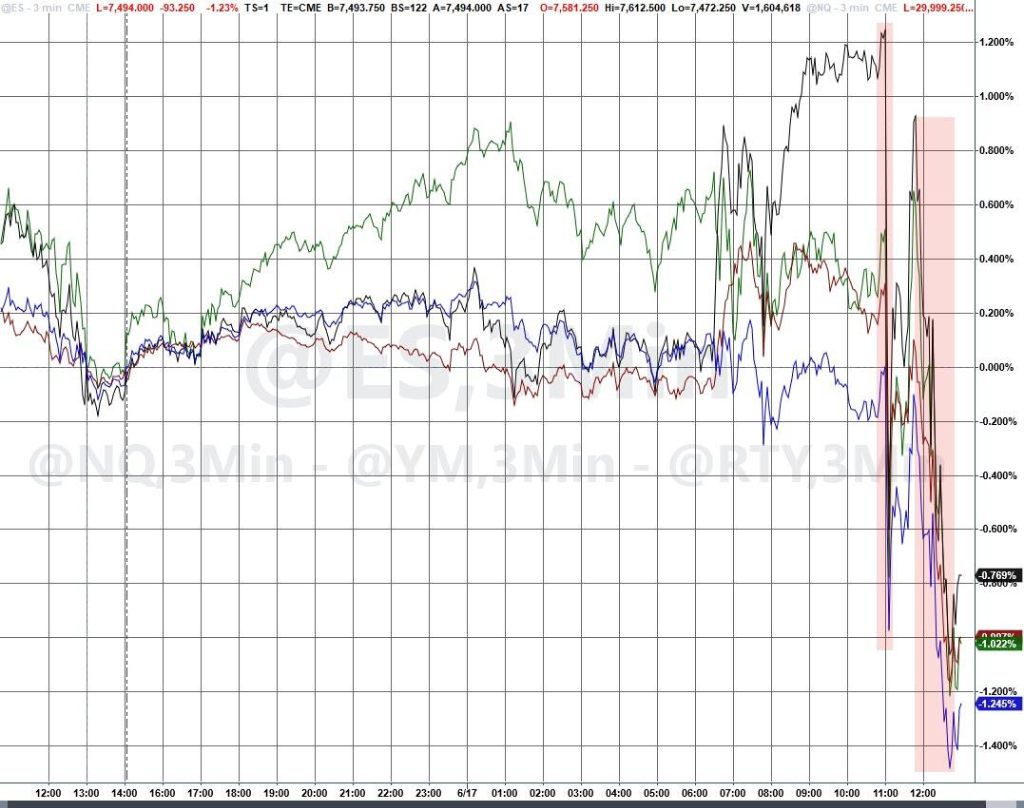

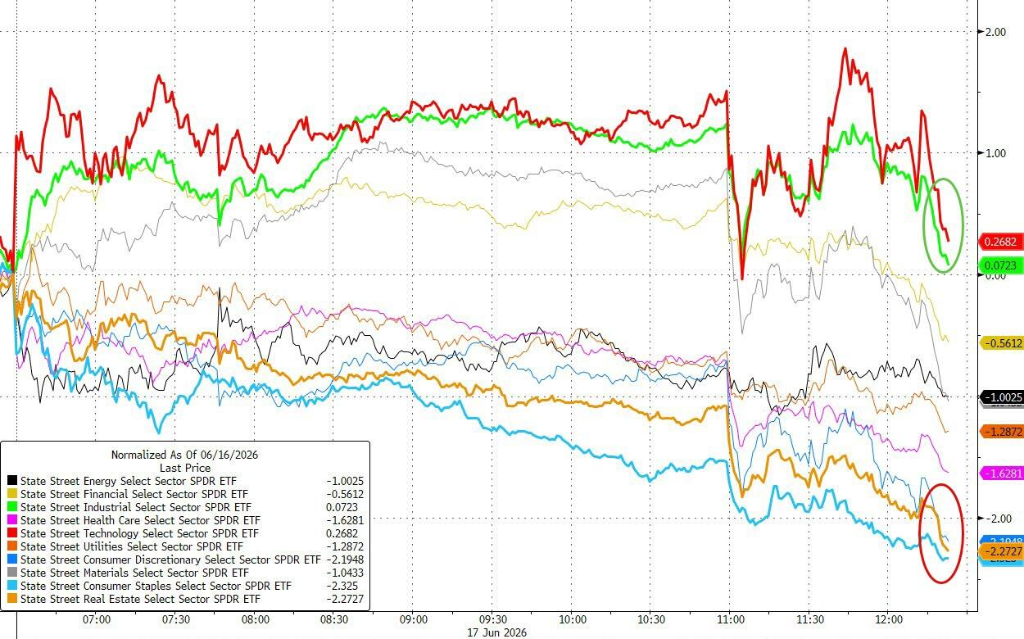

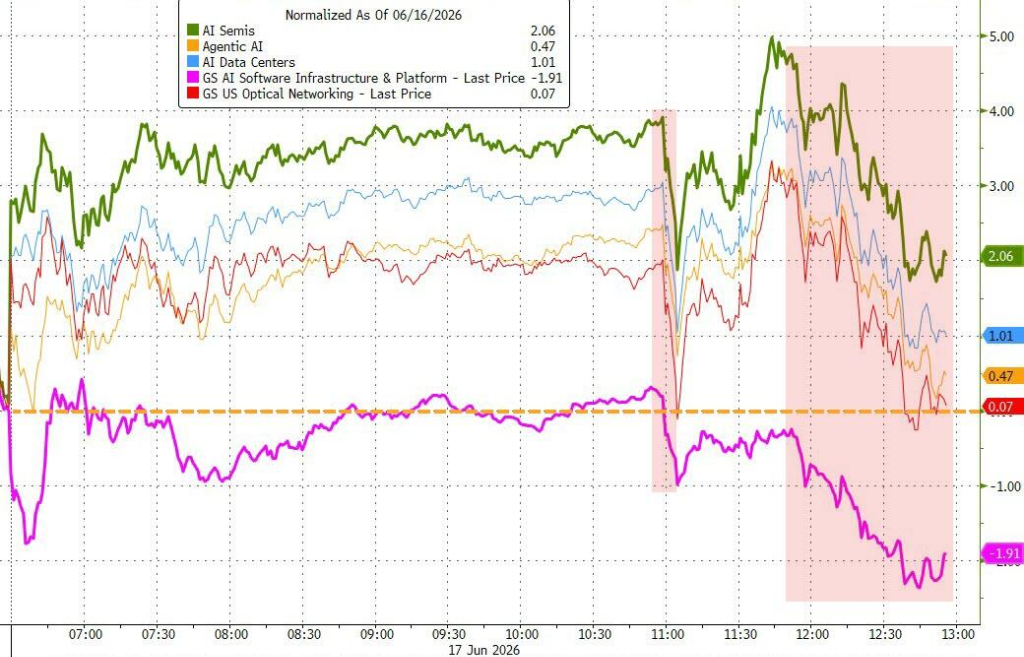

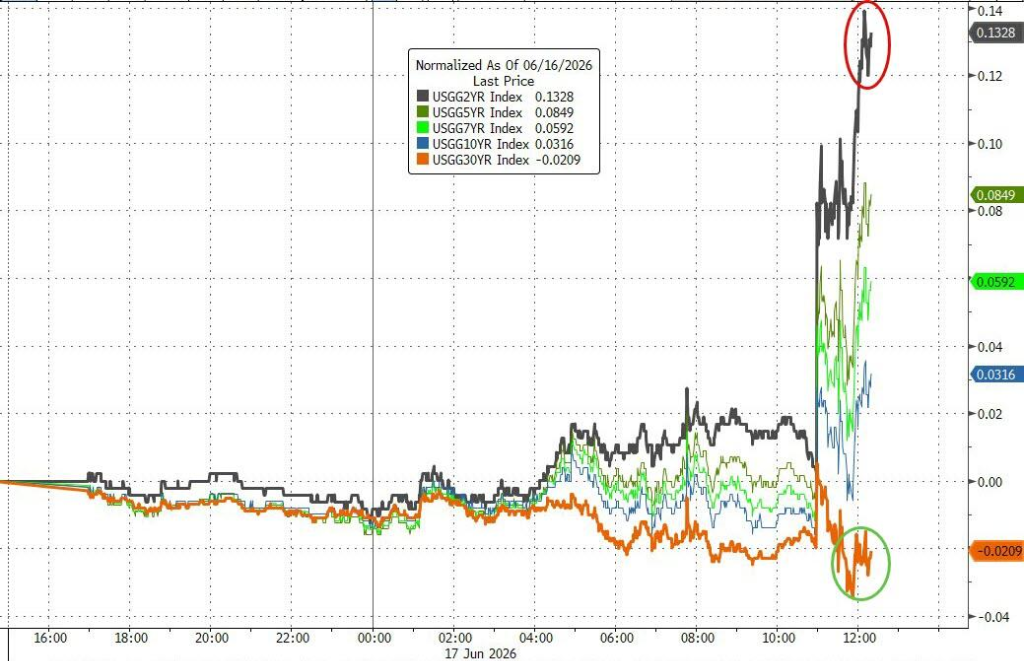

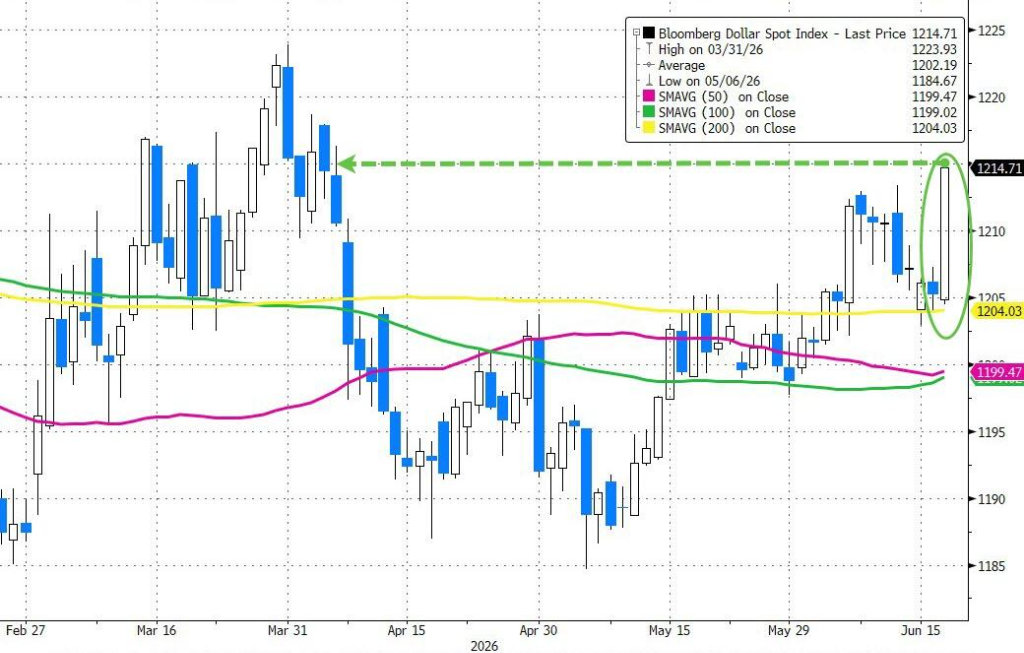

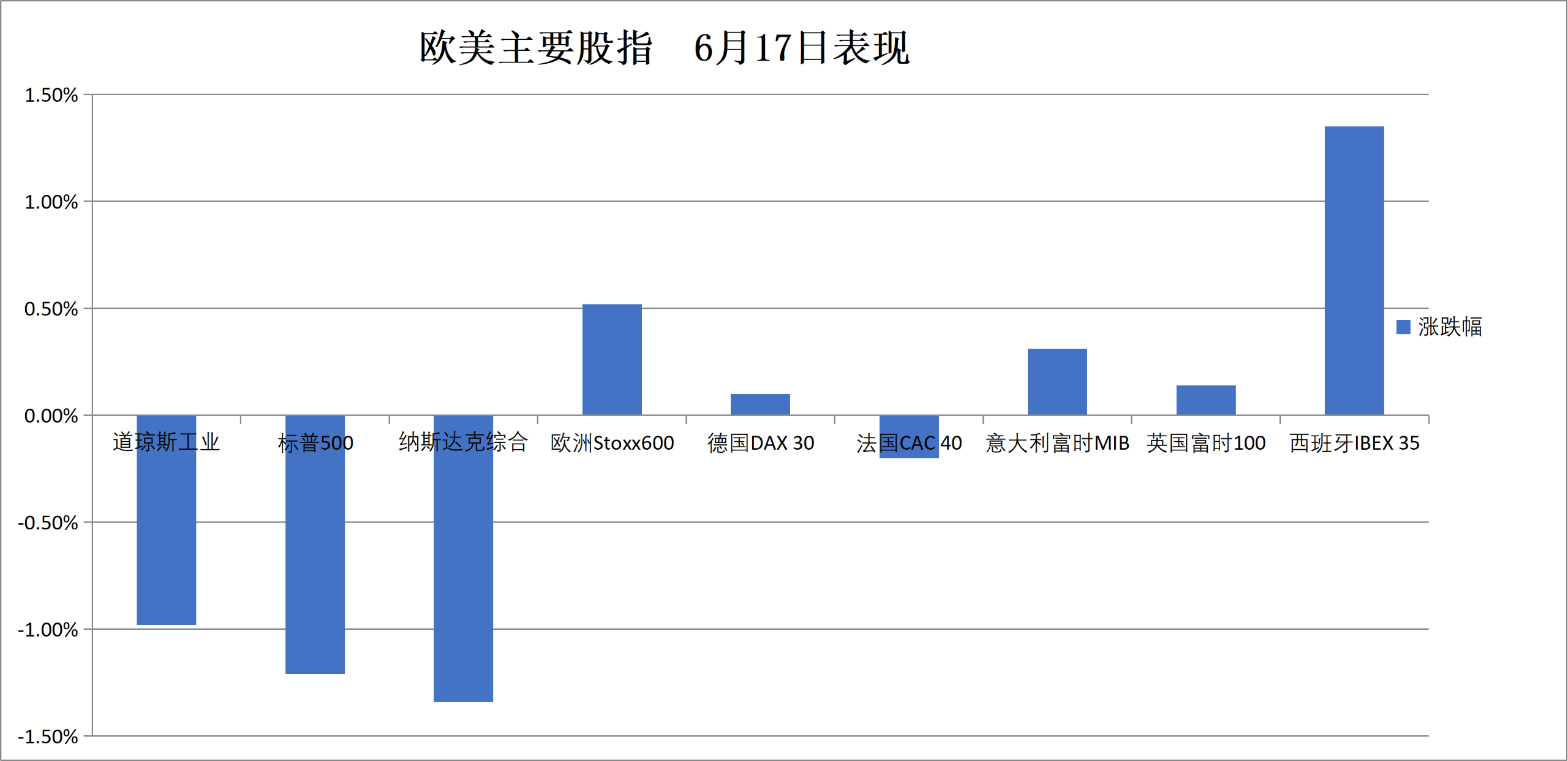

