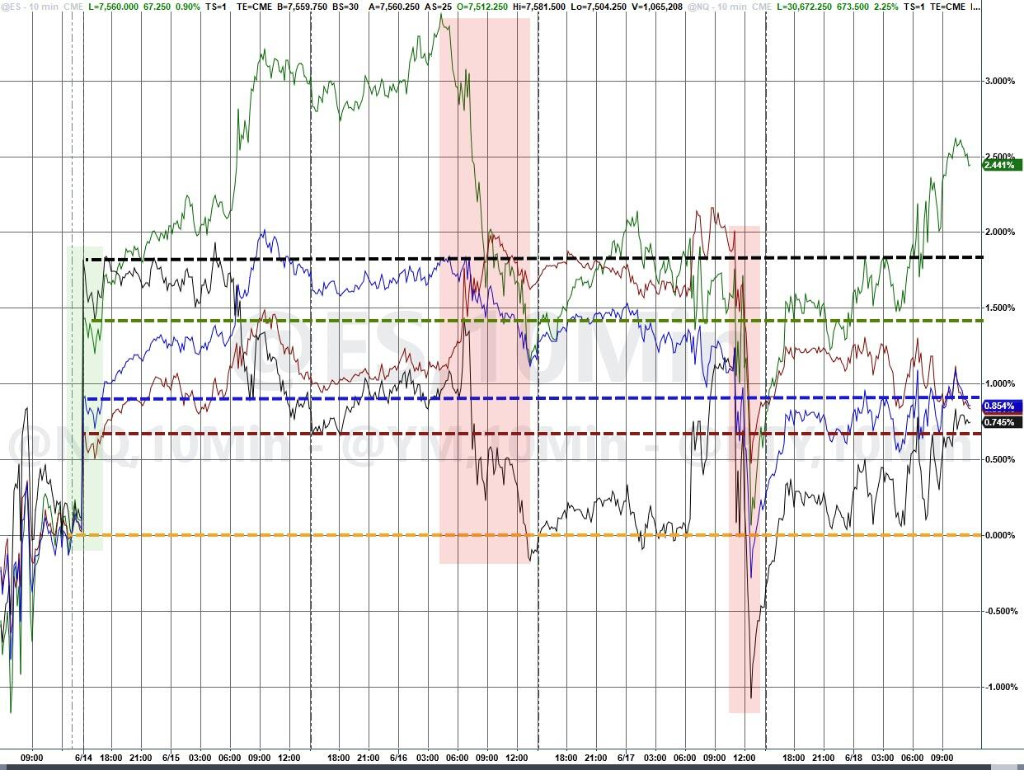

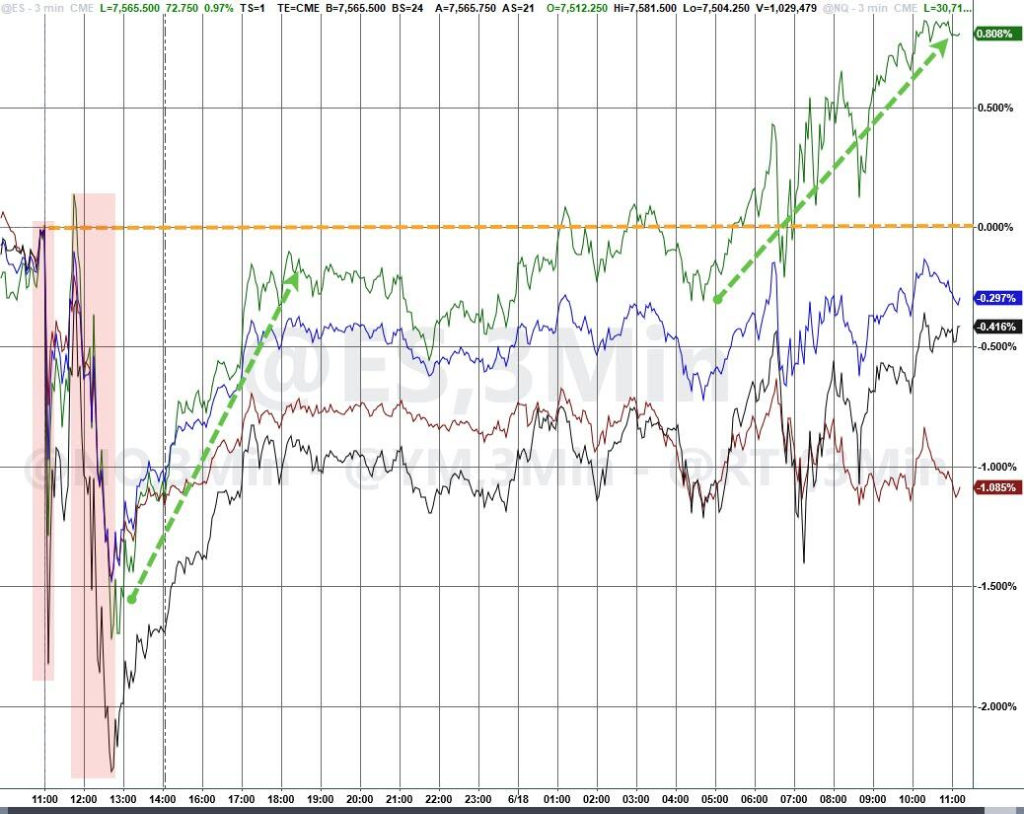

On Thursday, the S&P 500 rose by 1.1%, and the Nasdaq 100 gained 2.5%. U.S. markets were closed on Friday for the Juneteenth holiday, making this a shortened trading week. The Nasdaq was ultimately the only major index to fully recover its losses triggered by Chair Powell's hawkish remarks. Chip stocks led the rally, with the Philadelphia Semiconductor Index surging 6.4% in a single day. European equities pulled back from record highs, while the Eurozone blue-chip index continued to reach new all-time highs.

The U.S.-Iran peace agreement has reopened shipping through the Strait of Hormuz, driving both U.S. equities and Treasury bonds higher, though market concerns over a potential Federal Reserve policy pivot remain unresolved, keeping short-end rates under persistent pressure.

Following the entry into force of the interim U.S.-Iran peace agreement, multiple supertankers have traversed the Strait of Hormuz. Anticipated restoration of crude oil supply has exerted downward pressure on energy prices, narrowing inflation risk premiums.

According to CCTV, on Thursday, April 18, Eastern Time, U.S. Vice President Vance announced at a White House press briefing that the 60-day negotiation window stipulated in the Memorandum of Understanding (MoU) signed by U.S. President Trump and Iranian President Pezeshkian on Wednesday has officially commenced.

According to CCTV, on Thursday, April 18, Eastern Time, U.S. Vice President Vance announced at a White House press briefing that the 60-day negotiation window stipulated in the Memorandum of Understanding (MoU) signed by U.S. President Trump and Iranian President Pezeshkian on Wednesday has officially commenced.

The Trump administration announced that U.S. forces have lifted all maritime blockades against Iran. Within hours of the agreement’s signing, three Saudi-flagged supertankers passed through the Strait of Hormuz, marking the first resumption of transit through this critical global energy corridor since it was closed during hostilities.

Trump immediately posted on Truth Social:

Oil is flowing, Iran will never have nuclear weapons, and the stock market is roaring.

U.S. Vice President Vance downplayed external concerns that Iran might impose tolls on transiting vessels. Following the agreement’s implementation, WTI crude futures settled at $76.60 per barrel—the lowest level since before the outbreak of the Iran conflict—recording the steepest weekly decline in nearly two months.

