Market Snapshot

As of the time of writing, the three major U.S. stock index futures were trading higher in pre-market hours. Dow Jones Industrial Average futures rose 0.27%, S&P 500 futures gained 0.47%, and Nasdaq 100 futures climbed 0.76%.

$Star Tech Companies (LIST2518.US)$ Most stocks rose in pre-market trading, with Micron Technology up over 4% and Qualcomm rising nearly 3%.

$China Concept Stocks (LIST2517.US)$ Most stocks rose in pre-market trading, with GDS Holdings up over 4% and United Microelectronics Corporation (UMC) rising nearly 2%.

Individual Stock News

AST SpaceMobile announced it has scheduled the launch of its BlueBird 8, 9, and 10 satellites.

AST SpaceMobile announced it has scheduled the launch of its BlueBird 8, 9, and 10 satellites.

Palantir faces intense scrutiny in the UK! Labeled an 'unacceptable risk,' its $440 million contract with the National Health Service (NHS) may be terminated.

The UK is conducting a comprehensive review of the contract signed between U.S. data analytics firm Palantir and the National Health Service (NHS). $Palantir (PLTR.US)$ The contract with the UK’s National Health Service (NHS) is undergoing a comprehensive review. Under mounting political pressure, the UK government is being urged to activate the termination clause when the initial contract period ends in early 2027.

The contract, awarded to Palantir in 2023, aims to build a platform connecting NHS healthcare data. It runs until early 2027, at which point the UK government must decide whether to renew it. On Tuesday, UK Minister for Tech Liz Kendall stated that the review will assess whether to extend the £330 million (approximately USD 441 million) agreement under its existing terms. According to those terms, the UK government may either extend the contract by up to seven years or terminate it outright.

In an interview, Liz Kendall said, 'The current Secretary of State for Health is reviewing every aspect of this contract to ensure we secure the best possible deal for the UK.' She cited concerns regarding patient privacy protection, public trust, and reliance on a U.S.-based vendor.

Rumors suggest Swiss regulators are softening their stance: UBS Group's capital requirement could be reduced from 100% to 70%, alleviating a multi-billion-dollar burden.

According to foreign media reports citing informed sources, Swiss lawmakers are considering a new proposal to ease capital requirements for $UBS Group (UBS.US)$ UBS Group. If implemented, this proposal would reduce UBS’s capital burden by several billion dollars compared to the government’s submitted draft.

The legislative draft submitted to parliament in April aimed to introduce stricter rules to prevent a repeat of the Credit Suisse collapse. It required UBS Group to fully back its overseas subsidiaries with Common Equity Tier 1 (CET1) capital.

Since its acquisition of the collapsed Credit Suisse in 2023—leaving it as Switzerland’s sole globally systemically important bank—UBS Group has criticized the proposed regulatory framework as “excessively stringent.”

Four individuals familiar with the discussions revealed that under the new proposal, UBS Group would need to support its overseas subsidiaries with approximately 70% to 80% CET1 capital, rather than the 100% mandated by the government.