All three major U.S. stock indices closed lower, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average each declining by approximately 1% or more. Sector performance diverged, as defensive sectors (consumer staples and utilities) fell sharply, while technology and industrial sectors held up relatively better; AI-related semiconductors rose, but AI software stocks declined. The 2-year Treasury yield rose by 16 basis points to 4.21%, and the U.S. Dollar Index gained 0.8%. Gold prices dropped sharply, falling below $4,250 per ounce.

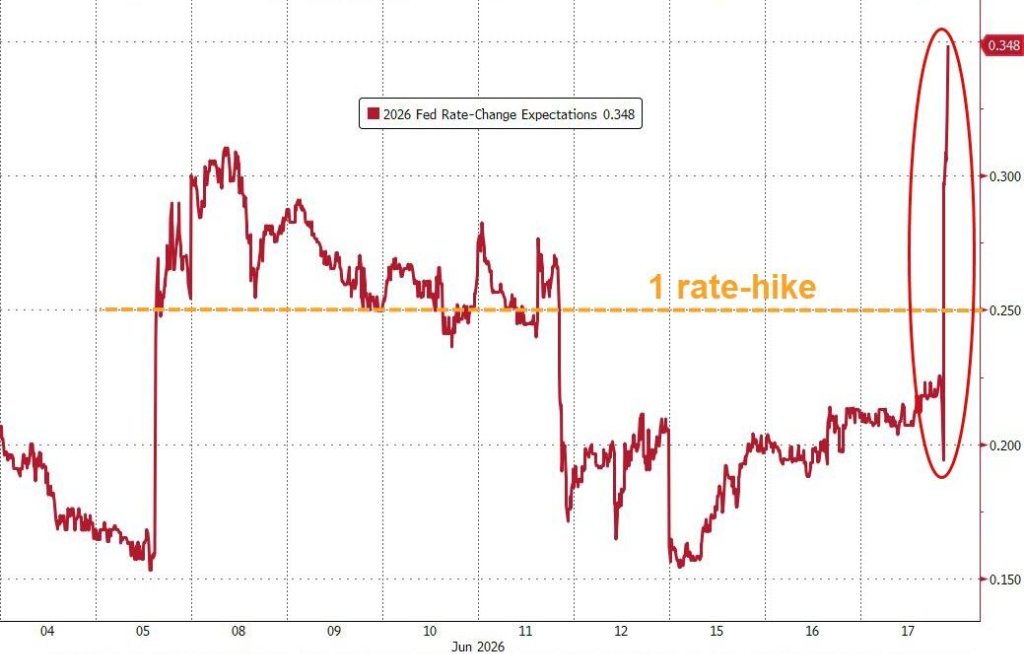

The Federal Reserve's dot plot showed a sharp increase in expectations for rate hikes this year, driving short-term U.S. Treasury yields and the dollar sharply higher, while U.S. equities, gold, and cryptocurrencies broadly declined. Crude oil ended flat overall after significant volatility.