Ian Lyngen of BMO Capital Markets stated:

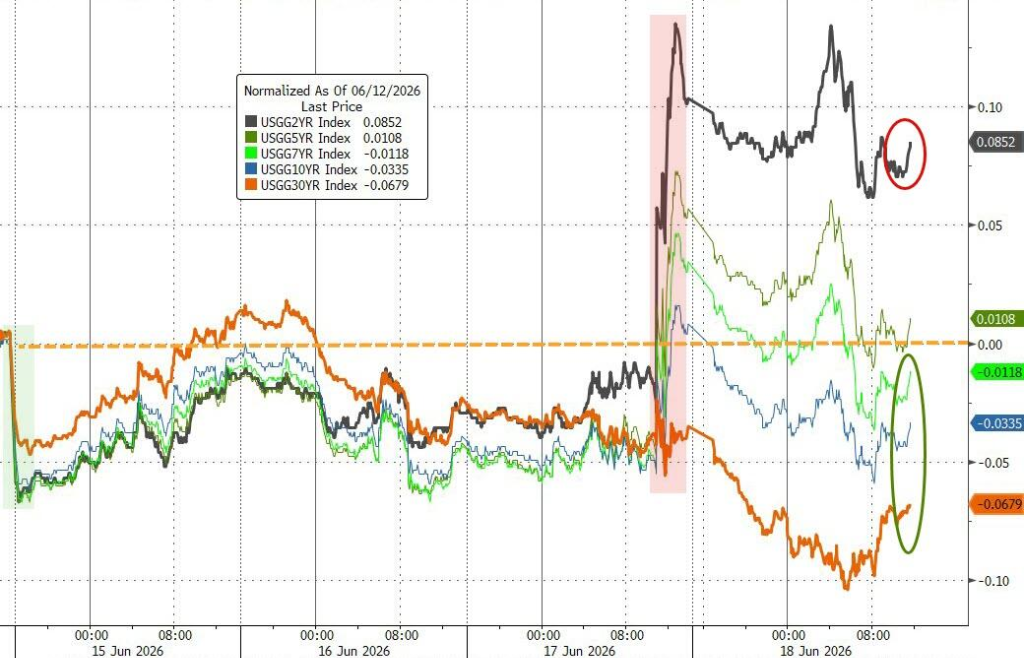

Improved prospects for Persian Gulf oil supply have supported equity prices, while lower energy costs have alleviated forward-looking inflation expectations, contributing to a meaningful decline in long-end U.S. Treasury yields.

Fawad Razaqzada of Forex.com believes that if lower energy costs continue to feed into inflation data, policymakers may ultimately find sufficient justification to hold rates steady rather than hike. Fawad Razaqzada said:

My assessment is that inflation should gradually moderate over the coming months, which may allow the Federal Reserve to maintain its current policy stance without implementing another round of tightening.

The disinflationary effect from falling oil prices has partially offset pressure on the Fed to pivot its policy. Long-end yields have declined alongside lower oil prices, while short-end rates continue to face significant upward pressure.

The 10-year U.S. Treasury yield fell by 3 basis points to 4.45%, partially absorbing the hawkish shock delivered overnight by Fed Chair Waller.

Bloomberg analyst Simon White noted that excess liquidity has turned negative for the first time since 2021 and continues to decline, creating an increasingly strong headwind for equities as financial conditions are clearly tightening.

On Thursday, the S&P 500 rose 1.1%, while the Nasdaq 100 gained 2.5%, led by semiconductor stocks, $PHLX Semiconductor Index (.SOX.US)$ surging 6.4% in a single day. Trading volume on U.S. exchanges soared to a record high, driven by over $7.5 trillion in options expiring that day.

Notably, with U.S. markets closed on Friday for the Juneteenth holiday, this week was shortened, and the Nasdaq was the only major index to fully recover all losses triggered by Waller’s hawkish remarks.