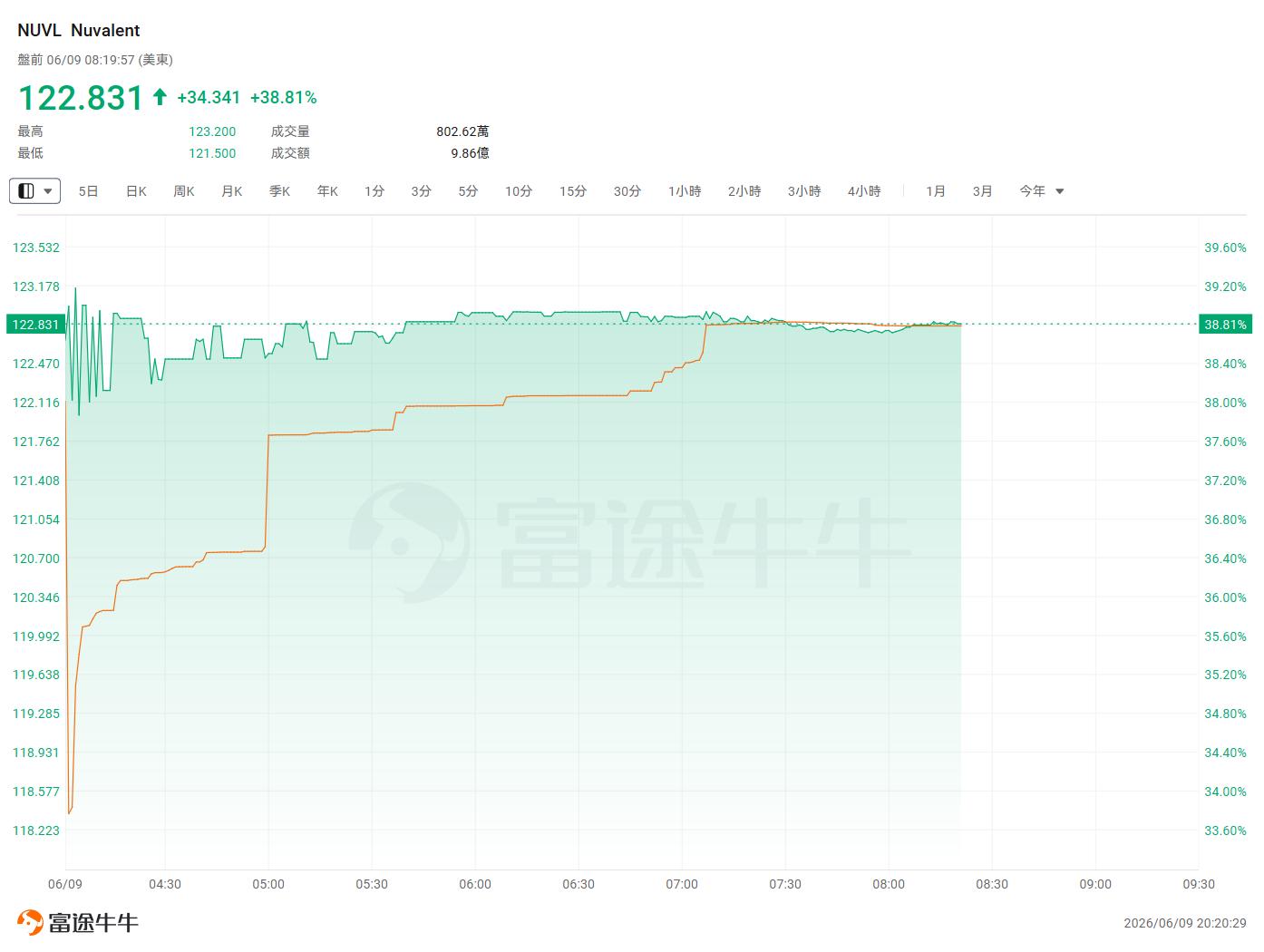

GlaxoSmithKline plans to acquire Nuvalent for $10.6 billion at a 40% premium, strengthening its position in the oncology drug sector.

GlaxoSmithKline (GSK.US) agreed to acquire an oncology therapeutics company for $10.6 billion. $Nuvalent (NUVL.US)$ In a statement released on Tuesday, GlaxoSmithKline said it would acquire Nuvalent for $124 per share in cash, representing a 40% premium over the Cambridge, Massachusetts-based company's closing share price on Monday.

The acquisition marks a significant expansion of GlaxoSmithKline’s oncology business. Since the British pharmaceutical company re-entered the oncology field in 2019, its cancer drug portfolio has been steadily growing. This transaction also represents the first major acquisition under CEO Luke Miels.

Since taking office earlier this year, Miels has been focused on revitalizing GlaxoSmithKline, a company long perceived as risk-averse and struggling to alleviate investor concerns about its pipeline of investigational drugs.

Bubble burst or 'golden pit'? Mizuho endorses storage stocks like SanDisk, betting AI chip demand will surge eightfold by 2028.

Mizuho Securities raised the target price for $SanDisk (SNDK.US)$ 、 $Seagate Technology (STX.US)$and$Western Digital (WDC.US)$ , as the firm believes artificial intelligence (AI) will continue to cause supply-demand imbalances in the memory market.