On Wednesday local time, the Federal Reserve held rates steady, but the policy statement—led by new Chair Waller—took a markedly hawkish turn, catching markets off guard.

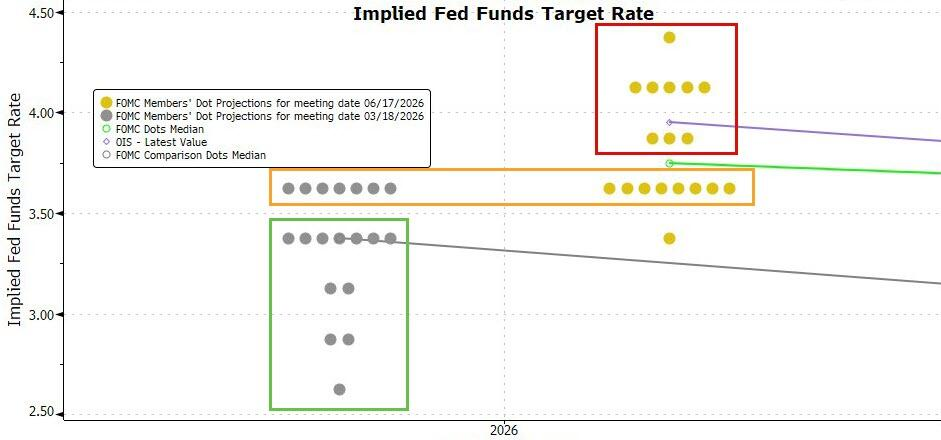

The dot plot indicated that nine officials expect at least one rate hike this year. The Fed also completely removed forward guidance, declaring 'price stability' as its primary objective.

The dot plot indicated that nine officials expect at least one rate hike this year. The Fed also completely removed forward guidance, declaring 'price stability' as its primary objective.

Notably, Waller himself did not submit a rate path projection, breaking with the precedent set by previous Fed chairs. He also announced the formation of a dedicated task force to review the Fed’s $6.7 trillion balance sheet and examine whether monetary policy transmission stems primarily from interest rate tools or balance sheet tools.

Following the meeting, money markets fully priced in one rate hike by October. The probability of unchanged rates for the remainder of the year plunged from 40% the previous day to 15.7%. The likelihood of a 25-basis-point hike by December rose to nearly 38%, while the probability of a 50-basis-point increase climbed to approximately 33%.

Bob Michele, Chief Investment Officer and Global Head of Fixed Income at JPMorgan Asset Management, stated:

Half of the committee members anticipate a rate hike this year—this is nothing short of a wake-up call for markets. I believe they are preparing to raise rates.

Impacted by this shock, all three major U.S. equity indices closed lower on Wednesday. The S&P 500 fell by approximately 1.2%, the Nasdaq declined by about 1.3%, and the Dow Jones Industrial Average dropped roughly 1%. $CBOE Volatility S&P 500 Index (.VIX.US)$ rose back above 18.