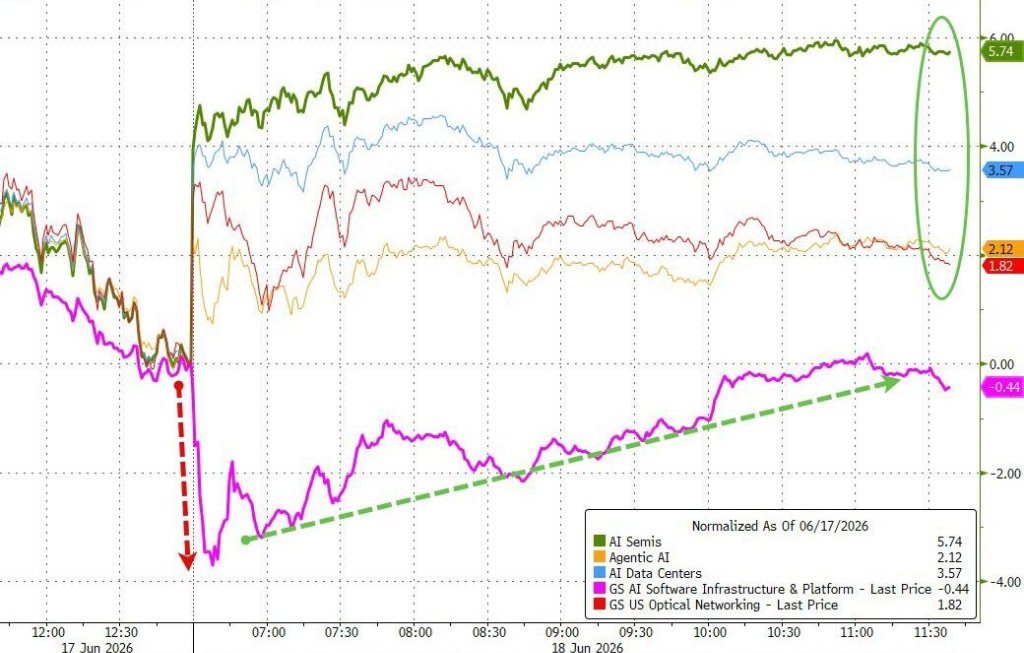

Artificial intelligence once again dominated market sentiment today, with bargain hunters rushing in—particularly in the semiconductor sector. Even AI software stocks, which opened weakly, saw nearly uninterrupted buying interest throughout the day.

At the individual stock level, $SpaceX (SPCX.US)$ shares declined for the second consecutive day following their listing, though the stock price remains well above its IPO offering price.

Chip stocks rose collectively, $SanDisk (SNDK.US)$ 、 $Intel (INTC.US)$ 、 $Micron Technology (MU.US)$ 、 $Taiwan Semiconductor (TSM.US)$ , Western Digital, Applied Materials, $ASML Holding (ASML.US)$ closed at a record high.

Specifically, the Philadelphia Semiconductor Index rose 6.42%, SanDisk gained over 11%, Intel rose more than 10%, Micron Technology climbed over 8%, Taiwan Semiconductor and Qualcomm each advanced over 6%, NXP Semiconductors rose over 5%, and ARM, Broadcom, Western Digital, Applied Materials, and AMD all gained over 4%, while ASML Holding increased by over 3%, $NVIDIA (NVDA.US)$ rose 2.95%.

