The U.S. and Iran signed a framework agreement and reopened the Strait, driving Brent crude below $77 per barrel. However, analysts warned of a divergence between financial markets’ expectations of resumed production and the actual tightness in supply: global inventories continue to decline sharply, while freight rates have tripled and shipowners’ caution is creating logistical bottlenecks. Although markets have already priced out the geopolitical risk premium, actual supply recovery will still take time.

$Brent Last Day Financial Futures (AUG6) (BZmain.US)$This week, prices fell below $77 per barrel, nearly erasing all the geopolitical premium accumulated since the outbreak of the Iran war and hitting their lowest level since hostilities began. However, several analysts have warned that futures markets are pricing in a supply recovery that has not yet materialized, creating a significant divergence between financial market optimism and the realities of the physical crude oil market.

On Wednesday evening, the U.S. and Iran signed a 14-point framework memorandum of understanding. The U.S. Central Command immediately confirmed it had lifted the blockade on the Strait of Hormuz, with reports emerging of tankers transiting the waterway. Brent crude briefly dropped to $76.54 per barrel intraday before rebounding slightly to close at $79.85. WTI declined 0.2% to settle at $75.85, marking its lowest level since the conflict began. The U.S. national average retail gasoline price subsequently dipped below $4 per gallon, falling to $3.999—still approximately $1 higher than pre-conflict levels.

Since peaking above $100 per barrel in May, Brent has posted a cumulative decline of over 25%, as markets rapidly priced in expectations of a large volume of Middle Eastern crude returning to global markets. Yet, fundamental realities remain far more complex than market pricing suggests—from the absence of shipping insurance and tanker freight rates still triple their pre-conflict levels, to the International Energy Agency’s (IEA) estimate that global inventories continue to draw down at nearly 4 million barrels per day.

Since peaking above $100 per barrel in May, Brent has posted a cumulative decline of over 25%, as markets rapidly priced in expectations of a large volume of Middle Eastern crude returning to global markets. Yet, fundamental realities remain far more complex than market pricing suggests—from the absence of shipping insurance and tanker freight rates still triple their pre-conflict levels, to the International Energy Agency’s (IEA) estimate that global inventories continue to draw down at nearly 4 million barrels per day.

This race between financial markets and physical markets has become the central point of divergence in current oil price dynamics. Analysts at multiple institutions believe the recent sell-off carries risks of overshooting, though others argue that expectations of eased sanctions on Iran have not yet been fully priced in—and if formally confirmed, could exert further downward pressure on prices.

Hormuz Reopens; Sentiment Drives the Sell-Off

The immediate trigger for this sharp drop in oil prices was the signing of the U.S.-Iran memorandum of understanding. Under the agreement framework, Tehran will reopen the Strait of Hormuz—a critical chokepoint that normally handles roughly one-fifth of global daily oil trade—in exchange for Washington lifting its blockade on Iranian ports and sanctions on oil exports, and opening a 60-day window for nuclear deal negotiations. Iran also pledged never to develop or acquire nuclear weapons.

Markets reacted instantly: sell first, ask questions later. Trump declared prominently on Truth Social: "Oil is flowing… markets are roaring… you’re welcome!"

In a research report, Goldman Sachs analyst Yulia Zhestkova Grigsby estimated that Persian Gulf oil exports could return to pre-conflict levels by the end of July, while noting that full recovery still faces several hurdles. Navin Das, Senior Crude Oil Analyst at Kpler, added that the post-agreement decline in oil prices reflects a limited unwinding of geopolitical risk premiums embedded in the forward curve, combined with market expectations of restored flows through Hormuz, jointly pressuring spot prices.

Shipping Markets Remain Skeptical: Freight Rates Still Triple Pre-Conflict Levels

Yet, in stark contrast to the optimism in futures markets, shipping markets have so far failed to reflect this expectation of peace.

It was reported that Sinopec attempted this week to charter a very large crude carrier (VLCC) to load Iraqi crude for delivery between June 25 and 30, receiving six bids—all at freight rates nearly triple pre-war levels—yet ultimately failed to secure a deal. PetroChina directly articulated the core issue: "There are tankers available, but they’re too expensive, and there’s no guarantee you can pass through the Strait." Meanwhile, Indian Oil received zero bids for its tender issued for the same period; Sinochem is still searching for vessels.

Nader Itayim, Gulf and Middle East markets editor at Argus Media, noted that market optimism regarding the agreement’s impact may have overstated both its scale and the speed at which supply will normalize. "Although there is oil awaiting export in the Gulf Cooperation Council region, the additional supply may not materialize immediately," he stated. "Logistical bottlenecks must still be overcome before flows return to normal levels."