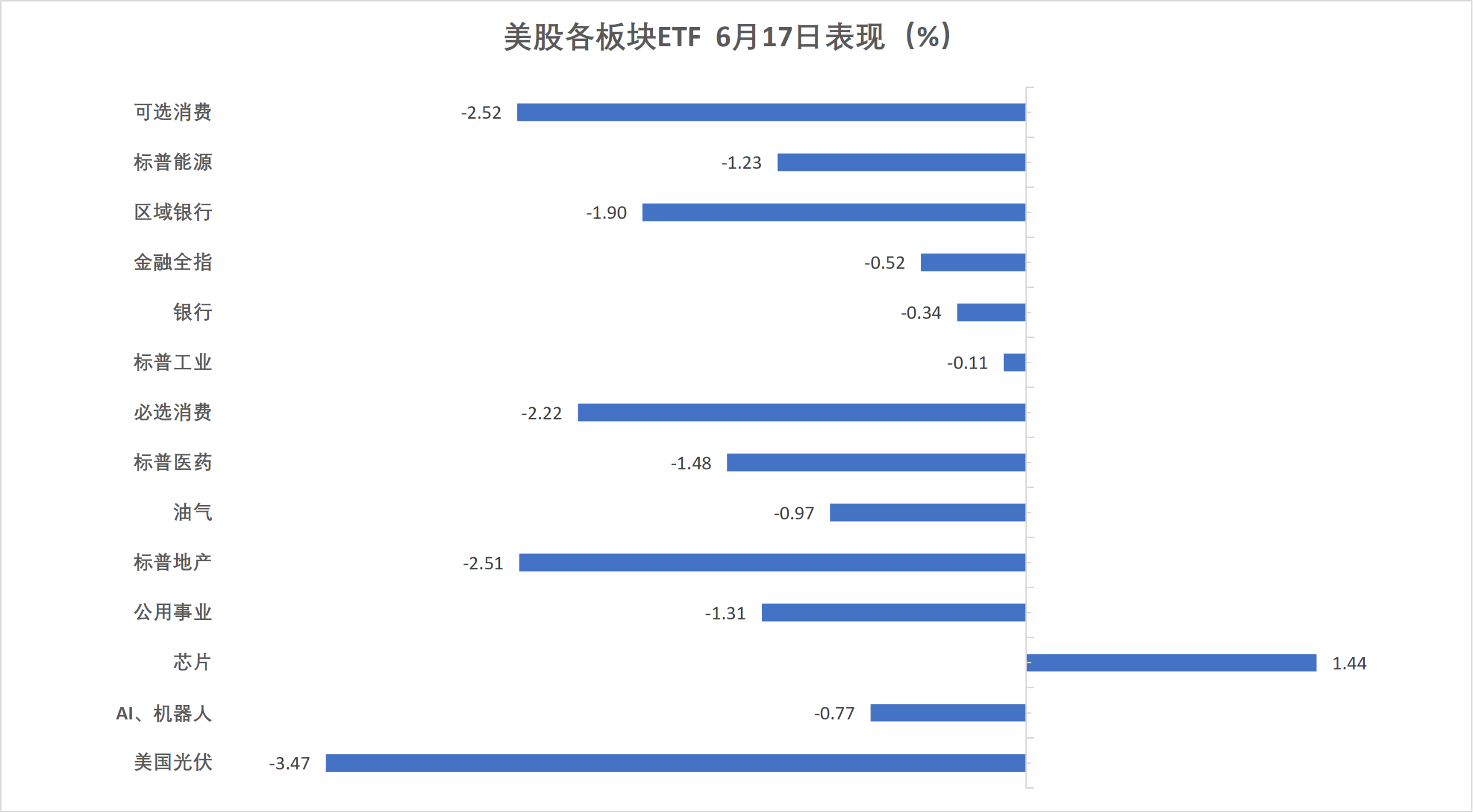

From a sectoral perspective, defensive sectors performed the worst, with consumer staples and utilities declining sharply as interest rates rose, while technology and industrial stocks held up relatively better.

Semiconductor stocks tied to artificial intelligence closed in positive territory, with the Philadelphia Semiconductor Index rising 182.848 points, or 1.38%, against the broader market trend; however, the AI software segment declined.

Notably, $SpaceX (SPCX.US)$ It recorded its first decline since listing, closing down nearly 5% today.

The Fed's hawkish signal directly impacted the short-end U.S. Treasury market, with the 2-year Treasury yield jumping approximately 13 to 16 basis points in a single day to around 4.21%, while the 30-year Treasury yield edged down by about 2 basis points. The spread between the 2-year and 30-year yields narrowed sharply to its flattest level in over a year.

Bret Kenwell of eToro noted:

The greater impact stemmed from interest rate projections. Although the market was somewhat prepared, the Fed’s dot plot indicated that policymakers were willing to maintain a hawkish stance for longer than investors had anticipated.

However, several analysts remained cautious about the actual path of rate hikes. Kay Haigh of Goldman Sachs Asset Management stated that although the Fed’s recent hawkish pivot was not solely driven by elevated energy prices, the base case scenario still narrowly avoids further rate hikes—but the margin for error is slim, making upcoming inflation data critically important.

Ellen Zentner of Morgan Stanley Wealth Management judged that:

Despite the more hawkish tone in the statement, the Fed’s next move could still be a rate cut, but it will require inflation to ease sufficiently to give the committee room to maneuver.