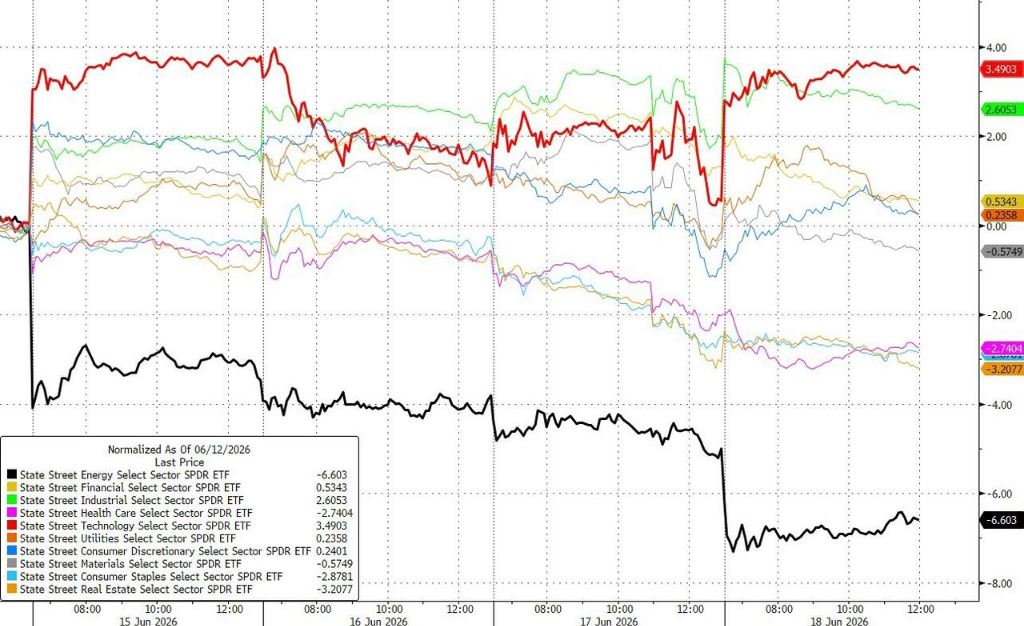

Technology stocks led gains this week, with the industrial sector also showing strength, while energy stocks were the weakest performers.

Goldman Sachs partner Bobby Molavi succinctly characterized the current market landscape: the market remains narrow and concentrated, driven by a single factor (momentum) and a single theme (AI computing power and storage), and continues to overcome various challenges it encounters.

He also cautioned that corporate attitudes toward AI investment are quietly shifting from 'cost-insensitive experimentation' to 'ROI-focused prudence,' which may signal the end of the era of 'token maximization.'

The U.S. Dollar Index recorded its largest two-day gain in three months, surging sharply after a strong rebound from its 200-day moving average.

The dollar's strength was primarily driven by a sharp depreciation of the yen, with USD/JPY breaking above the 161 level, prompting Japanese officials to issue warnings of potential intervention.

$XAU/USD (XAUUSD.CFD)$ Prices fell by 0.9% to $4,216.58 per ounce, $Bitcoin (BTC.CC)$ dropping 1.9% to $63,124.21, with both failing to follow the equity market rebound and remaining under pressure amid a stronger U.S. dollar.

European equities retreated from record highs, while the Eurozone blue-chip index continued to reach new closing records. Italian equities and the banking sector posted fresh all-time closing highs, while the UK benchmark index declined by 1% and defense ETFs dropped more than 2.7%.

Pan-European Index:

The STOXX Europe 600 Index closed down 0.34% at 637.14 points, ending a streak of five consecutive trading days of gains and three straight days of record closing highs.

The EURO STOXX 50 Index rose 0.37% to close at 6,323.27 points, marking its fifth consecutive day of record closing highs and posting a cumulative gain of 5.21% over the past six trading days.

Major Stock Indexes Around the World:

Germany's DAX 30 Index gained 0.37% to close at 25,026.80 points.

France's CAC 40 Index advanced 0.44% to close at 8,467.98 points.

The FTSE 100 Index in the UK closed down 1.04% at 10,399.70 points, opening lower and trending downward throughout the session.

Sector and individual stock performance:

Among Eurozone blue chips, Infineon rose 6.42%, Siemens Energy gained 4.70%, and Safran, Schneider Electric, Adidas, Airbus (Paris-listed), and Hermès posted gains ranging from 2.05% to 2.92%, placing them among the top seven best performers.

Among all constituents of the STOXX Europe 600 Index, Capgemini Consulting fell 8.87%, Sacyr dropped 7.34%, Hochschild Mining declined 7.29%, the London Stock Exchange ranked as the fourth-largest decliner, and Kering Group rose 4.40%.

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Stephen