Mizuho raised SanDisk’s price target from USD 1,825 to USD 2,200; Seagate’s from USD 875 to USD 1,090; and Western Digital’s from USD 550 to USD 685, while maintaining an “outperform” rating on all three stocks.

Additionally, the firm also highlighted the upside potential of $Broadcom (AVGO.US)$and$Micron Technology (MU.US)$ .

The analyst team led by Vijay Rakesh stated: “We continue to view AI as the key driver behind the supply-demand imbalance in the memory market, as we observe mounting demand in our fiscal 2027/28 forecast period that could place further strain on the market. We continue to expect DRAM wafer starts in fiscal 2026/27 to increase by 10% and 6% year-over-year, respectively, driven indirectly by rising HBM demand. However, we also note that high HBM yield loss rates may constrain growth, while demand is projected to rise by 27% and 24% year-over-year, respectively. In NAND flash, we see enterprise solid-state drives (eSSDs) as the primary demand driver, with total NAND demand expected to grow by 18% and 18% year-over-year in fiscal 2026/27, respectively. Wafer starts are projected to decline by 5% in fiscal 2026 and increase by 3% in fiscal 2027, as we anticipate no significant visible supply additions until fiscal 2028.”

Apple's AI strategy diverges from Silicon Valley's capital-intensive playbook: it pairs in-house models with dual infrastructure from NVIDIA and Google, prioritizing privacy as its key differentiator.

Monday, $Apple (AAPL.US)$ disclosed its progress in artificial intelligence research and development at its annual Worldwide Developers Conference (WWDC) held in Cupertino, California.

At this year's WWDC, Apple showcased a redesigned demonstration version of Siri, which now supports multi-turn conversations with users—a significant upgrade over previous versions. In one demonstration, Siri not only checked concert dates and set ticket-purchase reminders but also planned a route to pick up a friend en route to the concert venue.

However, this launch also highlighted Apple’s distinct strategic approach compared to most of its Silicon Valley rivals: rather than spending billions of dollars betting on infrastructure and hyperscale advanced models, Apple is emphasizing privacy and user convenience for its potential customers. Apple executives underscored this differentiated strategy in their remarks on Monday.

Craig Federighi, Apple’s Senior Vice President of Software Engineering, stated during the event: 'Some companies seem to be charging ahead blindly, pursuing AI for AI’s sake, without truly focusing on who this technology is ultimately meant to serve—all of us.'

Global Macro

Trump Says U.S.-Iran Talks Have Reached 'Final Stages'

On the 9th, U.S. President Trump stated that negotiations between the United States and Iran have reached a "final stage" and that an agreement will be reached "within two to three days." Speaking to reporters at John F. Kennedy International Airport in New York on the 9th, Trump said Israel and Iran had previously been engaged in "back-and-forth exchanges," but have now "agreed to a ceasefire." He added, "We are at the final stage and will reach a very, very great agreement." When asked how much longer the negotiations would take, Trump replied, "Two to three days." From the evening of the 7th to the 8th local time, Iran and Israel engaged in their largest-scale exchange of fire since the U.S., Israel, and Iran announced a ceasefire in early April. Later on the evening of the 8th, both Iran and Israel separately announced they would cease attacks against each other. Trump has recently stated multiple times that an agreement with Iran is imminent, but none has been finalized to date. (Xinhua News Agency)

Is the Bank of Japan hitting the brakes on QT? Reports suggest it may pause the reduction of bond purchases in the next fiscal year, though internal disagreements remain.

According to informed sources, the Bank of Japan will consider maintaining its current scale of government bond purchases unchanged beyond the next fiscal year, thereby pausing its bond-buying tapering process. This move would mark a significant turning point in its quantitative tightening (QT) program.

At its policy meeting scheduled for June 15–16, the BOJ will review its current bond-buying tapering plan—which runs through March of next year—and unveil a new plan covering fiscal year 2027 and beyond. While markets widely expect no changes to the existing tapering schedule, investor attention is now focused on whether the BOJ will continue reducing its monthly bond purchases after FY2027 or maintain the current pace of approximately JPY 2.1 trillion (about USD 13 billion) per month.