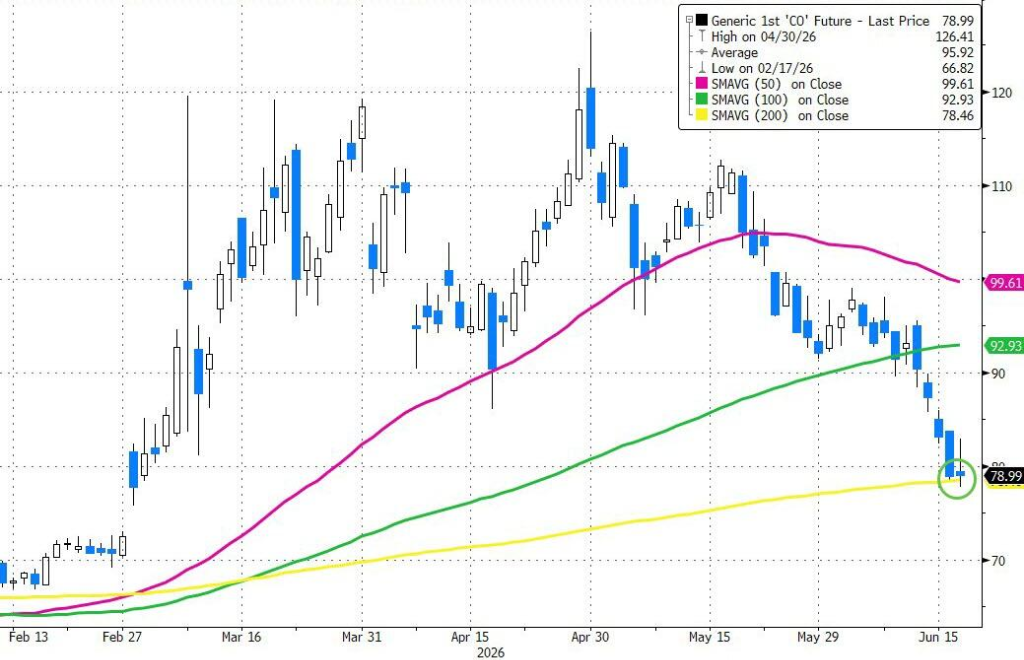

Compared to the impact from the Fed, oil markets on the day were more influenced by geopolitical headlines, though prices ultimately ended nearly flat, with WTI crude holding around $76 per barrel.

During the day, oil prices stabilized and rebounded after touching the 200-day moving average, bolstered by a significant drawdown in crude inventories reported by the U.S. Energy Information Administration (EIA), with stocks at the Cushing delivery hub falling to 'tank-bottom' levels, briefly lifting WTI prices.

However, prices then plunged sharply on reports of progress in U.S.-Iran talks, only to quickly rebound after Trump stated he would not rule out resuming military action if dissatisfied with the terms of any agreement, leading to repeated shifts between bullish and bearish sentiment.

Notably, prompt Brent crude—the most important benchmark for physical oil pricing—continued to decline, effectively erasing the war premium. Trump acknowledged that one reason he approved the memorandum of understanding was being informed that 'the U.S. Strategic Petroleum Reserve would be depleted in about four weeks.'

Driven by repricing of interest rate expectations, the U.S. dollar index strengthened significantly, with the Bloomberg Dollar Spot Index rising approximately 0.7%. The dollar climbed to around 1.1490 against the euro and 1.3281 against the pound, reaching its highest level in nearly two months.

Gold came under pressure and retreated, with spot gold prices falling roughly 1.9% to $4,247.93 per ounce, wiping out all gains accumulated earlier in the week on expectations of U.S.-Iran negotiations.