Goldman Sachs analyst Yulia Zhestkova Grigsby also wrote in a report that many shipowners remain cautious about transit guidance, with shippers’ risk aversion acting as a potential constraint. Additionally, Iran’s geopolitical objectives during the upcoming 60-day nuclear deal negotiations contribute further uncertainty.

Inventory data issues a warning: fundamentals do not support optimism

The fundamentals of the physical crude oil market have drawn a clear cautionary line against this sharp price decline.

The IEA estimates that global inventories have been depleting at a rate of nearly 4 million barrels per day since late February, when hostilities erupted. U.S. crude inventories have declined by more than 50 million barrels over the past nine weeks, with stockpiles at the Cushing storage hub hovering near what most analysts consider the operational floor. Countries that have been drawing down strategic and commercial reserves for months will ultimately need to replenish them.

According to the Brent futures curve, oil prices are not expected to fall back to pre-war lows—around $70 per barrel—until March 2031, highlighting a significant divergence from the aggressive pricing currently embedded in futures markets.

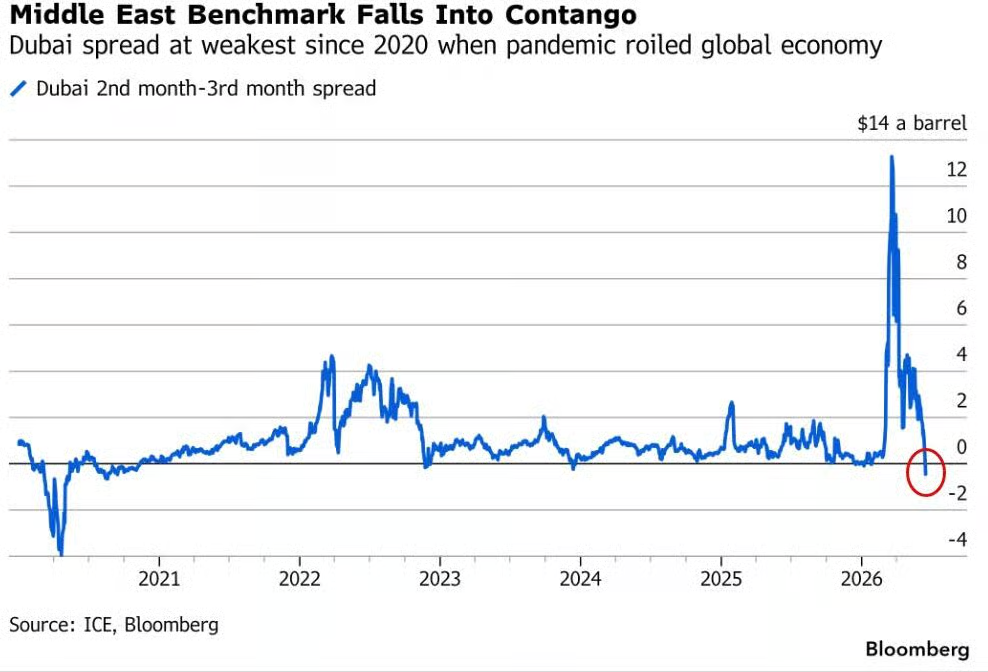

Bloomberg also pointed out that if Hormuz flows were to resume substantially, Asian markets would face another layer of pressure: Asian refiners had already substituted disrupted Middle Eastern crude with U.S. and other alternative sources, partially cutting processing rates, and now confront a sudden influx of Persian Gulf crude. This has already flipped the Middle Eastern crude futures curve into a bearish contango structure, with the market pricing in near-term oversupply rather than shortage.

Uncertainty remains over the agreement framework itself

Beyond the pace of supply restoration, the text of the agreement itself contains several ambiguities, adding further uncertainty to the market.

The memorandum of understanding stipulates that commercial vessels will be exempt from transit fees 'only for a period of 60 days,' yet Trump told the media that the strait would remain 'open free of charge' beyond those 60 days—a statement not included in the official text of the agreement. Itayim also emphasized that this agreement is not a comprehensive peace arrangement on which markets can fully rely, but rather a temporary framework aimed at de-escalating tensions and opening a window for subsequent negotiations; consequently, markets will continue to price in a certain risk premium.

Kpler analyst Navin Das highlighted another angle: the far end of the price curve has already begun partially reflecting the possibility of eased sanctions on Iran, though this factor has not yet been fully priced in—if formal confirmation of sanctions relief follows the conclusion of the 60-day negotiation window, oil prices could face further downward pressure.

Multiple analyses converge on the same core contradiction: financial markets have treated the signing of the agreement as a signal and have rapidly and fully priced in expectations of supply restoration, whereas physical markets—including shipping insurance, tanker scheduling, mine clearance in production zones, and restart of operations—follow an entirely different timeline. Currently, markets are trading this preliminary framework agreement as if it were a finalized production resumption plan, while physical markets are still waiting to see it actually implemented.

Editor/melody