Four sources indicated that, given the progress already made in shrinking its massive balance sheet, the BOJ is inclined to halt further reductions in bond purchases. One source stated, “Even if it stops further tapering, the BOJ’s bond holdings will still decline significantly due solely to maturing bonds rolling off naturally.” The other three sources echoed this view, adding that the BOJ may discontinue its practice of setting annual tapering targets and instead adopt an open-ended arrangement, committing to maintain monthly purchases at JPY 2.1 trillion.

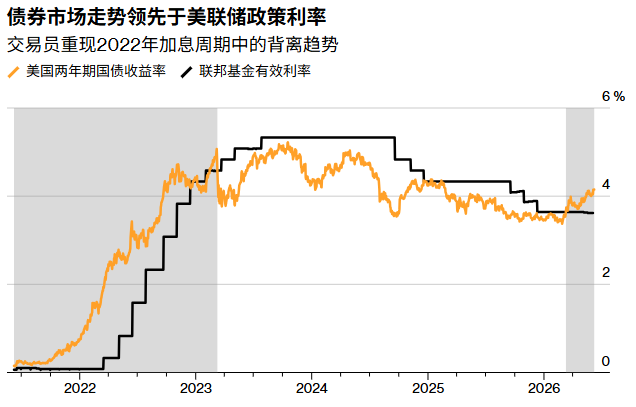

The U.S. Treasury market continues to send signals to Waller: the Federal Reserve needs to raise interest rates.

The U.S. Treasury market is sending a clear signal that current interest rates remain insufficient to curb potential economic overheating. As traders' expectations grow that the Federal Reserve could hike rates by at least 25 basis points as early as October this year, the yield on two-year U.S. Treasuries surged to around 4.15%—its highest level in over a year—significantly above the Fed’s policy rate range of 3.5%–3.75%.

This divergence first emerged in March and reflects the market’s repricing of policy-sensitive assets. Last week’s stronger-than-expected nonfarm payroll data intensified expectations for further rate hikes and reinforced concerns that inflationary pressures and an AI-driven economic boom could lead to overheating. The Consumer Price Index (CPI) and Producer Price Index (PPI) for May, due for release this week, are expected to further substantiate this trend.

Broadband companies' 'land-grabbing spree' backfires: banks offload loans at discounts, while distressed debt funds snap them up at low prices

Banks holding debt claims on highly leveraged broadband providers are selling loans at discounts to distressed-debt funds, reflecting growing fatigue among financial institutions toward cash-strapped telecom companies. In recent weeks, London-based FitzWalter Capital acquired approximately half of the bank debt of German altnet DNS:Net. This followed an announcement by DNS:Net’s owner, 3i Infrastructure, that it would not provide further capital injections, prompting banks to seek exits. After DNS:Net’s fiber broadband rollout plan stalled, the private equity firm wrote down the value of its stake to zero. Similar transactions have occurred repeatedly in the alternative network operator (altnet) sector, where smaller firms aim to challenge incumbent operators such as Deutsche Telekom and BT Group.

FitzWalter also took control of the UK-based company G.Network through the acquisition of both debt and equity, ultimately bringing it under its umbrella via an insolvency process. Separately, a bank that had lent to Deutsche Glasfaser, a leading German altnet operator, sold approximately €350 million (US$404 million) of loans to Strategic Value Partners, led by Victor Khosla, during a €7 billion debt restructuring.

The entry of distressed-debt funds into this infrastructure financing segment—traditionally dominated by banks—highlights how far some financial institutions are willing to go to reduce their risk exposure to this troubled industry.

Top 20 pre-market trading volume stocks in the U.S.

Reminder of the US stock market macroeconomic calendar

(The following times are in Beijing Time)

20:15 Weekly Change in ADP Employment (thousands), Week Ended May 23, United States

20:30 U.S. Trade Balance for April (USD billions)

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Want to select stocks or get a stock diagnosis? Curious about the opportunities and risks in your portfolio? For all your investment questions,Just ask Futubull AI!

Editor/Lee