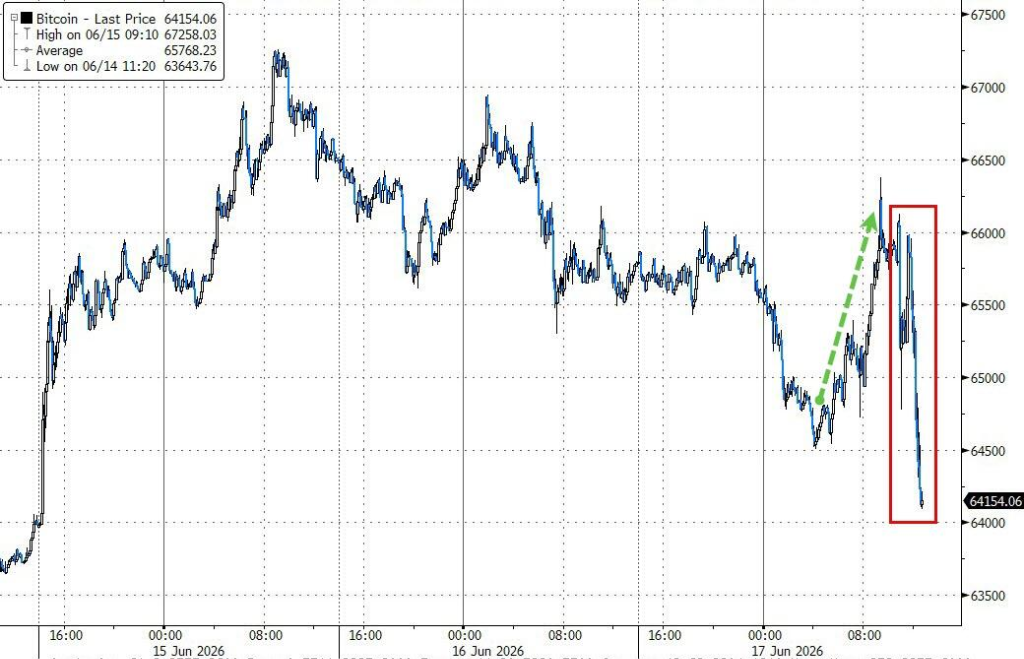

$Bitcoin (BTC.CC)$ Experienced sharp intraday volatility and ultimately closed down approximately 2.3% near $64,301, retreating below $64,500.support levelbelow.

On Wednesday, all three major U.S. equity indices declined, with the CBOE Volatility Index (VIX) closing up 12.31%, and sector ETFs across the U.S. stock market broadly ending lower.

U.S. benchmark indices:

The S&P 500 Index closed down 91.25 points, or 1.21%, at 7,420.10.

The Dow Jones Industrial Average closed down 507.12 points, or 0.98%, at 51,492.55.

The Nasdaq Composite closed down 354.688 points, or 1.35%, at 26,021.656. The Nasdaq 100 Index fell 297.181 points, or 0.99%, closing at 29,670.948.

Russell 2000 IndexClosed down 0.72% at 2,917.982 points.

The CBOE Volatility Index (VIX) closed up 12.31% at 18.43.

U.S. stock sector ETFs:

The Internet Stocks ETF fell 2.89%, while the Consumer Discretionary ETF and Consumer Staples ETF declined by as much as 2.51%; the Semiconductor ETF rose 1.29%.

Mag 7:

The Magnificent 7 index declined 2.38% to close at 210.21.

$Meta Platforms (META.US)$ fell 5.44%, $Microsoft (MSFT.US)$ fell 3.79%, $Amazon (AMZN.US)$ fell 3.46%, Alphabet Class A shares dropped 2.53%, and Tesla declined 2.05%, $NVIDIA (NVDA.US)$ fell 1.33%, and Apple dropped 1.10%.

Chip Stocks:

$PHLX Semiconductor Index (.SOX.US)$ rose 182.848 points, or 1.38%, to close at 13,477.072.

Taiwan Semiconductor ADR gained 1.48%, $Advanced Micro Devices (AMD.US)$ up 1.02%, $Broadcom (AVGO.US)$ 、 $Marvell Technology (MRVL.US)$ up 4%, $Intel (INTC.US)$ Rose more than 3%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 1.14% at 6,122.30.

Among popular Chinese ADRs, $Li Auto (LI.US)$ down 3.4%, $Alibaba (BABA.US)$ down 3.1%, Nio up 0.2%, and ASE Technology Holding up 2%.

Other individual stocks:

$Circle (CRCL.US)$ up 1.24%.

The eurozone blue-chip index extended its record closing highs for a fourth consecutive session ahead of the Federal Reserve’s policy statement, with component BMW dropping more than 8.3%. The Dutch stock market closed up nearly 1.2%, alongside Italian and Spanish indices, which also hit record closing highs.

Pan-European Index:

The STOXX Europe 600 Index closed up 0.52% at 639.31, marking its third consecutive record closing high and posting a cumulative gain of 3.42% since June 11.

The Eurozone STOXX 50 Index rose 0.68% to close at 6,300.07 points, marking its fourth consecutive day of record closing highs.

Major Stock Indexes Around the World:

The German DAX 30 Index gained 0.10% to close at 24,934.67 points.

The French CAC 40 Index declined 0.20% to close at 8,430.79 points.

The UK FTSE 100 Index advanced 0.14% to close at 10,508.61 points.

Sector and individual stock performance:

Among Eurozone blue-chip stocks, Bayer rose 4.80%, ASML Holding gained 4.10%, Siemens Energy increased by 3.60% (ranking third), Deutsche Bank climbed 2.45%, and UniCredit advanced 2.43%.

Among all constituents of the STOXX Europe 600 Index, Straumann Holding surged 10.80%, Auto1 Group rose 8.35%, Endesa gained 6.82%, Aixtron SE increased by 6.72%, and ASM International advanced 5.89% (ranking fifth).

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen